Energy Transportation Stock: Favorable Market Outlook Matches Strong Financials (NYSE:ET)

to imagine

introduction

It is known that the energy industry has witnessed many fluctuations and instability. This is because many factors affect the supply and demand in this market such as macroeconomic variables, geopolitical events, policies and regulations related to everything such as emissions, zoning rights, etc., making It can affect companies in this market to a great extent. Therefore, it is very important for value investors to have a good perspective on the financial stability of companies in this market, and thus analyze their ability to absorb these risks. The transfer of energy (New York Stock Exchange: ET) is one of the largest energy infrastructures in the United States that transports energy fuels and liquids throughout the United States and internationally. As covered in my former Analyzing ET in detail, one of the key strengths that distinguishes ET from its peers It is its diversified portfolio of assets spread across different geographies, enabling the company to generate strong cash flow.

In this article, I investigate some of the key drivers of the energy market and the impact of recent geopolitical and technological events on energy supply and demand while analyzing the company’s financial position compared to its peers, and ultimately providing an estimate of a fair price for an ET unit.

Market forecast

The energy market has faced many fluctuations and has been one of the most volatile industries. Various factors influence supply and demand in this market including geopolitical events, emissions policies and regulations, zoning rights, etc. Macroeconomic variables such as interest rates and inflation, which raise material costs, and new technologies are other important variables that can play critical roles in the demand and supply sides of investments in the oil and gas industry. But will oil and gas be eliminated from economies any time soon?!

This idea didn’t make sense to me, at least in the near future. For example, during the COP28 conference in April 2024, participating countries agreed to reach 11,000 GW of renewable capacity by 2030. In other words, this means that an average of 800 GW of new capacity needs to be added every year from 2022 to 2030. What are the current capacity levels? In 2022, global wind capacity reached 832 GW, while global solar capacity reached 892 GW. As a result, the annual additional capacity required is almost equal to the entire world’s wind and solar capacity in 2022. There is no doubt that the share of renewable energy in the world’s energy is growing rapidly. However, achieving this goal by 2030 may pose significant challenges.

In addition, the role that artificial intelligence will play in energy consumption is very important. In nitty-gritty, on average, a ChatGPT query requires 10 times more energy than a Google search. With artificial intelligence rapidly developing in economies, the electricity consumed by data centers will rise to 3% to 4% of total energy by the end of this decade. Over the past decade, the growth of energy demand in the United States has been almost zero, and the main reason for this may be related to the efficiency of technology leading to lower energy use. However, energy demand is expected to rise by about 2.4% between 2022 and 2030, while data centers will use 8% of US energy by 2030, compared to 3% in 2022.

The aforementioned high future energy demand appears to be supported by the supply side. The United States produces more than 13 million barrels of crude oil per day, its highest production ever. Due to geopolitical tensions such as Iran’s conflicts with Israel, which added uncertainty to the current rising tensions in the Middle East, oil prices rose in April. However, oil price fluctuations have been largely controlled due to rising crude oil production capacity likely from the United States and other countries. In short, in the event of further supply disruptions in the short term, global supply could be available to the oil market. All these developments and geopolitical events around the world indicate our dependence on oil, and show that this dependence will not end soon. As a result, the higher the demand for energy, the greater the opportunity for energy infrastructure companies like ET to cover the increase in storage demand.

ET’s financial forecasts

2024 has already been a bright year for ET in many financial respects. For example, the company generated $3.9 billion in adjusted EBITDA in the first quarter of this year compared to $3.4 billion at the same time last year. Moreover, the company increased its cash dividend by 3.3% to $1.27 year-over-year as a result of higher distributable cash flow (DCF) of $2.4 billion in the first quarter of 2024 compared to $2 billion in the first quarter of 2023. During the months In the past few years, management has redeemed a large number of its existing units, which is a sign of low future cash flow for the company as it does not need to pay dividends for this number of units. The main focus of Energy Transition in terms of capital expenditure has been on the intermediate products, NGL and refined products segments, which will lead to increased volumes. It is worth noting that the highest increase in adjusted EBITDA refers to the crude oil sector, which reached US$848 million at the end of the fourth quarter compared to US$526 million in the first quarter of 2023. As management commented: “ This is primarily due to significantly stronger pipeline volumes, increased terminal throughput, as well as favorable timing of gains associated with hedged inventory. Energy Transfer increased crude oil transportation volumes from 4.2 million barrels per day at the end of the first quarter of 2023 to 6.1. million barrels per day at the end of the last quarter, showing a 44% increase. Management has ongoing plans to expand potential capacities in various sectors, such as moving to the next phase of capacity expansion to transport natural gas from northern Louisiana to the Gulf Coast. Another important point is related to the methodology Contracting with ET, nearly 90% of the company’s contracts are on a fee basis to protect the company from commodity price fluctuations, enhancing confidence that regardless of the high-risk nature of the industry, energy transmission provides stability and improves its operational efficiency by increasing its volumes.

In early May 2024, the company completed its acquisition of NuStar Energy LP. This acquisition will result in an additional potential increase in capacity because NuStar has approximately 9,500 miles of pipeline. It also has 63 terminals and storage facilities to store and distribute crude oil, refined products, renewable fuels and ammonia. Given the positive impact of this order on ET’s financials, management has revised its 2024 adjusted EBITDA guidance from $14.5 to $14.8 billion to $15 to $15.3 billion.

ET evaluation

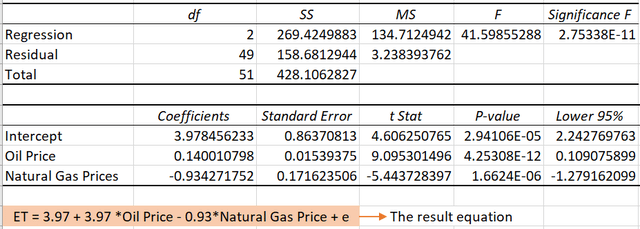

Making the most of data is my forte. Given my model of ET unit price, my analysis statistically highlights the importance of oil and gas prices in determining the stock price. These results indicate the extent to which fluctuations in energy prices affect the resulting price, highlighting the high-risk nature of this industry (see Table 1).

Table 1- Regression model to predict the effects of oil and gas prices on ET stock price

Author’s calculations

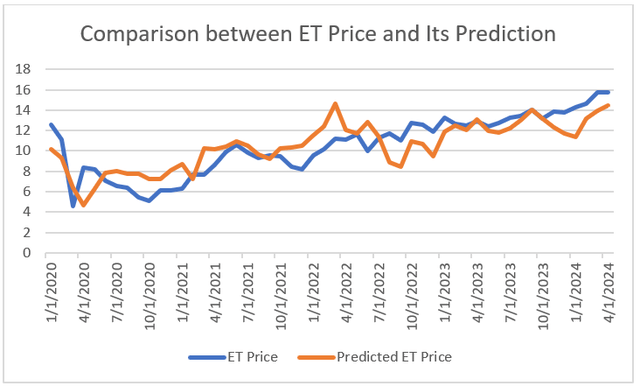

I plotted my forecasts for the period from 2020 to the first quarter of 2024. As Figure 1 shows, my forecasts were fairly close to the actual stock price. As a result, and based on the expectations of higher oil prices in the near future and their strong impact on the company’s stock price, which was shown previously, I believe that ET still has a bright future.

Figure 1 –

Author’s calculations

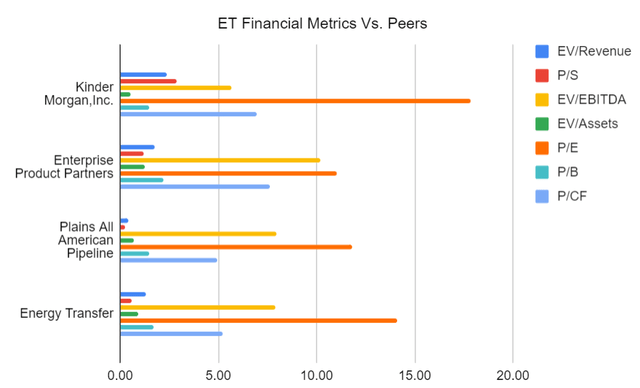

In addition to the effects of market variables on the company’s stock, its financial statements show a healthy and strong future outlook for ET compared to its peers. In this regard, I used the Comparable Companies Analysis (CCA) method to analyze ET’s financial health against its peers and evaluate its unit price. As shown in Table 2, ET’s P/E ratio of 0.61x is one of the lowest among its peers, after Plains All American (PAA) with a P/S ratio of 0.24x. Overall, as a sign of its potential undervaluation, ET’s P/E ratio is well below the group average. ET has an EV/EBITDA roughly the same as its peers’ average of 7.93x, while Enterprise Products Partners (EPD) has the highest ratio. Also, after PAA, Power Transmission has the lowest P/E, which, for value investors, indicates that it has a higher ability to generate cash flow compared to its market price, reflecting a sign of operational efficiency, compared to its peers. Figure 2 indicates a comprehensive comparison of ET’s financial metrics versus its peers.

Figure 2 –

Author’s calculations based on alpha data search

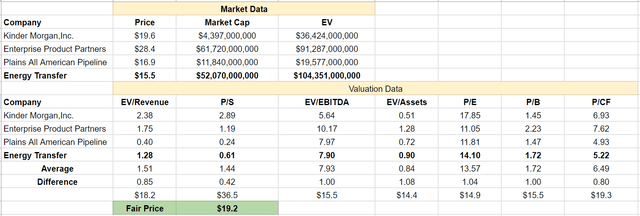

When all is well, ET has shown a relatively low value compared to its peers, and its financial metrics indicate the financial and operational health of the company. As Table 2 shows, the fair price for ET is around $19 per unit based on the CCA approach, which is very close to the stock’s pre-pandemic strikes, and I believe the ET unit price has the potential to reach pre-pandemic records.

Table 2 – Evaluation of ET unit based on CCA method

Author’s calculations based on alpha data search

Risks related to energy transmission investment

One of the major risks related to ET’s operations, other than fluctuations in commodity prices, relates to regulation of the industry. Energy Transfer is one of the largest energy infrastructure companies in the United States and operates in a highly regulated industry. State and federal regulations in various aspects such as environmental concerns may negatively impact a company’s financial condition. Although I am optimistic about ET, we must take into account several risks that the company faces such as the recent increase in investments in renewable energy technologies, which may bring technological challenges to the company and reduce the demand for the fuel it transports and, ultimately, negatively impact Over its capacity. Cash flow generations. Furthermore, economic conditions such as recession, inflation, and interest rates may directly impact reduced household spending on gasoline, diesel, and travel. Last but not least, weather plays a critical role in energy usage rates, which may affect demand for ET infrastructure on a seasonal basis.

Conclusion

In this article, I looked at how new technologies such as artificial intelligence are raising energy demand. On the supply side, although geopolitical events, especially in the Middle East, may disrupt supply, increased supply from the United States and other countries could resolve this shortage. Regarding Energy Transfer’s financial health, I’m bullish on the company based on its metrics compared to its peers. All said and done, I assess a fair price for ET at around $19 per unit.

I appreciate you taking the time to read this content, and as always, I welcome your thoughts and opinions.