omersukrugoksu/E+ via Getty Images

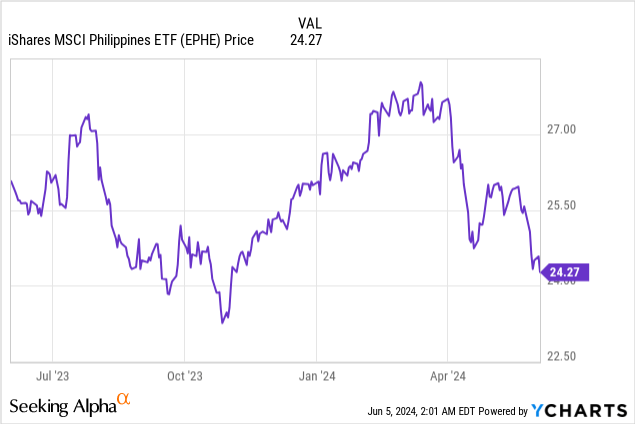

iShares MSCI Philippines ETF (NYSEARCA:EPHE) has seen a significant amount of volatility since I last covered the name (see EPHE: More headwinds on the horizon), and this year was no different. After a significant rise in Q1, the Fund It suffered a sharp decline in reaction to a tightening repricing in interest rate expectations. As it stands, EPHE is now down to high single digits year-to-date. However, the big problem with buying the dip is that domestic interest rates look increasingly likely to remain “higher for longer” given Rice inflation pressures And a A significant increase in the minimum wage. central bank Last comment He also stressed the need to protect against further currency weakness, so it seems unlikely that there will be a pivot to the Philippines anytime soon.

This is not an ideal setup for EPHE’s portfolio of interest rate sensitive real estate and industrial properties, many of which are Which was strongly rerated on hopes of lowering interest rates. Even if its banking holdings see an extra quarter or two of margin benefit from rising interest rates, the relatively low financial/nonfinancial split means it won’t be enough to offset the headwinds for the rest of the portfolio. EPHE is not priced particularly cheaply on earnings or relative to the underlying book (~30% premium) here. Net-net, I don’t see a particularly compelling case for buying Philippine stocks.

JP Morgan

EPHE Overview – The largest and most liquid Philippine tracker

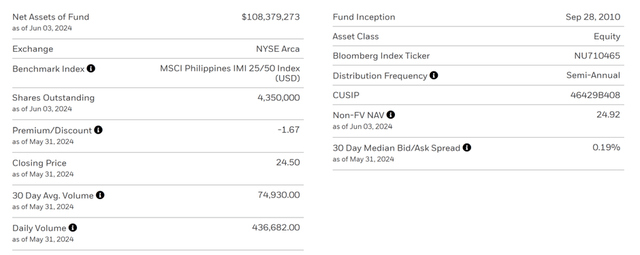

Fundamentally, the iShares MSCI Philippines ETF has not changed much in recent quarters. It still tracks the dollar-denominated MSCI Philippines IMI 25/50 Index, which imposes concentration limits on a basket of Philippine large-cap stocks. The asset base is a bit larger but still relatively small at around $108 million, so liquidity (about 19 basis points in bid/ask) and execution are not great by iShares standards. However, an expense ratio of 0.6% is competitive, especially given the lack of US-listed alternatives to the Philippines’ single-country exposure.

iShares

EPHE Portfolio – Tilt towards larger companies in the Philippines

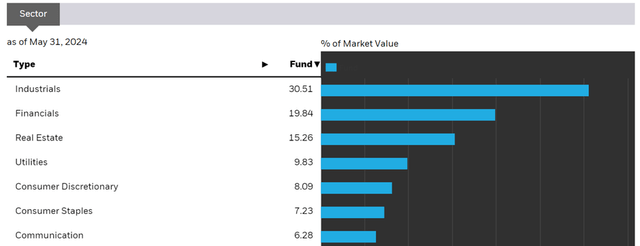

The ETF has narrowed its portfolio to 33 holdings in recent quarters, meaning the allocation ratio is higher than before. By sector, Industries, where the various Philippine conglomerates are categorized, continues to have the largest exposure at 30.5%. Interest rate sensitive sectors such as financials (19.8%) and real estate (15.3%) are other major allocations. The rest of the top five list is made up of utilities (9.8%) and consumer discretionary services (8.1%) – both of which have outperformed in recent years.

From a sector perspective, there are two things worth noting here. First, the diversified nature of EPHE Group’s holdings makes its actual sector profile more balanced than the headline numbers suggest. Second, while the fund is relatively defensive, this cycle has seen the stock’s beta rise slightly to 0.8 (vs. the S&P 500 (SPY)) – an indication of the portfolio’s current price sensitivity.

iShares

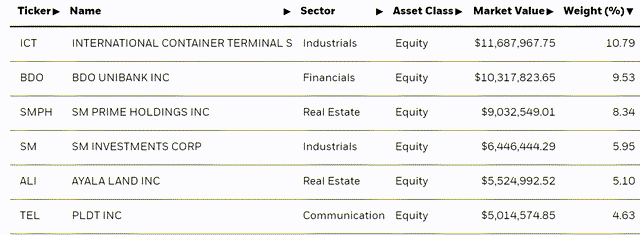

With the addition of International Container Terminal Services (OTCPK:ICTEF), the largest piece in billionaire Enrique Razon’s business empire, to EPHE, investors now have exposure to the Philippines’ most prominent business families. Recall that the fund has historically maintained exposure to local businessman Henry Sy’s real estate developer, SM Prime (SPHZF) (8.3%), and its holding company, SM Investments (OTCPK:SVTMF) (6.0%). Another key element is EPHE’s exposure to the Zobel de Ayala business group via Ayala Land (OTCPK:AYAAF) (5.1%) and Ayala Corp (4.2%).

Including BDO Unibank (OTCPK:BDOUY), the top five companies contribute 39.7%, although the overlap between the conglomerates and their subsidiaries (for example, SM Investments has a close to 50% stake in SM Prime and Ayala Corp has Approximately 51% of Ayala Land) means the actual concentration of individual stock is higher than it appears.

iShares

EPHE Performance – Poor serial performance across sessions

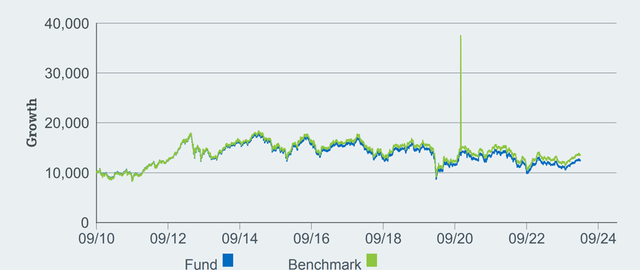

Over the past decade, EPHE, along with the rest of Southeast Asia’s large-cap companies, has destroyed more shareholder value than it has created. For context, the ETF has five- and ten-year annualized returns of -4.5% and -2.2%, respectively. Even after the Covid-19 crisis, when many stock markets enjoyed a strong rebound, EPHE remained in the red (-2.2% three-year annualized return).

iShares

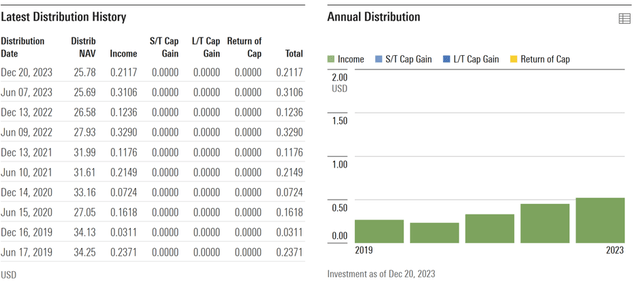

Despite having cash-generating conglomerates and banks within its portfolio, EPHE doesn’t make much either. The semi-annual distribution yield is about 2% on a trailing-twelve-month basis (about 1.2% 30-day SEC yield) – well below the top yield in Southeast Asia, the iShares MSCI Singapore ETF (EWS) at about 6%. The crux of the problem is that large-cap companies in the Philippines tend to be family-controlled conglomerates that do not prioritize returns to minority shareholders. Barring a tangible shift in management, I don’t expect EPHE to do a significant income check anytime soon.

Morning star

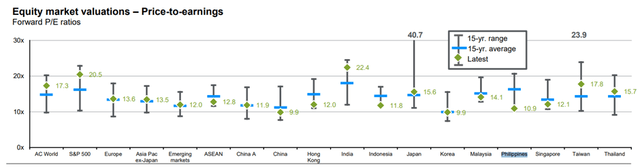

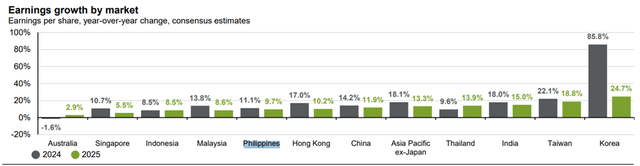

Perhaps the biggest problem for EPHE is that even after years of withdrawals, it is not particularly cheaply priced relative to its fundamentals. The fund currently trades at approximately 11x earnings and 1.3x book; In comparison, earnings growth is on track at 10-11% until 2024/25. Without a more attractive fundamental case for foreigners to return to the Philippine market, we expect technical headwinds from lower investor participation and lower benchmark weights to further pressure performance.

JP Morgan

Staying on the sidelines in the Philippines

After starting the year strong, EPHE quickly gave up its gains, and perhaps rightly so, given the direction in which fundamentals are headed. In the near term, all eyes will be on seasonal inflation and its impact on monetary policy, given the interest rate sensitivity of the EPHE portfolio. Moreover, the ability of large-cap Filipino companies to grow their earnings quickly enough to justify their multiples and ride out currency depreciation will be key. However, at the moment, I don’t see a compelling fundamental or technical case for owning EPHE and will remain on the sidelines.