Daniel Grzelj

Amid feelings of depression, the management team Innovix (Nasdaq: INVEX) fired on all cylinders in the first quarter of 2024.

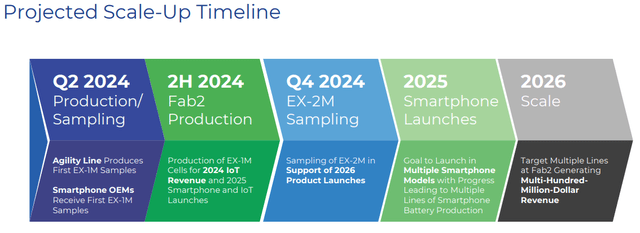

Manufacturing milestones have been reached, and Enovix is on track to produce and deliver its first samples With EX-1M technology in the second quarter of 2024 and Fab2 to be ready for production in the second half of 2024.

As the sampling process concludes, I expect to see more commercial interest in Innovix. This was also supported by the development agreement signed with the top five smartphone manufacturers by volume.

Enovix is not stopping there, as six of the top eight smartphone operators will receive EX-1M samples.

On top of these commercial developments, on the product front, Enovix has been working hard to improve its technology and products, and the next product, EX-2M, is expected to be produced. The sample is due in the fourth quarter of 2024, and the team is already working on the EX-3M, which is expected to be sampled in 2025.

I’ve written extensively about Enovix on Seeking Alpha, which can be found here. I’m more confident than ever about the company’s ability to deliver, and in this article, I aim to share with you why.

Manufacturing is on the right track

As of Q1 2024, factory acceptance testing of the Gen2 Agility line has been completed, most of the machines are already in Malaysia, and site acceptance testing is also well underway.

With this, management expects that they are on track to produce the first battery samples with EX-1M technology in the second quarter of 2024.

Factory acceptance tests for the high-volume Gen2 Autoline are also nearing completion. Productivity is also expected to be over 95% for the high volume Gen2 Autoline since it uses the same process as Agility Line.

With a strong focus on onboarding and getting things right at an early stage, management has a high degree of confidence in scaling the high-volume Gen2 Autoline.

In the second quarter of 2024, Enovix will sample the first EX-1M batteries from the Agility line to smartphone OEMs and some IoT customers.

In the second half of 2024, Fab2 will be ready for production.

By Q4 2024, Enovix expects to sample the EX-2M.

By 2025, Enovix aims to launch multiple smartphones and IoT clients with the EX-1M battery.

In 2026, Enovix will focus on expanding into multiple lines via Fab2.

Extend Schedule (Enovix)

Marketing has shown tremendous progress

This quarter marks a new chapter for Enovix, and will likely be one of the most important on the marketing front, as there were multiple material updates this quarter.

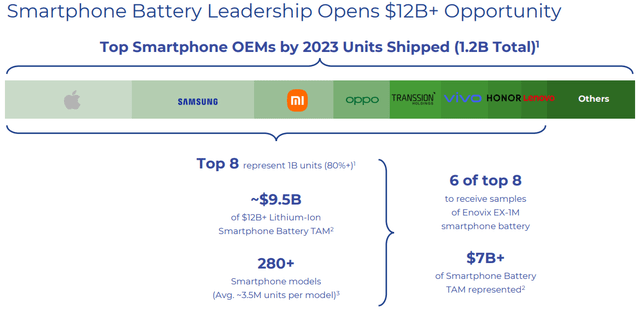

The first major announcement on the marketing front is Enovix announcing its first-ever development agreement with the top five smartphone manufacturers by volume.

This is a major development for Enovix, crushing critics who don’t believe in any marketing opportunities for the company. I’m of the opinion that this is a great endorsement of its strategy to focus on large smartphone OEMs, and also a great endorsement of the company’s technology and management team.

I think we’ll see more of these development agreements signed with Enovix through 2024 as more of the top eight smartphone OEMs trial Enovix products.

Before I talk about the second major announcement, I need to share a little more about Enovix’s market opportunities and where it’s focused.

This is one of the best chipsets that Enovix has offered in terms of its market opportunity.

As shown below, the smartphone battery market today is approximately $12 billion. 80%, or $9.5 billion, of the smartphone battery market is made up of the top eight smartphone players.

Chance Smartphone (Enovix)

The second major announcement on the marketing front made by Enovix is that six of the top eight smartphone operators will be getting EX-1M samples from Enovix.

To put this in context, this represents $7.5 billion of the total addressable smartphone battery market.

To indicate the scale of this opportunity, the top eight smartphone companies collectively produce about 280 smartphone models, and the average smartphone unit size is 3.5 million per model.

Thus, from Enovix’s perspective, three to four of these smartphone models will use the full capacity of one of its Gen2 lines.

The smartphone market is Enovix’s largest consumer electronics market, but another $12 billion of the total addressable market is in the combined IoT and computing sectors.

There are two things to note.

The first is that the largest smartphone OEMs are also the largest customers in the IoT and computing markets, producing tablets, wearables and PCs which all represent an additional market opportunity if Enovix wins smartphone business from the larger smartphone OEMs.

The second thing is also that the requirements for smartphones are the most stringent and difficult to achieve among the three markets. If Enovix can win the smartphone business from the larger smartphone manufacturers, there is a high probability that its IoT and computing business will also move to Enovix and even have a shorter qualification period after that.

A roadmap for its products

Enovix is focused on improving its batteries and is moving very quickly in this regard.

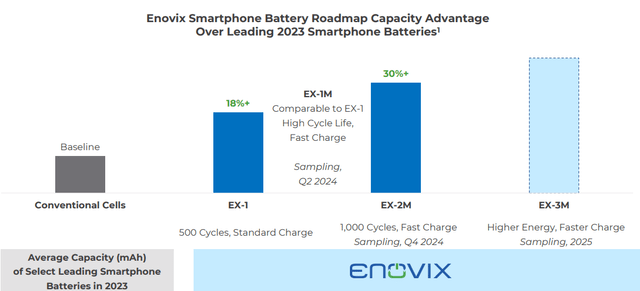

I previously mentioned the EX-1, which is the current technology we’ve been sampling since last year, and the EX-1M, which differs from the EX-1 in that it has better cycle life and fast charging characteristics.

The EX-1M will begin sampling in the second quarter of 2024, and this offering already represents the level of batteries available in the smartphone market.

The next product, EX-2M, will have further improvements to cycle life, power density and fast charging, which is expected to be sampled in the fourth quarter of 2024.

The R&D team is already working on the EX-3M, which will continue to make further improvements to cycle life, power density and fast charging, and the EX-3M is expected to be sampled in 2025.

Product Roadmap (Enovix)

The third major update from the marketing front is that management announced that it continues to make progress with IoT customers, and the strategy here is similar to that of smartphones in that it focuses on a few high-volume opportunities.

The commercial team is making progress on the EX-1M and EX-2M IoT opportunities, and management expects to launch these products in 2025 and 2026.

Smartphone OEMs are increasingly seeing the need for a battery with increased power density for the growing number of on-device AI applications, and the number of engagements Enovix has with the top eight smartphone OEMs is clear.

more

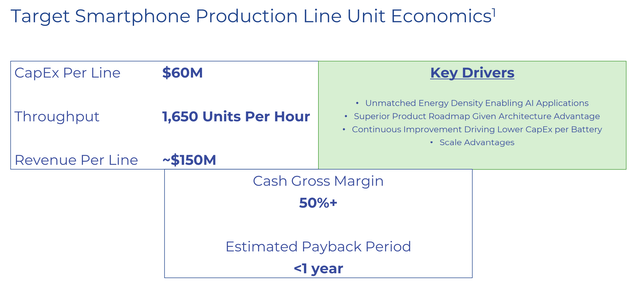

With Line 1 and Fab2 expected to begin production by the second half of 2024, management now has a clearer view of the unit economics of future Fab2 production lines.

From a capital expenditure perspective, management anticipates that $60 million in capital expenditures will be needed per line, and the target throughput per line is 1,650 units per hour.

However, each line is capable of generating $150 million in revenue per product line and with gross cash margin expected to be at least 50%, Enovix expects the payback for each of these lines to be only one year.

I think this gives investors an idea of how Enovix will expand the number of lines after the first line begins production in the second half of 2024, and that the company has attractive unit economics as it scales the business.

Smartphone Production Line Economics (Enovix)

Expanding the cash runway by reducing costs

Enovix announced $35 million in cost reductions, primarily in operating expenses.

These goals are expected to be achieved from the fourth quarter of 2024 through 2025 as more R&D activity moves from Fab-1 to lower-cost Enovix sites in Malaysia, Korea and India.

As cost-cutting measures and capital expenditures begin to ease following final vendor payments following the completion of FAT and SAT on Fab-2, the company expects to have enough cash on hand to last through 2026.

So, the question is whether Innovix will need to raise capital?

Management shared some thoughts on the call that as qualifications come in and customers express interest in purchasing Enovix batteries, there are two potential sources of capital where the company can attract the necessary capex for subsequent production lines.

The first group are customers who are increasingly providing financial support to Enovix to enable the company to reach the next stage in terms of expansion.

The second group is governments and sovereign wealth funds looking to provide capital to Innovix, most likely from Malaysia.

Finally, management confirmed and confirmed that, given current inventory levels, they do not view increasing equity as an option.

With the steps taken to improve the cost structure mentioned above, this has also helped lengthen Innovix’s runway such that it will not have any need in the near term to raise capital.

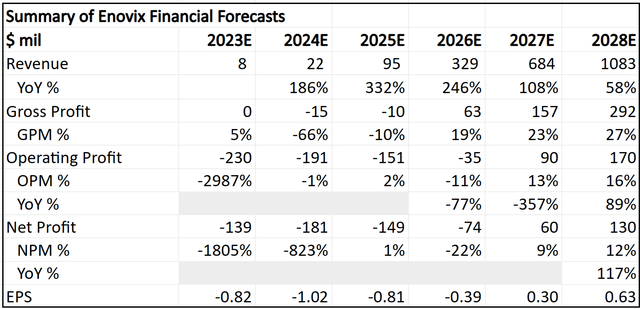

My focus on earnings is not necessarily on the financials, since the main thesis lies in Fab-2.

For Q1 2024, Enovix reported revenue of $5.3 million, beating expectations of $3.5 million to $4.5 million, driven by strong Routejade IoT battery shipments.

Q1 2024 adjusted EBITDA loss of $26 million was in line with guidance of $24 million to $31 million.

For the second quarter of 2024, Enovix’s guidance was for revenue of $3 million to $4 million, EBITDA loss of $26 million to $32 million, and adjusted EPS loss of negative $0.22 to negative $0.28.

evaluation

It goes without saying that Enovix’s financials will change from time to time as more information emerges about its manufacturing, marketing, and margins progress.

I think that on a very optimistic to very pessimistic range, my financials are on the conservative end because I think there are many risks and uncertainties along the way.

It has assumed 4% dilution per year or 20% cumulative dilution, although management has indicated there is unlikely to be any capital raising in the near term.

Additionally, while if there were one line and four lines operating at full capacity, Enovix should be able to generate revenues of $150 million and $600 million respectively, I incorporate some conservatism into this. Management expects to be able to ramp up these four lines in 2026, but I have postponed that to 2027, and I also assume that in 2025, the first line will not reach full capacity.

Enovix 5-Year Financial Statement Summary (Author-created)

My intrinsic value for Enovix has been revised to $15.60.

My one-year and three-year price targets have been revised upward to $17.80 and $23.80, respectively, based on 2028 financials discounted to 2024 and 2026, respectively.

Conclusion

While there is a lot of good news to celebrate following this earnings report, Enovix still has a lot of execution to do before it becomes a leading battery company.

For now, the company has been able to build a product that is superior to others on the market, building a factory capable of building samples first, then at scale, and attracting the largest smartphone operators interested in sampling these batteries.

The next step, of course, will be for Enovix to need to convert actual wins for its first and subsequent lines.

With this demand, it will be easier for Innovix to attract capital from clients or governments. With this additional capital for the next few lines, demand for Innovix will continue to grow.

Naturally, the company needs to be able to manufacture these pioneering batteries on a large scale, and do so in an economically attractive way.

I began investing in Enovix when the new management team came in, and after watching the management team deliver on its promises over the past year, I have become increasingly confident in their abilities to scale Enovix into the leading battery player it can become.