Kutay Taner/Digital Vision via Getty Images

The obvious question investors face when the market is at or near all-time highs is what to do next. Momentum investors are likely to start buying aggressively, because that is their factor Choice is everything. For value factor lovers, there are a few possible steps, and one option is to venture outside the country to find discounts that suit them. For example, they may be exploring opportunities in a developed, resource-rich economy, and Australia immediately comes to mind. The country is a low-price-to-profit haven with huge amounts of iron ore, copper, natural gas and other resources. One exchange-traded fund that could be considered a convenient exposure to this treasure trove is the iShares MSCI Australia ETF (NYSEARCA: EWAA), which began in 1996 and It now has $1.66 billion in net assets.

However, as tempting as the premise seems, I am opposed to buying EWA at this point. There are some issues I see.

- First, economic growth in Australia has almost stopped, while disturbing signs have emerged that inflation remains too difficult to bring back to the desired level. This is either neutral or bearish for the Australian dollar, but clearly not bullish. The Australian dollar has been the main critic of the Electricity and Water Authority’s performance in the past.

- Second, EWA has a somewhat unconvincing track record, having underperformed developed world equities from the iShares MSCI EAFE ETF (EFA) over the past 10 years (June 2014 – May 2024) by 84 basis points in annualized return. It has also lagged the US market proxying with the SPDR S&P 500 ETF Trust (SPY) since its inception, resulting in higher volatility and significant downside holding.

Let’s review all of these in more depth below in the note.

Economic growth has stalled. HEmbarrassing hints from the Reserve Bank of Australia

It’s been a long time since I’ve discussed Australian stocks. A lot has changed since March 2021, as the narrative in both the country and the world has shifted from a post-pandemic recovery and expansion fueled by pent-up demand to its side effect, namely inflation. Inflation has yet to be tamed, while the economy is barely expanding.

Fortunately, at this point, the Australian economy is not contracting. just yet. But it grows anemic, if it grows at all. Confirming the latest GDP data provided by the Australian Bureau of Statistics on June 5, the nation achieved growth of 10 basis points in the March quarter, due to…

Domestic demand declined as increased consumer spending was offset by a decline in aggregate investment.

The market expected an improvement of 20 basis points.

Overall, the IMF’s World Economic Outlook (April 2024) forecast identifies only a 1.5% improvement in Australia’s real GDP in 2024, which is 20 basis points lower than the group of advanced economies, or 2.9 times lower than the group of advanced economies. Expected growth. For the Asia-Pacific region, it is 1.8 times lower than the growth rate of the United States

Returning to inflation, data published on May 29 show that the Consumer Price Index rose by 3.6%, beating market expectations by 3.4%. The reason behind this surprise was housing, among other things.

Compared with regulators in other advanced economies, the RBA has taken a slightly more moderate approach to taming inflation. It has already made more interest rate increases, with a total of 13 between May 2022 and November 2023. Meanwhile, the Fed raised interest rates just 11 times from March 2022 to July 2023, but in a more aggressive manner, with federal funds. The interest rate now ranges from 5.25% to 5.50%, while the official interest rate in Australia is only 4.35%. But the problem here is that further steps may be needed to get the CPI back on target. At a Senate hearing at Parliament House on 5 June, Reserve Bank of Australia Governor Michelle Bullock made the following comments:

If, for example, it turns out that inflation is starting to rise again, or that it has become more persistent than we think, and we are unable to lower it, we will not hesitate to act and raise interest rates again… Conversely, if the economy turns out to be much weaker than expected If this puts more downward pressure on inflation, we will look to ease.

This theoretical tightening may offer some support to the Australian dollar, which has performed somewhat sluggishly this year, similar to the euro falling 2.94% against the US dollar (euro down 2.45%), but combined with stalling growth, this may translate into A case of stagflation, perhaps not an outright one (for context, in 1975, inflation in Australia rose to 17.7% in March while GDP grew just 1.3% for the year), but a serious enough situation. To be interpreted by investors as a sell signal, which is a good thing neither for the national currency nor for the stock market. However, there are potential tailwinds, with copper demand being the primary one. Here, there are two main variables: demand from the semiconductor industry as AI scales up and the trajectory of the Chinese economy. That’s why I refrain from creating a bearish thesis for EWA, its counterpart Franklin FTSE Australia ETF (FLAU) which tracks the FTSE Australia Capped Index, or the Invesco CurencyShares Australian Dollar Trust ETF (FXA).

EWA returns: chronic underperformance, with FX among the detractors

Unfortunately, investing in Australian shares via EWA means consistently high volatility and poor performance. To illustrate this, let’s review the results achieved since its inception in 1996. To ensure proper context, I’ve added SPY and two advanced global equity ETFs, the iShares MSCI Japan ETF (EWJ) and the iShares MSCI Germany ETF (EWG). SPY was chosen as the benchmark. The period from May 1996 to May 2024.

| measurement | yeah | EWJ | Environmental Working Group (EWG). | spy |

| Beginning balance | $10,000 | $10,000 | $10,000 | $10,000 |

| The final balance | $71,636 | $15,254 | $47,932 | $132,408 |

| Compound annual growth rate | 7.26% | 1.51% | 5.74% | 9.64% |

| standard deviation | 21.94% | 17.89% | 23.41% | 15.51% |

| Best year | 68.13% | 60.88% | 66.64% | 33.48% |

| Worst year | -47.95% | -30.31% | -43.48% | -36.81% |

| Maximum withdrawal | -63.81% | -57.84% | -64.17% | -50.80% |

| Specific ratio | 0.33 | 0.05 | 0.27 | 0.53 |

| Sortino ratio | 0.48 | 0.07 | 0.38 | 0.78 |

| Standard correlation | 0.74 | 0.64 | 0.81 | 1 |

| Upside capture percentage (%) | 102.64 | 58.69 | 111.34 | 100 |

| Downside Capture Ratio(%) | 114.14 | 87.9 | 131.44 | 100 |

Data from portfolio visualizer

During that period, EWA underperformed SPY, resulting in much higher volatility. It has captured more upside, but also significantly more downside. The maximum drawdown was among the deepest in the group. However, it beat EWJ and EWG.

However, what if we shorten the period? For example, to December 2017 – May 2024, as its FLAU counterpart was created in November 2017. Here, I also added FXA.

| measurement | yeah | EWJ | Environmental Working Group (EWG). | Fxa | Flow | spy |

| Beginning balance | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| The final balance | $14,377 | $12,831 | $11,316 | $8,988 | $14,864 | $22,201 |

| Compound annual growth rate | 5.74% | 3.91% | 1.92% | -1.63% | 6.29% | 13.05% |

| standard deviation | 21.31% | 15.14% | 22.46% | 10.18% | 21.67% | 17.58% |

| Best year | 22.41% | 20.32% | 23.36% | 9.50% | 23.33% | 31.22% |

| Worst year | -12.02% | -17.72% | -22.20% | -8.85% | -10.16% | -18.17% |

| Maximum withdrawal | -31.36% | -28.85% | -41.66% | -22.77% | -31.70% | -23.93% |

| Specific ratio | 0.27 | 0.19 | 0.1 | -0.31 | 0.29 | 0.67 |

| Sortino ratio | 0.39 | 0.28 | 0.15 | -0.42 | 0.42 | 1.02 |

| Standard correlation | 0.84 | 0.81 | 0.86 | 0.71 | 0.86 | 1 |

| Upside capture percentage (%) | 85.87 | 57.73 | 85.1 | 24.67 | 88.7 | 100 |

| Downside Capture Ratio(%) | 112.6 | 82.05 | 127.96 | 56.05 | 113.9 | 100 |

Data from portfolio visualizer

As we can see, both funds underperformed SPY, capturing a lot of the downside but not much of the upside. Meanwhile, FXA had an annualized total return of -1.63%, meaning the Australian dollar was the main detractor of EWA and FLAU’s performance.

EWA wallet configuration

Tracking the MSCI Australia Index, EWA includes 58 stocks. This is a fairly heavy basket, with the 10 major positions representing 59.7% of net assets as of June 7. This is not unique to the Electricity and Water Authority. This is even typical for international ETFs. For example, the iShares MSCI France ETF (EWQ) and EWG also have more than half of their net assets allocated to just 10 key positions.

Seeking alpha

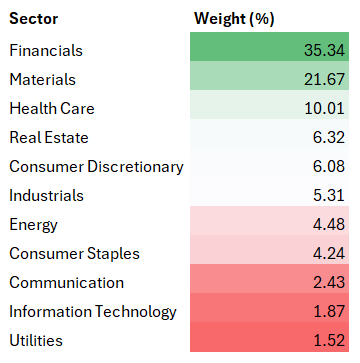

When talking about sector mix, financials take the top spot, with Commonwealth Bank of Australia (ASX CBA Index) (OTCPK:CBAUF) being the leading stock in the sector with a weight of 11.1%.

Created by the author using data from EWA

With a 10.5% YTD return, this stock is responsible for a meaningful share of EWA’s gains this year, along with National Australia Bank (ASX NAB Index) (OTCPK:NABZY), its fourth largest stock with a weight of 5.8%, Which has increased in price. By 14.2%. At the same time, BHP Group (BHP), a giant in the materials sector and its largest holding (with a weight of 11.97%), declined significantly, falling by about 14.5% on the New York Stock Exchange. Overall, relatively inexpensive (P/E of 18.56x according to its website), EWA has significantly lagged the high-tech SPY year-to-date.

Investor takeaways

EWA offers an impressive range of major Australian companies, the most important of which are banks. As past performance shows, EWA can deliver strong gains; For example, it beat the SPY every year from 2001-2007. In 2009, it outperformed the SPY by a whopping 41.77%. However, the 2000s were a lost decade for it, as it performed better than SPY only in 2010 and 2012. And the 2020s have not been easier, with the ETF only being ahead of the US leaders in 2022. I am skeptical of its potential and at this point, there are macro headwinds from slowing growth to persistent inflation that are worth addressing . There is also another problem inherent in most but not all international equity ETFs: the onerous expense ratio, which in the case of EWA is 50 basis points, in stark contrast to 9 basis points for FLAU. In this regard, the Hold rating is maintained.