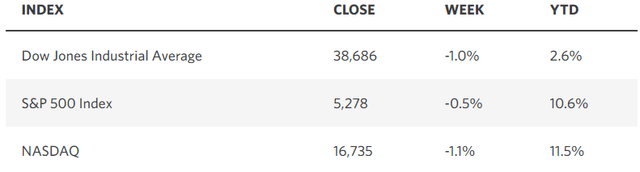

Klaus Wiedefelt

Technology was the worst-performing sector in the market last week, as disappointing earnings reports from Salesforce and Dell Technologies prompted profit-taking in the most influential group, which also put an end to a five-week winning streak for the major market averages. the The fact that the first quarter economic growth rate was revised from 1.6% to 1.3% didn’t help matters either, especially when the decline was driven by a slowing growth rate in consumer spending. But we must beware: as the deflationary trend continues following slowing economic growth rates, pessimists will stop warning about inflation and start renewing their calls for stagnation. This is because soft landings, which are difficult to achieve, are not in their rules of the game. That’s good because this bull market needs a wall of anxiety to climb as we enter the mid-cycle slowdown phase of this expansion.

Edward Jones

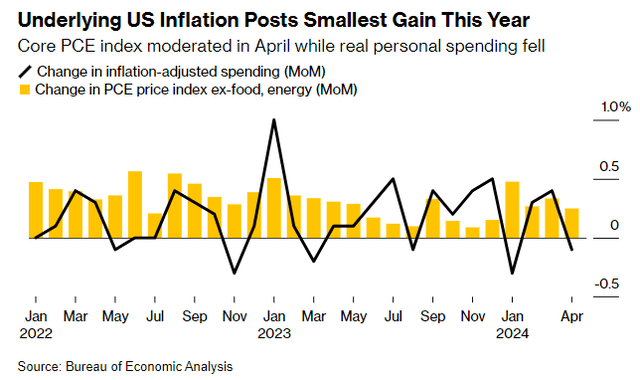

Last week ended with a strong performance as April inflation data was in line with expectations, confirming the deflationary trend. The core personal consumption expenditures price index rose 0.2%, leading to a 2.8% annual rise for the third month in a row. Although the downward trend over the past three months has stalled, personal spending in April fell by 0.1% in (real) inflation terms, and spending on services rose by only 0.1% in real terms. Therefore, we are seeing signs of lower inflation rates in the form of declining demand for goods and services.

Bloomberg

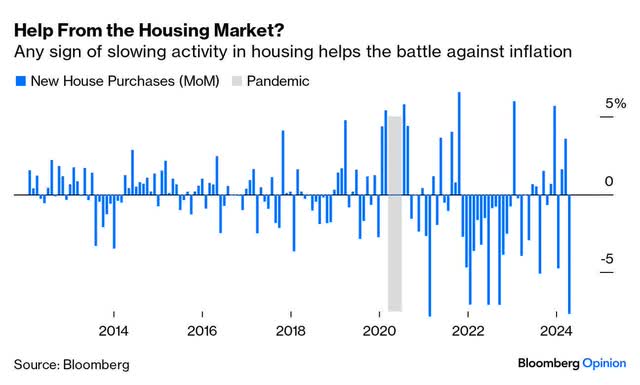

It’s not just goods and services, either, as the housing market is finally seeing some easing in price pressures, with homebuyers rejecting new listings that don’t take into account 7% mortgage rates. As a result, landlords are cutting asking prices by numbers not seen since late 2022, according to data from Redfin This corp is raising interest rates in action to reduce the inflation rate. Inventories should begin to rise more clearly as activity slows, and the market should rebalance in favor of buyers over sellers, causing pending home sales to grow again. The rate of change here has become less negative, which is a positive thing.

Bloomberg

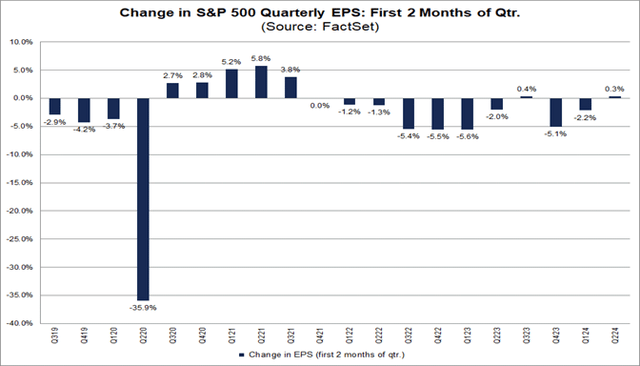

With lower inflation rates come slower rates of economic growth, as we saw in the first quarter GDP review, and this is leading to bear warnings about a recession. Let’s not forget that S&P Global’s Purchasing Managers’ Index (PMI) survey of services and manufacturing companies conducted two weeks ago saw a sharp rise in activity during May. I will look for confirmation of this strength in this week’s ISM polls. A good sign of continued growth comes from corporate earnings estimates for the second quarter, which were raised by analyst consensus during April and May. This is not what we usually see, unless we are emerging from a recession, when the consensus tends to be overly pessimistic.

FactSet

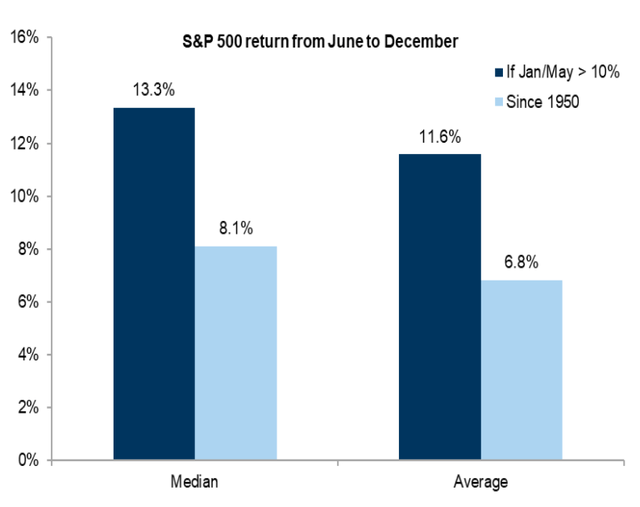

Soft landings balance enough growth to sustain the expansion, with enough of a slowdown in the growth rate to reduce the inflation rate. I still believe we are on the right track, but the market will be our best leading indicator in this process, and its performance so far is a positive sign. To reinforce the bullish outlook, I found another encouraging statistic for the remainder of 2024. Over the past 74 years, the S&P 500 has risen 10% or more during the first five months of the year 21 times. The index suffered losses only twice, in 1987 (-13%) and 1986 (-0.1%). The average gain over the remaining 19 years was 11.6%. I don’t use statistics like this to formulate my basic expectations, but they give me confidence that I’m on the right track when I encounter them after I’ve already established such an outlook.

Bloomberg

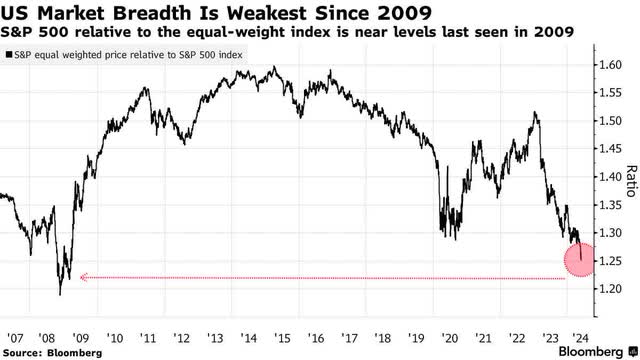

Now consider that the spread in performance between the market cap-weighted S&P 500 and its equal-weighted version reached an extreme not seen since 2009. That year was one of the best times in recent history to invest in average stocks. I think it’s a precursor to the shift from technology to every other sector of the market, that Magnificent 7’s earnings growth rates slow dramatically between now and the end of the year. Meanwhile, we see slower but increasing growth rates for the rest of the market. This should narrow the performance spread shown in the chart below and improve market breadth.

Bloomberg