Trevor Williams

thesis

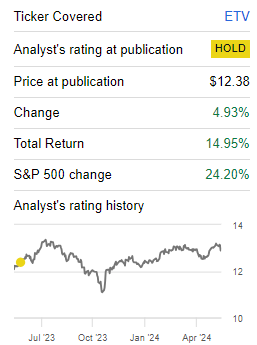

Buy-and-write opportunities fund managed by Eaton Vance (New York Stock Exchange: ETTV) is one of our core holdings, and we’ve been covering the last name for about a year with a Hold rating:

Pre-evaluation (author)

2023 was tough The overall year of the fund is due to its structure, with the name lagging the performance of the S&P 500 due to its covered buy-period setting, and sudden increases in stock prices rather than smooth rises.

In this article, we’ll revisit the name in light of the big picture for 2024, and highlight why we think the name is an appropriate fund to use in order to gain equity exposure and extract dividends.

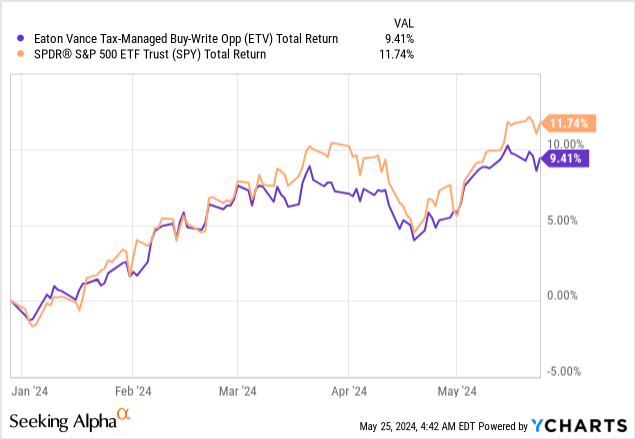

Back to having similar performance to the S&P 500

This year has been much better for the fund, as the smooth market has been closely matched By CEF:

Year-to-date, the CEF is up 9.4% on a total return basis, while the S&P 500 is up 11.7%. Buy-write mutual funds work best when the market is moving up in a smooth manner, with small weekly gains. In this layout, the CEF gets most of its benefits from written call options, and is thus able to closely match the performance of the S&P 500.

ETV, just like other call and put names, will continue to be negatively impacted by the very low VIX environment currently prevailing, and an overall setup resulting in lower than usual option premiums.

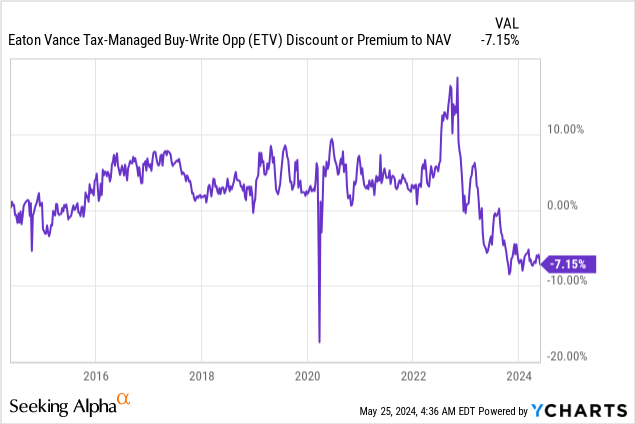

The discount to net asset value is historically wide

ETV typically trades at a slight premium to NAV of 5% on average:

Given its poor performance in 2023, the market has now taken the name to a very significant -7% discount to NAV. If we look closely at the chart above we will notice that this discount is a broad historical discount, when we remove the Covid shock in 2020.

It appears that market participants are now pricing each year to resemble 2023, which is not actually the case. Buy-write funds tend to underperform in aggressively rising markets, because their overlay feature significantly reduces the upside. Not every year will see the same exponential upward movement, and we believe there will be a mean reversal in the discount to NAV, with the potential for a 7% gain as the fund trades flat with its NAV.

Classic construction of buy and write

According to her literature:

The Fund invests in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a significant portion of the value of its common stock portfolio in an effort to realize current gains from the option premium. The Fund’s portfolio managers use the Adviser and Subadviser’s internal research and proprietary modeling techniques in making investment decisions.

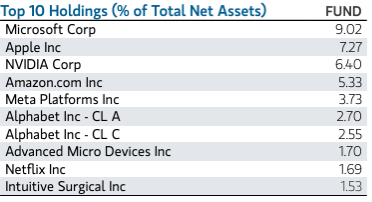

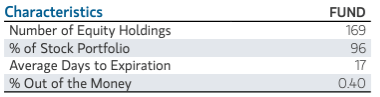

CEF has only 169 holdings, the most important names of which are as follows:

Top Holding (Fact Sheet)

Portfolio managers attempt to outperform the index on the back of their holding selection. The Fund will never generally hold all 500 components of the S&P 500 Index, but will always participate in selecting an individual name as directed by its portfolio managers.

Covered calls are covered on 96% of the fund’s holdings, with a very short lead time:

Current wallet (IFF fact sheet)

The average days to expiration for options is 17 days, and they are only a little out of the money at 0.4%. This translates to CEF having a two-week turnover period (approximately) for its options, and an uptrend that maxes out at 0.4% during that period.

The fund does best when the index rises less than 0.4% during each successive two weeks (options have a better chance of generating income in this scenario), and it does worst against the index when the S&P 500 posts large gains in a short sum. Of time.

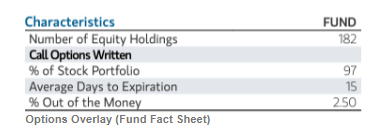

Portfolio managers have flexibility in the options chosen, but they focus on approximate two-week durations for the CEF, all while adjusting the “money” of the options:

Overlay recall previous article (author)

The above is taken from our last article in 2023, and we can see that while the average duration is still around 2 weeks in 15 days, the “percentage in the money” has changed from 2.5% to 0.4%. This change makes the fund more sensitive to increases in stock prices.

Active management plays a big role in the success of many mutual funds, and ETV has proven over the years its ability to adjust the delta of its options to the best combination of risk/reward calls.

Main risk factors

1. Hard landing

The biggest risk factor for a fund like an ETV is a “hard landing” scenario in the broader stock markets. The fund is closely correlated with SPY on the downside due to the low protection offered by written calls. A call option overlay functions primarily as a means of extracting premiums and paying dividends for the fund, rather than a tool for managing the fund’s downside.

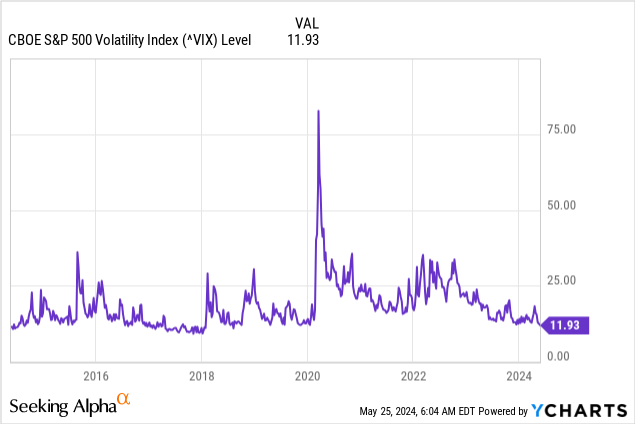

2. Permanent volatility shift

One issue in the last couple of years for many buy-write funds has been the shift to lower volatility:

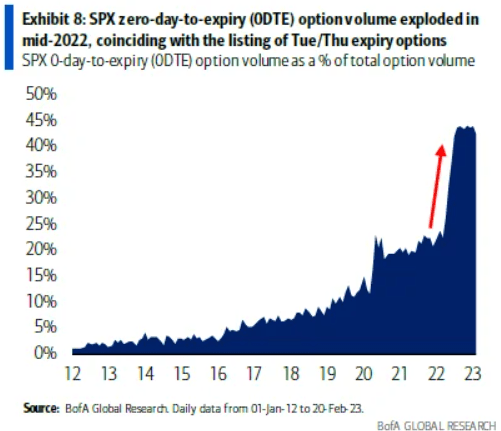

A lower VIX translates into lower option premiums, all else being equal. One market thought process is that the introduction of ‘0DTE’ options is responsible for the downward shift:

Size 0DTE (Bank of America)

After listing “0DTE” for every business day in 2022, volume exploded according to the chart above from Bank of America. ‘0DTE’s are now approaching 50% of the total options volume in the market.

While 2023 has seen very weak volatility, we have yet to see whether this is a permanent shift in the long term, or just a temporary shift. We haven’t seen a significant rise in the VIX since 2022, and given the current volumes of ‘0DTE’s and related products, it will be interesting to see how they will be affected when volatility actually rises.

Conclusion

ETV is a CEF for buying and writing stocks. The fund comes from the Eaton Vance family and has a very strong track record of turning stock returns into profits. The fund was negatively impacted by the low VIX environment in 2023 and the massive rally in stocks, factors that hampered its performance and caused the fund to become a discount to NAV.

2024 saw “volatility” in stock returns, a setup that helped the ETV track the performance of the S&P 500 more closely. Barring any unexpected negative shocks, ETV will continue to perform in 2024, with the overall setup favoring a continued slow rally in stocks with extended periods of range-bound movement. This macro picture is favorable for ETV, which should subsequently see a significant -7% discount to closing NAV. We hold the name and find the CEF attractive in today’s environment versus an outright buy of SPY.