Diverse photography

introduction

I had a “sell” thesis for Enphase Energy (NASDAQ:INV) in March. The stock has gained 3% in line with the S&P 500 since mid-March, which makes my thesis not sound very good. On the other hand, the company continues Navigating a challenging environment as the residential solar market struggles to bounce back. There are some strong indicators that it may take longer for the industry to recover. The company has had disappointing earnings recently, and the next quarter is not expected to be much better as revenue is expected to decline further and by a significant amount. The valuation still doesn’t look attractive, and I’m leaning toward reaffirming a “sell” rating.

Fundamental analysis

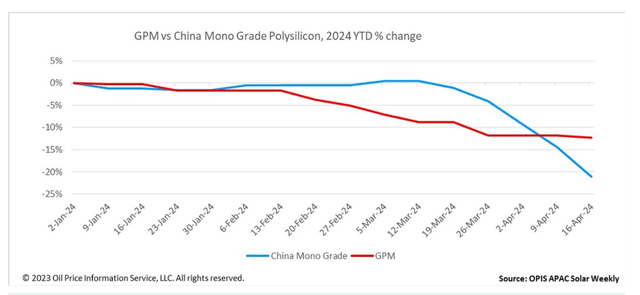

There are factors that indicate that unfavorable trends for the residential solar industry are likely to continue. According to pv-magazine.com, global polysilicon (‘GPM’) prices have fallen. Noticeably since the beginning of the year due to weak demand. China is also showing weakness in monograde polysilicon in 2024, indicating that demand for solar panels is weak worldwide. Polysilicon is An essential element The production of rooftop solar equipment and the sharp decline in its price are strong evidence of weak demand from end markets.

pv-magazine.com

Furthermore, as interest rates in the USA and Europe remain high, demand for residential solar will likely continue to decline, which could delay the industry’s recovery.

Another downside factor I’d like to highlight is that ENPH’s revenues are expected to decline much deeper in 2024 than the expected industry contraction. According to consensus, the top line is likely to contract by 35.5% in fiscal 2024. This is a deeper decline compared to the 13% contraction in the residential solar market in 2024 that Wood Mackenzie predicted. With this expected weakness compared to the industry in 2024, I have doubts that ENPH will be able to achieve a 45.8% revenue recovery in fiscal 2025. Furthermore, Wood Mackenzie forecasts that there will be a more modest industry expansion of 13% in 2025. With a notable discrepancy between ENPH’s 2025 and industry forecasts, there is a risk that the company’s 2025 revenue estimates will be lowered soon.

Sa

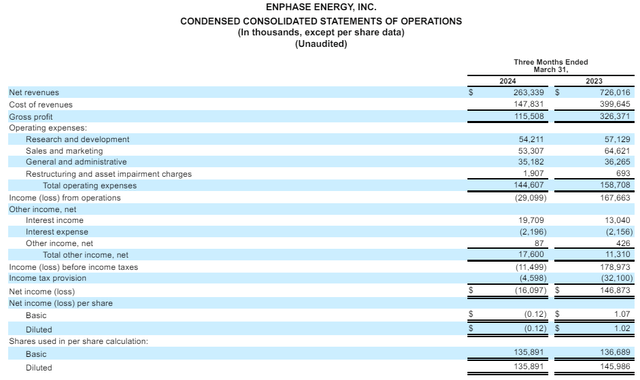

ENPH is struggling to weather industry headwinds as last quarter’s financial performance was disappointing. The company missed consensus estimates, which never adds optimism to investors. Revenue declined approximately 64% year over year.

10-Q Report, Q1 2024

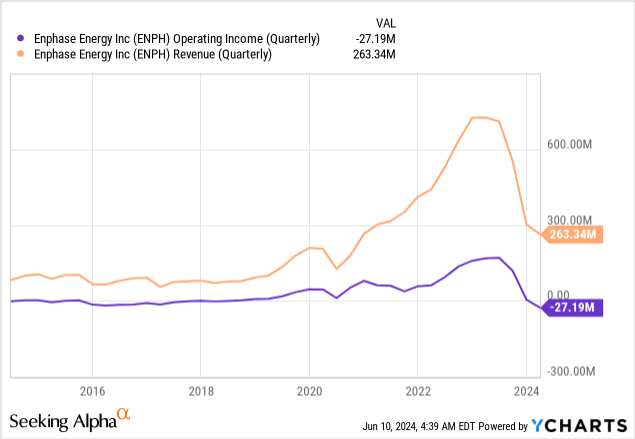

Gross margin was not affected much but the decrease in operating expenses was marginal. This resulted in negative operating income, something that had never happened to ENPH since 2017. However, in 2017, the company was much younger, and its revenues were much lower. However, management is not showing enough flexibility in operating expenses to maintain profitability. During the earnings call, management did not outline any brief cost-savings plan. This doesn’t look shareholder friendly, in my opinion. I believe any management should react by offering cost efficiencies when their revenues are shrinking at a rapid pace. Aside from information released in late 2023 about a 10% headcount reduction, there has been no news of new layoffs. This seems disproportionately low compared to the 64% year-over-year revenue decline in the first quarter.

Moreover, the pain won’t end in the second quarter. Management expects revenue to be between $290 million and $330 million for the quarter. The midpoint of the range is $310 million, approximately 56% lower compared to revenue generated during the second quarter of 2023. For the third quarter of 2024, consensus estimates expect revenue to decline by 24% year over year. In my opinion, not having a cost-cutting plan amid a high-to-mid double-digit revenue decline is a bad sign. This means that profitability is likely to struggle further.

Evaluation analysis

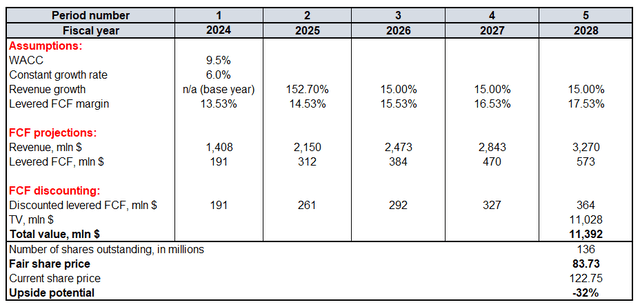

My previous estimate for ENPH stock price was $118. Let me recalculate my discounted cash flow (DCF) model to assess how much fair value has changed over the past three months. Future cash flows will be discounted using a weighted average cost of capital of 9.5%. There was a massive drop in consensus estimates for FY2024 compared to the previous cash flow stream, from $1.62 billion to $1.48 billion. This also negatively impacted FY2025 revenue estimates, falling from $2.33 billion to $2.15 billion. For the years following FY2025, I repeat the same 15.1% revenue CAGR. Despite the temporary weakness, I believe the secular residential solar trend is strong and repeats a consistent high 6% growth rate for the Terminal Value (‘TV’) calculation. The TTM leveraged FCF margin also decreased from 15.57% to 13.53%. I use the 13.53% level for FY 2024 and replicate the 1 percentage point annual expansion due to secular tailwinds. According to Seeking Alpha, there are 136 million shares of ENPH stock outstanding.

Calculated by the author

With all the unfavorable changes in assumptions, I’m inclined to lower my fair share price estimate for ENPH significantly, from $118 to $84. The new price target indicates a downside potential of 32%, meaning ENPH is significantly overvalued.

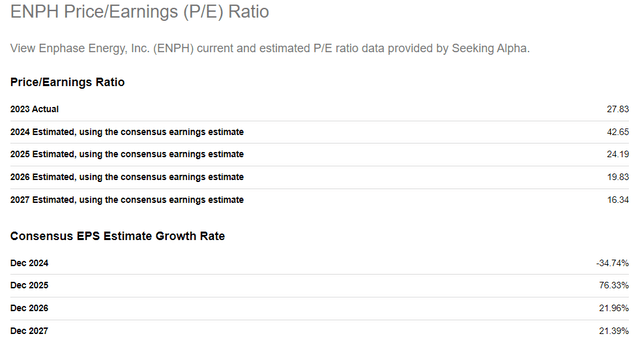

Examining ENPH’s valuation ratios also doesn’t help in seeing any decline in value. The forward P/E ratio is close to 100, which is high for a company experiencing declining revenues and shrinking profitability. The consensus expects P/E to shrink to as low as 16 by fiscal 2027. However, this would be the case if adjusted EPS nearly triples between fiscal 2024 and fiscal 2027, from $2.88 to $7.51. This is a difficult task, especially with headwinds expected to continue.

Sa

Mitigating factors

The Federal Reserve is likely to start cutting interest rates soon, which is a potentially strong catalyst for all growth stocks. Although ENPH faces severe headwinds, they are likely to be temporary. From a secular perspective, the company has the potential for long-term growth. ENPH continues to show strong profitability despite rapidly shrinking revenues. Its strong financial position can withstand a turbulent environment, which is also a fundamental strength. Therefore, ENPH could become one of the favorites to ease monetary policy.

Yahoo Finance

Solar energy in the United States and the European Union relies heavily on government subsidies. Therefore, expanding government incentives for faster adoption of solar energy in residential areas may help the industry recover faster, and will lead to a reassessment of FY2024-2025 revenue projections. This could significantly positively impact the net present value of future cash flows and boost the target stock price, and my thesis would not fare well in this case.

Conclusion

ENPH continues to internalize the broader industry’s weakness, but management does not appear to plan to at least partially mitigate the massive decline in revenues through cost-saving initiatives beyond the modest 10% layoffs last December. The valuation doesn’t look attractive either, and the price target for ENPH is $84.