duuuna/E+ via Getty Images

introduction

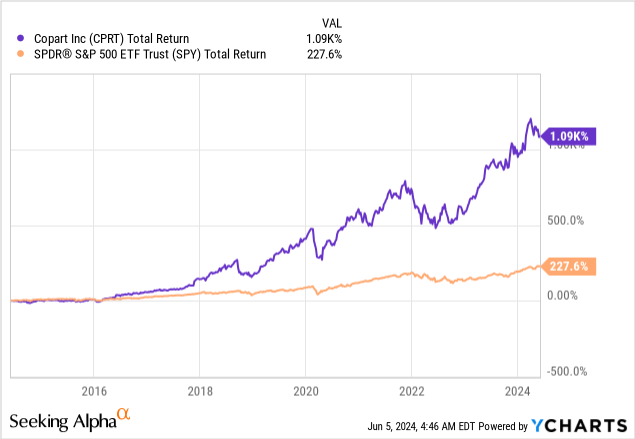

On October 3, I wrote an article entitled “Copart: Top notch boat I buy on weakness.”

Well, it didn’t go as I expected.

since then, Copart (Nasdaq: CBRT) Shares rose 24%, bringing the 10-year return to a staggering 1,090% – More More than 4 times the return of the S&P 500!

What we’re dealing with here is one of America’s biggest success stories.

Copart, which went public in 1994, was founded by Willis Johnson.

Johnson, who received a Purple Heart for his tour in Vietnam, bought a junkyard in 1972. The operation turned into a publicly traded giant with a market value of more than $50 billion, making him one of the richest people. Americans, where the Copart president still owns 5.7% of the company he founded.

When I look back, I think My success is partly due to the lessons my father taught me, and partly to God’s hand guiding me along the way. I also think a big part of it had to do with the fact that it never occurred to me that what I was doing might not work. I never thought I couldn’t do it. Some might call it trust. – Willis Johnson

In this article, I’ll take a closer look at the company, update my thesis, and explain how I approach a company that likely has a very bright future ahead.

So lets get to it!

The ideal business model for growth

Headquartered in Dallas, Texas, Copart operates in 11 countries, including the United States, Canada, the United Kingdom, Brazil, Ireland, Germany, Finland and others.

However, since more than 80% of its revenue came from the US last year, this is the main market to focus on.

So what does the company do?

Since it all started with a junkyard, we can assume that the current business still has something to do with old cars.

This is correct.

Copart has become a leading provider of online auctions and vehicle remarketing services.

Essentially, the company plays a major role in recycling and reusing vehicles, spare parts and raw materials globally.

This is not only profitable, but it is also a way to add to sustainability.

Vehicles that pass through the Copart system are often recovered, cannibalized for parts, or scrapped for raw materials.

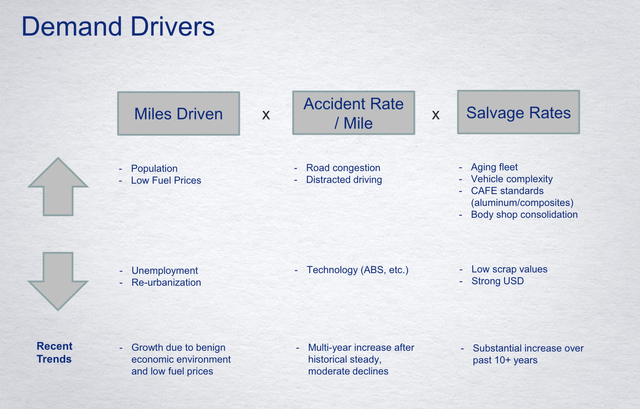

As the company’s 2016 overview shows, demand drivers are a combination of the following factors:

- Total miles traveled: Affected by population growth, fuel prices, employment, and urbanization.

- Accident rate: The more accidents there are, the greater the need for scrap services and new parts.

- Rescue rates: Affected by fleet ages, vehicle complexities and related factors.

Please note that the bull/bear drivers after eight years have changed.

Copart

Eight years later, the bull is no weaker. Despite falling fuel prices, population growth remains strong (supported by mass migration), re-urbanization has seen people move to rural areas (very optimistic), and road congestion remains a problem.

Furthermore, the aging fleet is becoming a much bigger problem (also rising).

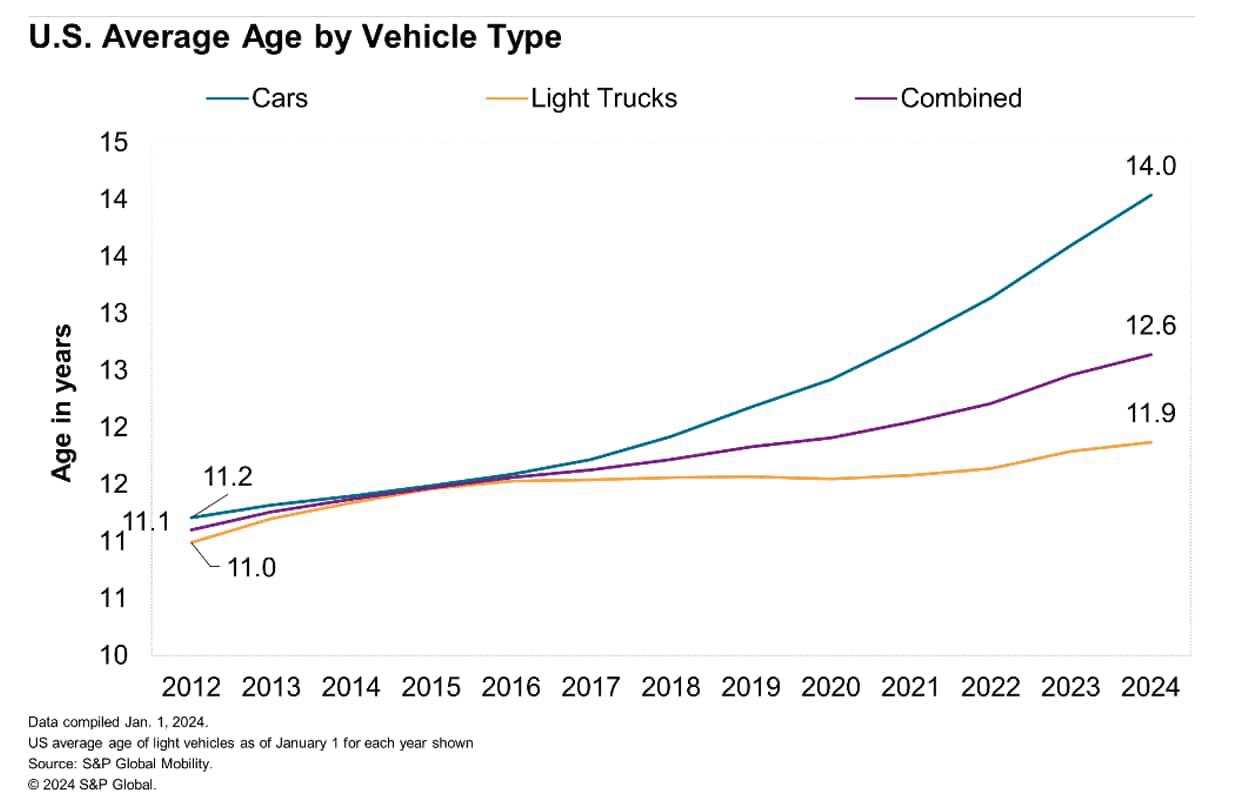

As I wrote in a recent article, the average age of cars on American roads is now 14 years. Including younger light trucks, the overall average age is 12.6 years – a new record!

Standard & Poor’s Global

Here’s what S&P Global, which published the chart above (emphasis added):

This continues Improving business opportunities for companies in the aftermarket and automotive sector in the United Statesas repair opportunities are expected to grow along with the age of the vehicle.

“With average age growth, More vehicles are entering the main range of after-sales serviceusually from From 6 to 14 years“With more than 110 million vehicles in that sweet spot — roughly reflects 38% of the fleet On the road – We expect continued growth in the volume of vehicles in that age group to rise to a level It is estimated at 40 percent until 2028” – Standard & Poor’s Global

Returning to Copart, the company has a number of services for vehicle sellers, including insurance companies, banks, charities and individuals.

Their primary sellers are insurance companies that need to dispose of vehicles damaged by accidents or natural disasters.

Buyers are typically vehicle dismantlers, rebuilders, and used vehicle dealers/exporters.

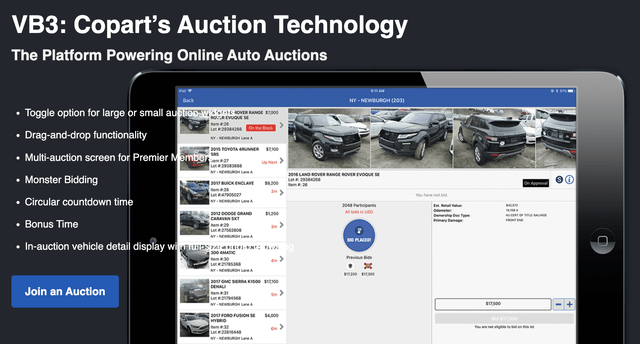

It has auction platforms that support online sales to scale its operations more effectively. The Virtual Bidding System (“VB3”), for example, aims to optimize the selling price and keep administrative costs low.

Copart

Furthermore, the company offers a wide range of related services, including residual value estimates (Copart ProQuote), machine learning to improve seller auction decisions (IntelliSeller), and others.

Furthermore, and this is a big deal, the company owns almost all of its land, which has reduced inflationary pressures due to the absence of significant rental costs.

As I have highlighted in the past, we expect our capital allocation strategy to enable Copart to fully focus on delivering differentiated products and services. To achieve this goal, over the past 12 months we have deployed more than $540 million across our real estate, leasing and technology portfolio. Today, our global portfolio of approximately 19,000 acres of third-party vehicle storage space, a robust fleet of transportation assets and more than two decades of virtual auction technology development are the foundation of what truly sets Copart apart. – CPRT 3Q24 earnings call

Personally, I like for companies to fully own strategic assets, as it adds a real estate-like aspect of value. This is also one of the reasons I bought Old Dominion Freight Line (ODFL), which owns more than 90% of its less-than-truckload service centers.

However, the market seems to like this business model too, as its stock price has risen more than 1,000% over the past 10 years.

So, what does this mean for investors? What do the numbers tell us?

Risk/reward after a 1000% rise

In light of secular tailwinds, the company continues to perform well.

In the third quarter of fiscal 2024, the company reported a 6.8% increase in U.S. insurance volumes, driven by a recovery of overall loss frequency to pre-pandemic levels.

According to the company, this recovery is supported by falling prices for new and used vehicles combined with rising repair costs, making it more economically attractive for insurers to total vehicles rather than repair them.

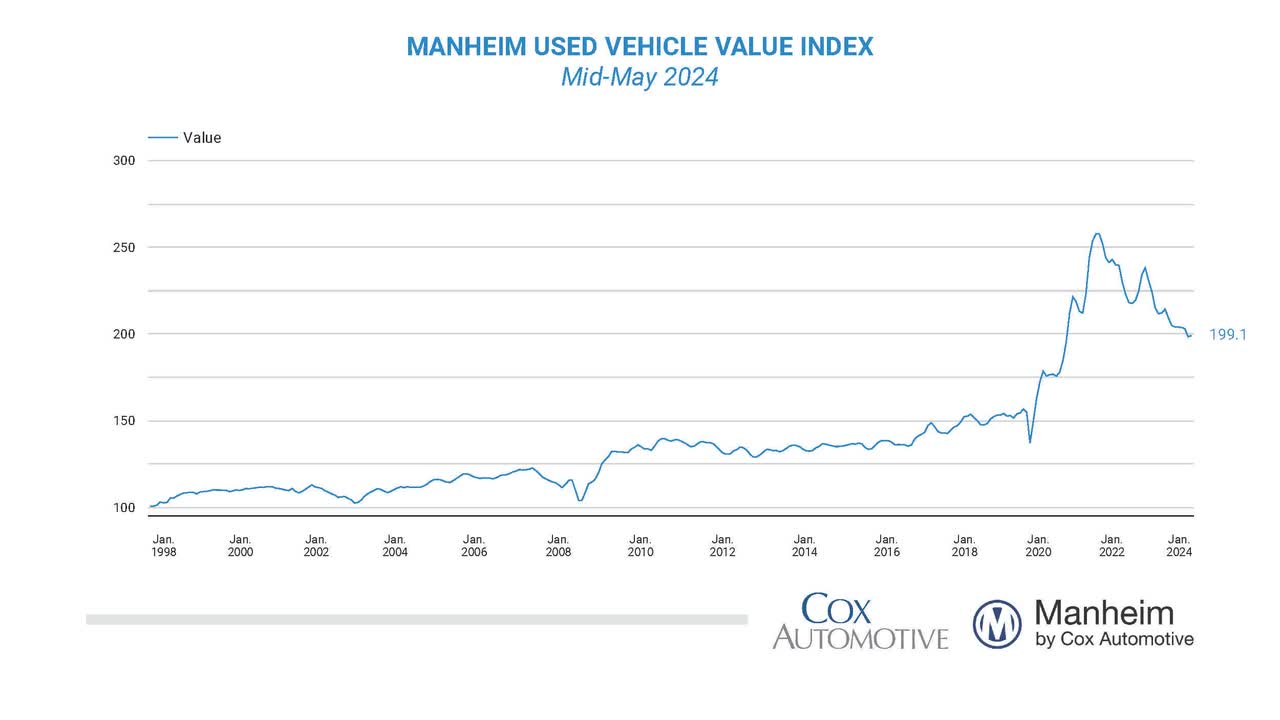

Mannheim

Meanwhile, the total loss frequency was 21.1% in the first calendar quarter of 2024. This is 150 basis points higher compared to the same quarter of the previous year.

Furthermore, Copart’s non-insurance business segments have shown promising growth trends.

- The Blue Auto business, which serves banking, financing, fleet and leasing partners, saw year-over-year growth of approximately 24%.

- Dealer sales volumes, handled through Copart’s dealer services and NPA, increased unit volumes sold by approximately 18%.

- Overall, U.S. auto and uninsured dealer volume, excluding low-value and wholesale units, saw a 19% year-over-year increase.

Furthermore, the company has expanded its capabilities to better respond to natural disasters, including optimizing teams, logistics and real estate to achieve maximum capacity.

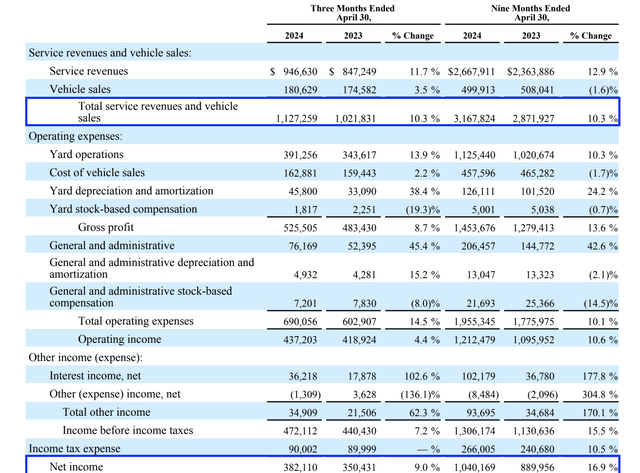

Furthermore, looking at the bigger picture, total unit sales rose 11% in the fiscal third quarter, supported by higher market share.

Global revenue rose 10% to $1.13 billion. This helped the company boost net income by 16.9% to $382 million.

Copart

The company is also highly efficient when it comes to generating cash.

On top of generating a 34% net income margin (the S&P 500’s net profit margin is 13%), it generated $408 million in free cash flow from $496 million in operating cash flow and $382 million in net income.

It also helps that the company has $4.3 billion in liquidity, including more than $3 billion in cash and investments.

This year, analysts expect the company will end up with $1.6 billion in net cash, which means more cash than total debt.

Speaking of expectations, using the FactSet data in the chart below, analysts expect EPS growth to remain high.

After an expected increase this year of 14%, 2025 and 2026 are expected to witness growth of 13% and 17%, respectively.

Quick charts

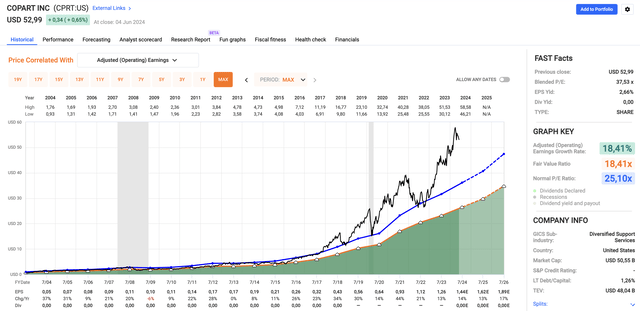

The bad news is that a lot of the growth is priced in, with CPRT trading at a mixed P/E ratio of 37.5x.

This is a mile higher than the company’s normal P/E ratio of 25.1x, giving the stock a fair price per share of roughly $48 to $50, just below the current price.

Although I think a premium is justified to reflect favorable business conditions, I’m not a fan of paying nearly 38 times earnings in an environment rife with potential demand risk.

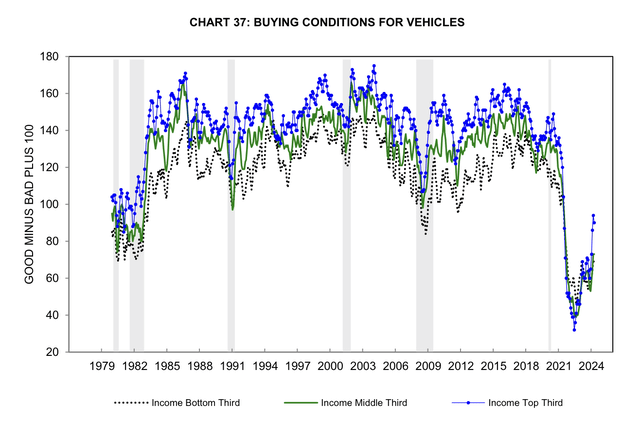

As we see below, consumer sentiment showing vehicle purchasing conditions is very poor for lower and middle class households.

University of Michigan

While this certainly supports demand for used vehicles compared to more expensive new vehicles, I would like to see some weakness in the CPRT share price first before I change my rating to He buys evaluation.

As much as I love this American success story, the price tag is a little too high for my taste.

Away

Copart’s impressive business model, supported by strategic assets and expanding services, continues to thrive in light of favorable industry trends.

Unfortunately, despite the positive growth and strong financial position, the current valuation looks high, with a P/E ratio of 37.5 times.

As much as I admire Copart’s success, I would rather wait for a more attractive entry point before considering it as an entry point He buys.

For now, I’ll keep this standout in my watchlist rather than my portfolio.