Editorial by Jarmo Pironen/iStock via Getty Images

Dear readers/followers,

I haven’t covered Fortum publicly or on Seeking Alpha’s free site for some time – but I have covered it in our private investing community as well as in the chat, where I’ve been present Clear on my bullish stance on Fortum Oyj (Otkbk:fwjkf) (OTCPC: fujsi).

Fortum has been trailing the lows for some time now, but when the company momentarily approached less than €10.5 per share for the natives, that’s when I dug in deep and bought over 1.5% in both my trading account and my own account. “That bet paid off.” Aside from the double-digit covered dividend yield, I’ve also been able to enjoy significant capital appreciation as the company begins to return to normal.

Fortum is a BBB+ rated terminal utility with operations throughout Scandinavia. It has witnessed significant fluctuations over the past 10-20 years in their operating profits, quite unlike most utilities, and the reasons for this are many – however, Russia is one of those reasons.

In this article, I will provide an update regarding the latest quarterly results, Q1 2024, and see what kind of future prospects we can see for Fortum. Some are understandably dubious – are they right?

lets take alook.

Fortum – What upside do we currently have, and what upside do we expect for the company

So, with the quarterly rise we’ve seen in the share price, the results must have been good, one might think – and in fact, the results have been very good for the company and where it’s headed.

First, Fortum saw a strong upgrade in its credit rating – now BBB+ as reported, and ongoing arbitration proceedings have been taken against the Russian Federation. Now, this last part I consider to be kind of news here – because I doubt that Russia will really care about this outcome, and simply do what it wants to do – as it has done for some time now.

Perhaps the biggest positive outcome was the very good results despite of Overall energy prices decline across the Nordics, which have been high for some time here.

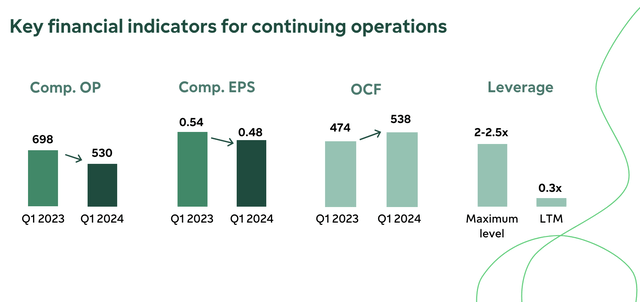

Fortum IR (Fortum IR)

What you’re seeing here for Fortum is a very strong FCF for Consumer Solutions and Operations, where the only decline really came from the generation segment. Lower working capital was another impact here, and although EBITDA was lower overall, leverage saw significant improvements due to lower net financial debt. Here we also find the reason for the improved credit rating. Find me another company with that kind of LTM leverage of 0.3x – there’s not many, if any, that I know of with that kind of size, scale, and operations.

Lower energy prices are associated with a warmer year. Energy prices have fallen in the Nordic countries, gas prices have fallen, and coal prices have fallen somewhat as well. Spot prices have moved sideways, with futures markets weak. Trends that led to higher prices, such as the 890/MWh peak during daily pricing, have subsided here. This was also supported by lower gas prices.

Overall, I did fortum Less resultsbut a Better quality of results. This is also why I’m fairly positive on the stock, and why I don’t think the somewhat bleak outlook is necessarily right here (more on that later in the review). The only real reason Fortum is actually down is because of the lower realized energy price, and there’s not much Fortum can do about that.

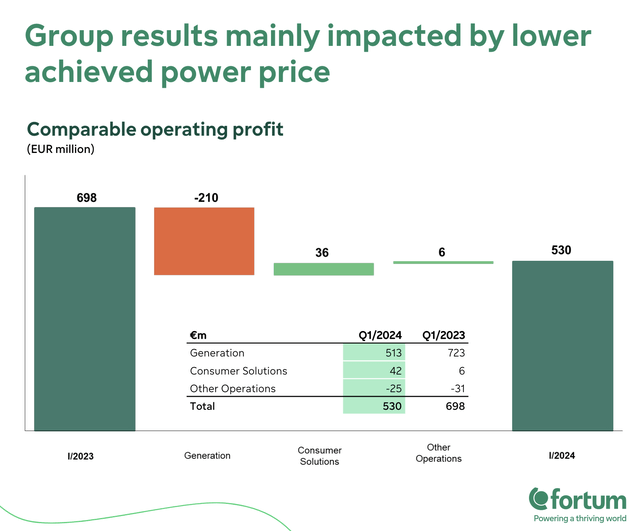

Fortum IR (Fortum IR)

Fortum still has low overall leverage, with strong liquidity and good maturities. There will not be huge maturities in terms of bonds until 2026-2029, as the next few years will bring only a few loans much less than current liquidity. The company’s current liquidity reserves stand at over €8.1 billion, compared to total borrowings of €5.7 billion as of this time, with an average interest rate including derivative hedging of 4.4%. It’s not the best in its class, but it’s certainly not alarming by any means.

Fortum is a mixed bag at the moment. The Russian cases are still backlogged, but if we focus on what actually remains, and remember that Uniper is now gone from the company and Fortum is focusing on reducing fixed costs, there are a lot of positives here.

Current estimates suggest a reduction in fixed costs of €100 million per year until the end of -25 at a full operating rate from 2026 onwards. Current estimates for CapEx including maintenance are approximately €550 million for the year, with a total of €1.7 billion between 2024-2026. This is by no means a cause for concern or something the company can’t handle, given the amount of cash it already generates. The company is still manipulating energy prices, and when they fall as they did last quarter, it is expected to impact overall results, as they did. However, Fortum has hedges in place regarding its district heating business and some renewables, such as Pjelax and other farms and assets that become available for use. This, by the way, is the largest wind park owned by Fortum, and the third largest wind park in the whole of Finland, with commercial operations starting as early as July this year.

At company-wide EBITDA of €622 million during the quarter, that still delivers a run rate of more than €2.4 billion in EBITDA each year.

Risks, concerns and things you should be aware of?

The Finnish state is still a very strong stakeholder in Fortum, but has recently announced that new ownership policy documents will be coming in the near term – so we are waiting for Fortum to comment on the impact of this, and see what this brings to the evaluation.

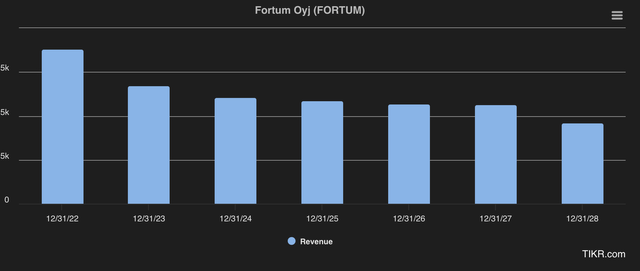

And this is important here because, and I want to be clear, it’s very clear to me that Fortum will see its revenue decline over the next few years – small declines at first, but declining nonetheless – and I’m not the only one who expects such a decline to decline at this time. These are the forecasts through 2028E from S&P Global.

Fortum Revenue Forecast (TIKR.com)

There are some Uniper, some Russia, and some other moving parts in this estimate. EBITDA is not expected to decline in the same way, although it still sees a moderate decline to the €1.5 billion level, but never below that level. Again, earnings quality is likely to rise, and we could see an EBITDA margin of 30% within a few years. Quite simply, revenue numbers will decline as the company moves from quantity to quality in generating sales, with a normal net income margin of 17-18% compared to 16% at this time, with more than 18% free cash flow margins (Paywalled TIKR link .com).

I actually expect earnings to decline as well. I expect a cut next year, in 2026, and for the cuts to stop there, back to the €0.8 per share level, which would put my YoC over time at around 8%. This would, depending on the payout policy, maintain the integrity of the company’s earnings while continuing to provide good returns to shareholders.

However, I bought Fortum very cheaply, and I can clearly say that just like the last time I sold Fortum at over €20 per share and made a nice profit, I’m willing to sell this time too – and not at €20. / Share this time.

Fortum – For me, the valuation dictates a ‘hold’ here, but rotation at the correct valuation, and a ‘buy’ below €12 per share

Fortum remains a strong play at this time if it can weather the decline in earnings that is likely to occur over the next few years. The company has prepared well for this by improving its asset base, leverage and credit rating. Long-term debt is now below 29%, which for an asset-heavy conservative player like Fortum is above the solidity level, which tends to be closer to 40% to 50% given how conservative it is. The company now has a market capitalization of €12.5 billion, with a dividend yield of more than 8%. My YoC is over 10% as of now, but will likely decrease on a future basis.

First, we look at other analysts. Fortum’s targets include a range of €11 on the low side to €18 on the high side, and that’s actually a range I can get into. The company’s average from 15 analysts is €13 per share, and if you’re looking for double-digit upside, again, that’s a target I can get on board with. The company’s “buy” recommendations decreased significantly. About 7 months ago, 13 out of 15-16 analysts had it at ‘buy’ or equivalent. Now it’s down to 4 out of 15, since the price is around €14.2.

There are those who would say it’s time to “leave” Fortum behind for greener pastures. I don’t think this is the case. I’d say that even if the company falls in the short term, Fortum has the potential to outperform and deliver better than the market expects. Not only am I saying this, this is the actual statistical trend. On a two-year basis, the company beat estimates by more than 20% 30% of the time (Paywalled FAST Graphs Link).

Is this likely to happen again? Some possibilities include positive demand in Russia (unlikely in my estimation), better-than-expected performance in power generation (not unlikely), and better overall operating efficiency, leading to bottom-line improvements. This last point I also consider possible.

With all of these improvements, I consider the company a “hold” with a breakout point of 14-15x EPS on a forward basis. For 2025-2026E, this amounts to around €13 per share, meaning the company is now ‘held’.

thesis

- Good facilities are rare when looking for undervalued companies. Fortum comes with its own set of challenges to consider before investing. However, few people would argue that the company offers a fundamentally safe investment opportunity with an attractive return. The question becomes whether one wants to maintain a very low potential for overall capital appreciation, beyond attractive profits.

- Finnish companies generally tend to have an even higher total return than other Nordic companies. My stake in Fortum is a stable stake, and I don’t intend to dispose of it unless we see prices above €15-€16 per share.

- Investors should consider Fortum if they want international energy/utility exposure coupled with attractive yield, currency diversification. However, after all that, Fortum has returned to my portfolio and is now over 1.5% in both business and personal portfolios on a cost basis of less than €11 per share.

- However, given the current pricing trends here combined with expectations, I would say the company is now ‘held’ and give it a price of €13, with a discount of around €15-16.

Remember, all I care about is:

- Buy undervalued companies – even if that devaluation is minor rather than staggeringly massive – at a discount, allowing them to normalize over time and reap capital gains and dividends in the meantime.

- If the company goes beyond normalization and goes into overvaluation, I take the gains and roll my position into other undervalued stocks, repeating #1.

- If a company is not overvalued but is hovering within fair value, or falling below its true value, I would buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash flows as defined in #1.

Below are my criteria and how the company meets them (in italics).

- This company is all about quality.

- This company is fundamentally safe/conservative and well managed.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a high enough realistic upside, based on earnings growth or multiple expansion/retracement.

I don’t consider Fortum cheap or interesting enough at this price to “buy”, but I would consider it a price below €12 per share. For now, this is “waiting.”

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.