Photos by Tang Ming Tong

Cohen & Steers Closed End Opportunities Fund (New York Stock Exchange: FOF) takes a box of box approach. The fund is well diversified across sectors and can be a decent option for less active, income-oriented investors who don’t want… To spend a lot of time managing their own portfolio of closed-end funds.

There are times when FOF trades at a discount, and you get a double discount, since FOF primarily invests in CEFs that also trade at a discount to NAV.

But on the downside, of course, you pay two sets of fees. FOF charges an expense ratio of 0.95% on top of the fees charged by the underlying funds. FOF is a non-leveraged fund, so at least there are no interest expenses for getting leverage.

FOF currently invests in 96 properties. And in the prospectus it says so They generally look for funds with a market capitalization greater than $200 million, and an average daily trading volume greater than $750,000 per day.

But there are several reasons why owning a FOF may be less than optimal compared to managing your own portfolio of mutual funds:

1) FOF may not take full advantage of corporate actions (e.g. tender offers, rights offers, etc.) that may occur in underlying closed-end funds.

2) FOF may not take full advantage of discount DRIP plans, such as those offered by Cornerstone or PIMCO funds, which often trade at a premium.

3) If you hold FOF in a taxable account, there are fewer opportunities for tax loss harvesting, compared to owning the underlying funds directly.

4) FOF typically invests about 10% of the portfolio in municipal bond CEF funds. If you hold FOF in an IRA or other tax-deferred account, you will waste the tax-exempt interest of municipal bonds and will eventually have to pay taxes on the interest earned when you withdraw the money from your IRA.

5) About 10% of the FOF portfolio is invested in low-cost index ETFs, such as VOO, SPY, and others. Effectively, you’re paying Cohen & Steers an extra 95 basis points per year to own these low-cost index funds that you could easily buy yourself.

Distribution policy

FOF uses a monthly managed distribution plan. It currently distributes $0.087 per share on a monthly basis. They have been paying this amount every month since October 2016! Before that, the fund paid a quarterly distribution of $0.26.

Below are the estimated distribution sources for the first five months of 2024. Note that the majority of distributions are a return of capital, so FOF can be an appropriate holding for a taxable account.

Source of distributions (FOF website)

Portfolio management team

- Douglas Bond: Head of closed-end funds. 43 years of experience. Mr. Bond holds a BA from Hamilton College and an MBA from New York University.

- Jeffrey Palma: Head of Multi-Asset Solutions. 28 years of experience. Mr. Palma holds a bachelor’s degree from Rutgers University and an MBA from Columbia University.

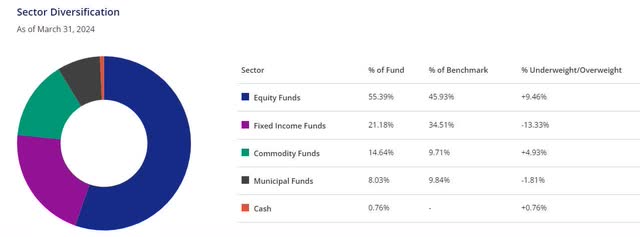

FOF portfolio sectors

FOF portfolio sectors (FOF website)

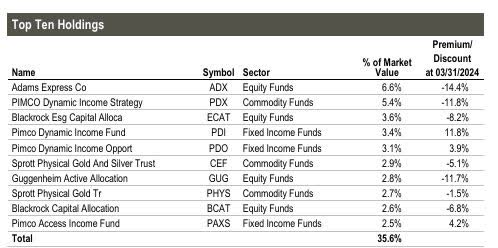

Top Ten Holdings

The top ten holdings as of 03/28/2024 were all closed-end funds. Most are trading at a discount to net asset value, but three of Pimco’s funds were trading at premiums. The fund also has a position in the Cornerstone Strategic Value Fund (CLM), which did not make the top 10.

I sent an inquiry to Investor Relations asking whether the fund participates in PIMCO or Cornerstone’s discounted DRIP plans, but have not yet heard back from them. I suspect they are not involved in these plans.

An active investor who owns the underlying funds directly can participate in PIMCO or Cornerstone DRIP plans, selling as many shares as needed to generate the desired income. This would add significant alpha compared to simply receiving dividends in cash without a discount.

Note that PIMCO’s Dynamic Income Strategy (PDX) is still treated as a commodity fund. This seems outdated. On November 21, 2023, the fund was renamed from the PIMCO Energy and Tactical Credit Opportunities Fund. PIMCO has changed its name, ticker symbol, investment objectives and composition of portfolio managers. Right now, PDX is really more of a fixed income fund than a commodities fund, but it does have a “slant” to energy in some of its underlying investments.

FOF Top 10 Collectibles (FOF Fund Website)

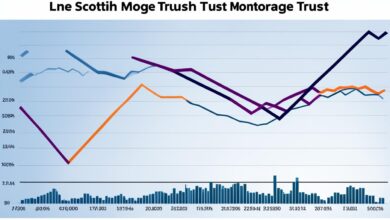

Total return performance

Below are FOF’s trailing total return price and NAV performance history compared to peers in Morningstar’s Moderate Allocation Category.

|

FOF price performance |

Perform FOF navigation |

Moderate Allocation Class (NAV) |

Percentile rank in category (NAV) |

|

|

2015 |

-9.03% |

-7.47% |

-6.68% |

83 |

|

2016 |

+16.78% |

+14.43% |

+12.41% |

15 |

|

2017 |

+23.41% |

+16.21% |

+15.33% |

29 |

|

2018 |

– 9.45% |

-9.67% |

– 8.03% |

72 |

|

2019 |

+31.37% |

+26.67% |

+26.43% |

50 |

|

2020 |

+1.60% |

+2.37% |

+3.88% |

50 |

|

2021 |

+28.40% |

+19.38% |

+19.65% |

50 |

|

2022 |

– 22.59% |

-18.17% |

– 8.98% |

100 |

|

2023 |

+18.20% |

+12.36% |

+4.30% |

20 |

|

YTD |

+9.37% |

+11.00% |

— |

— |

Source: Morningstar (as of June 10, 2024)

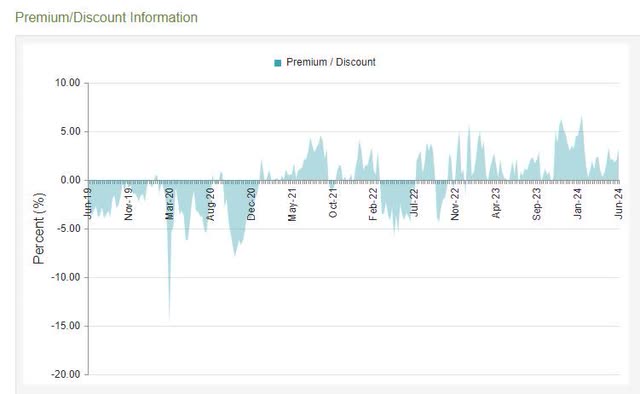

FOF – five-year discount history

FOF discount history (cefconnect)

Fund basic information

Cohen & Steers, Inc. Closed End Opportunity Fund.

Bar: (FOF) Navigation Bar: XFOFX

- Establishment date: November 20, 2006

- Total investment exposure: 317.5 million

- Total combined assets: 317.5 million

- Effective Leverage: None

- Basic expense ratio = 0.95%

- Premium = +2.00%

- Average installment for 6 months = +2.69%

- Annual distribution rate (market price) = 8.77%

- Current monthly distribution = $0.087

- Annual distribution = $1,044

- Number of holdings = 96

Concluding remarks

The average daily trading volume at FOF is about 50,000 shares or about $600,000. But the required bid spread is usually about four cents and can be as high as 10 cents. If you want to buy FOF, I definitely recommend using smaller size limit orders.

I never owned FOF when it traded at a higher price. But I’ve owned them occasionally when they were trading at a 5% discount or higher. This can be a very convenient way to get quick exposure to a basket of closed funds.

I have fond memories of FOF from 2010 when we had the “flash crash” on May 6, 2010. During the trading day, there was a $1 trillion flash crash that started around 2:30 PM and lasted about 20 minutes. The Dow Jones Industrial Average fell about 1,000 points, or 9%, within minutes, but recovered most of the losses by the end of the day.

During the flash crash, I was looking for something to buy that would be reasonably safe without having to worry about individual security risks. At the time, FOF was trading at a discount of about 6%. I started converting dollar cost averaging to FOF using 100 lot stock market orders during crazy market turmoil. At the low point, FOF fell more than 15% during the day, but by the end of the day it recovered most of its losses and closed down about 4%. Most of the intraday trades were very profitable.

Right now, I wouldn’t recommend owning FOF at a 2% premium. I think an active investor could do better by owning some money directly in a FOF portfolio, for the reasons I mentioned above. But for less active investors who want to own FOF, I recommend using their dividend reinvestment plan as long as the FOF is trading at a premium.

The FOF DRIP plan uses the following rule to determine the purchase price:

The number of shares to be issued will be calculated at a per share rate equal to the greater of (i) net asset value or (ii) 95% of the closing market price per share on the date of payment.

So, if FOF were to trade at a premium of 5% or higher, you could reinvest the dividends at a 5% discount to the market price. At the current premium of about 3%, you can reinvest the dividends at NAV, or roughly a 3% discount to the market price.

The FOF Prospectus contains the following clause describing the possibility of converting the FOF into an open-ended fund.

Open fund transfer.

The common stock has been approved to be listed on the New York Stock Exchange Exchange, subject to notice of release, under symbol “FOF”. The Fund’s statute stipulates this(commencing for a period of five years from the date of this prospectus) if the Fund’s common stock closes on New York stock Exchange at an average price over 75 consecutive trading days at a discount of 7.5% or more from The average net asset value of the Fund’s common shares during this period, the Fund will invite shareholders A meeting for the purpose of voting on the proposal to transform the fund into an open-ended fund by amending the law Fund’s statutes

Because of this condition, I think FOF would be an interesting buy if the discount returns to 7.5% or more. Until that happens, I think more active investors would be better off using a fund duplication strategy or choosing their own portfolio of closed-end funds.