Sisiriadigar

Investment thesis

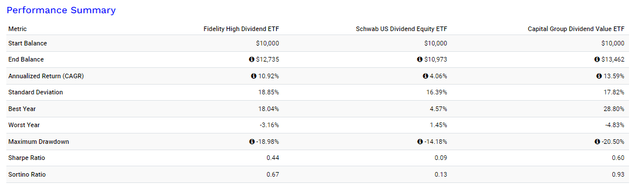

I checked last time Fidelity High Dividend Fund (NYSEARCA:FDVV) on February 27, 2024, where I listed a 3% dividend yield, low P/E, and high quality as reasons for my “Buy” rating. Since the initial upgrade On May 28, 2023, FDVV outperformed the Schwab US Dividend Equity ETF™ (SCHD(13.13% and roughly equivalent to the returns of the SPDR® S&P 500 ETF Trust)spy), which is an impressive accomplishment for a value ETF in a growth-friendly market.

Seeking alpha

Given these results, you might be concerned about buying at the top. While this is always possible, I remain comfortable with FDVV because it is well balanced across almost all of the fundamental factors it measures. In fairness, the forward P/E ratio is no longer as attractive as it was in February. However, it remains one of the most sensible large-cap ETFs on the market that provides enough income to meet dividends Investors and sufficient growth to participate in emerging markets. As a result, I’ve decided to maintain my “Buy” rating, and I look forward to discussing why in more detail below.

FDVV Overview

Strategy discussion

FDVV tracks the Fidelity High Dividend Index, selecting approximately 100 securities from the Russell 1000 based on three special screens:

- One-year trailing dividend yield (70%)

- One-year delayed dividend payout ratio (15%)

- One-year trailing earnings growth (15%).

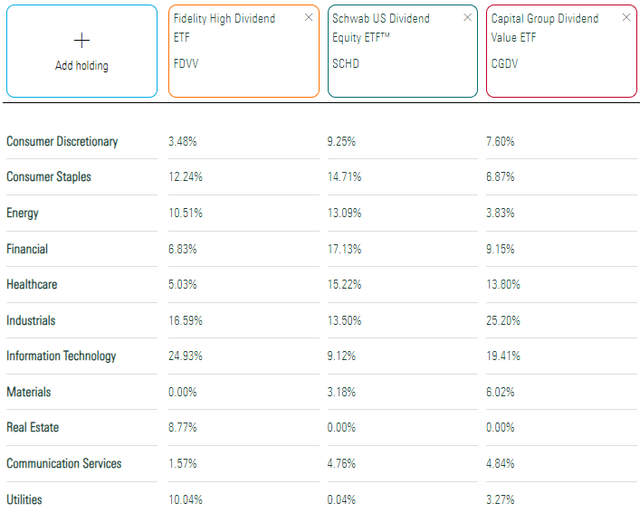

These screens are transparent, but the “proprietary” part relates to how the FDVV ranks securities compared to their sector peers. The result is a portfolio with a composition that overweights certain low-yielding sectors such as technology. This approach differs from the approach used by SCHD, which has 16% less technology exposure.

Morning star

I’ve also included sector exposures to the Capital Group Dividend Value ETF (CGDV) to benefit more aggressive value investors. Since March 2022, it has been the best performer of the three, with a total return of 34.62%.

Portfolio visualizer

Top Ten Holdings

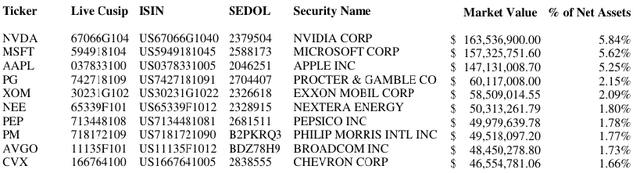

I’ve listed the top ten holdings of FDVV below, which total 29.69%. I expect you’ll be surprised to see Nvidia (NVDA), Microsoft (MSFT), and Apple (AAPL) at the top of the list, with trailing dividend yields of just 0.71%, 0.01%, and 0.50%, respectively. These will likely never be holdings in SCHD, which only selects from the top 50% of securities by dividend yield.

devotion

While this configuration is odd for a high-dividend fund, what’s even more significant is the index’s yield, which is 3.03%. After deducting FDVV’s expense ratio of 0.15%, net shareholders are 2.88%, 1.03% less than SCHD’s expected return of 3.91% but more than double SPY’s return.

Earnings growth analysis

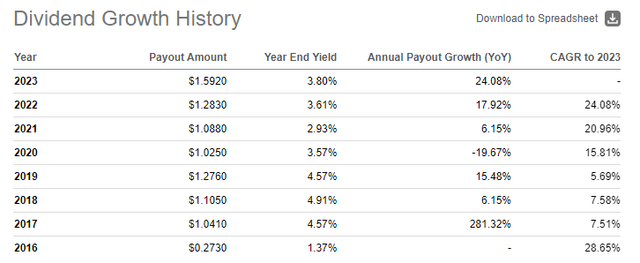

Before I get into the basics of FDVV, I want to address FDVV’s diminishing dividend yield. Ending 2020 at 3.80%, it is now 3.13% on a trailing-twelve-month basis, and my 2.88% estimate represents a further decline of 0.25%.

Seeking alpha

If what attracted you to FDVV in the first place were the annual earnings growth rates of 24.08% and 17.92% from 2023 and 2022, I suggest you move on, because that won’t happen in 2024. But before you do, understand that the decline in The ETF’s dividends do not mean that its constituents reduced dividend payments. Consider how FDVV’s share price is up 21% over the past year ($38.51 to $46.71), and to maintain the yield, 21% earnings growth is needed. This is neither possible nor responsible in an environment where estimated earnings growth rates are mediocre.

Fundamental analysis FDVV

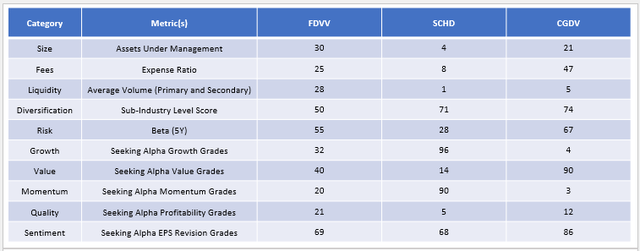

Factor Ratings vs. Large Cap ETFs

I want to provide a brief review of the factors to see how FDVV compares to other large-cap value ETFs, a category that includes 98 funds. As shown, the FDVV is well balanced across the board. Its weakest rating is Sentiment (#69/98), while SCHD and CGDV are relatively weak in terms of Growth and Value, respectively.

Investor Sunday

This table also helps explain the latest results. CGDV outperformed because it scored a good 4/98 in growth, while SCHD underperformed for the opposite reason. Using performance charts to identify the best ETFs is tempting, but it’s actually a futile exercise. The bottom line is that CGDV will perform well in growth markets, SCHD will perform well in value markets, and FDVV is appropriate if you are unsure which factors the markets will favor going forward.

FDVV Basics by Company

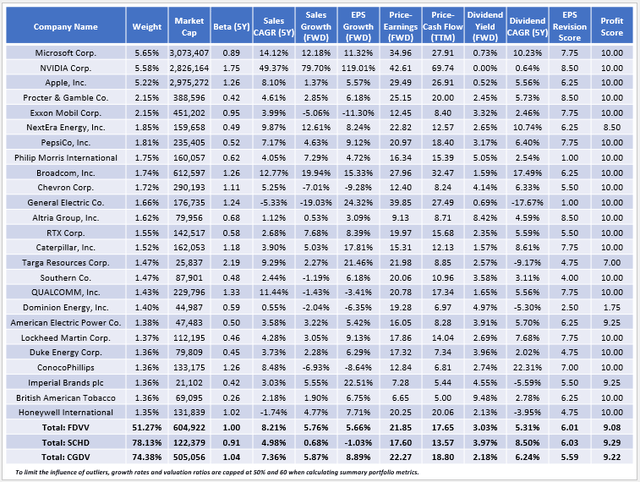

The following table highlights selected key metrics for FDVV’s 25 largest holdings, totaling 51.27% of the portfolio. I have also included summary measures for SCHD and CGDV in the bottom rows.

Investor Sunday

Here are five notes to take into consideration:

1. FDVV’s five-year weighted average beta is 1.00, putting it higher than SCHD but close to the category average of 0.98. Looking at holdings, Nvidia, a new dividend payer, is a major contributor to this number, which is why FDVV will be a little riskier going forward. according to Portfolio visualizerThe historical beta since January 2017 was 0.96.

2. Nvidia enhances risk, but also contributes to the fund’s balanced fundamentals. In particular, analysts expect 79.70% and 119.01% growth in sales and earnings per share next year, which they put at 50% when accounting for portfolio growth rates of 5.76% and 5.66%. I highlighted these metrics because growth rates are crucial for DGI investors. Without sufficient growth, there is no way for a company to grow dividends responsibly without cutting costs or increasing its dividend payout ratio. This is what has happened to SCHD over the past two years, and we must also monitor FDVV growth rates to avoid falling into the trap.

3. You’re probably wondering how SCHD has been able to grow its dividend in the double-digit range for so long while maintaining a high dividend yield. The reason is that earnings growth rates were astronomical for almost all large-cap funds several years ago. Today, this is not the case. To illustrate this, I backward-calculated the historical dividend growth rates for all three ETFs mentioned above using data from Seeking Alpha.

Investor Sunday

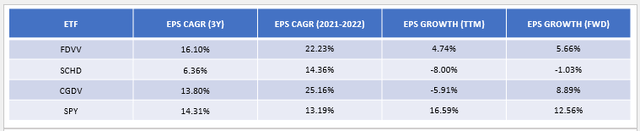

SCHD’s annual dividend growth rate for 2021-2022 was 14.36%, better than the 13.19% growth rate of the SPDR S&P 500 ETF.. As a result, it has been able to keep pace with SPY from a total returns perspective and grow dividends at a double-digit rate. However, SCHD’s earnings growth was -8.00% over the past year compared to 16.59% for SPY, and looking ahead to next year, the consensus estimate remains negative. In short, SCHD has moved from a value play with strong growth potential to a value-only play. Unlike before, a company will only do well if growth stocks lose popularity.

4. FDVV trades at a roughly 20% discount to forward earnings compared to SPY (21.95x simple weighted average, 16.58x harmonic weighted average). However, it is at the high end for the large-cap value category, and that is my main criticism today. In February, FDVV had roughly the same earnings per share growth (5.63%) but was trading at 19.52x (17.33x) of forward earnings, so there is a greater risk that FDVV is now overvalued.

Meanwhile, FDVV’s Value score of 40/98, derived from sector-adjusted alpha factor scores, suggests it’s not too bad of a value play. In other words, FDVV does a good job of selecting value stocks in each sector. However, if tech stocks collapse, I doubt FDVV will provide much downside protection. Stocks like Nvidia are easy targets, especially if earnings growth rates don’t materialize.

5. The return on CGDV components is 2.18% on average, and after subtracting the fund’s expense ratio of 0.33%, net shareholders should be 1.85% at current prices. It’s not an income play, but its estimated earnings growth rate of 8.89% is the best of the three and No. 3/98 in its class. This metric, its 1.04 five-year beta and 22.27x forward earnings valuation reinforce my previous conclusion that CGDV is a more aggressive value ETF than FDVV and SCHD. It has performed well recently, but I expect it to underperform in a market downturn.

Investment recommendation

The average estimated EPS growth rate for S&P 500 stocks yielding less than 3% is 9.92%, but only 0.53% for those yielding more than 3%. This simple statistic tells me that high-dividend investors should be more careful, because they risk missing out on a growth-fueled market upside for only marginally higher income. As I mentioned earlier, consistent growth for high dividend stocks wasn’t a problem several years ago, but circumstances have changed, and we must adapt.

FDVV solves this growth problem by including low-yielding stocks like Apple and Nvidia. The expected dividend yield of 2.88% is about 1% lower than SCHD’s, but Benefit is a much more balanced portfolio and ranks near average or better in terms of diversification, risk, value, growth, momentum, quality and sentiment. By avoiding a weak rating in any category, FDVV is well prepared for any market environment, and for these reasons, I have decided to revert my rating to Buy. I hope you find this information helpful, and I look forward to answering your questions in the comments section below.