joeygil

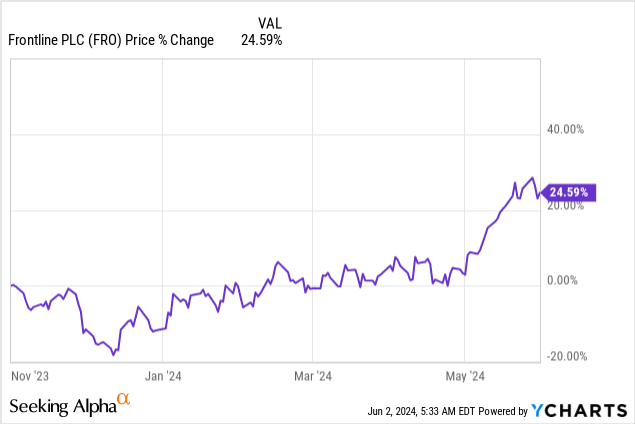

front line (New York Stock Exchange: back and forth) Earnings were reported last week, making it a great time to check how the company is doing. My last article under this name was from November 1, 2023 when she was busy getting Euronav fast. Things couldn’t have gone better for Frontline. After they made a major, strong acquisition, the market remained strong to very strong for a long period of time. In the same month, the Houthis began disrupting trade in the Bab al-Mandab Strait, although it initially appeared that container shipping was mostly affected. This is reflected in the stock price:

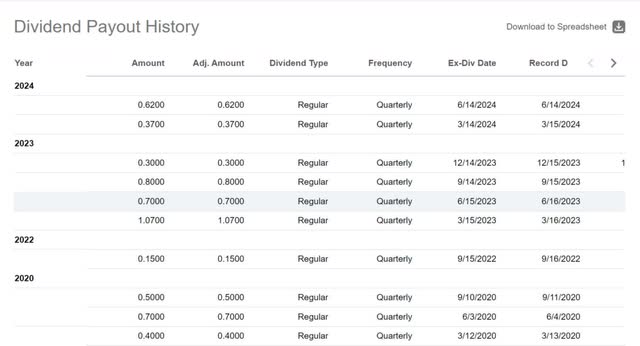

This suggests that the market expects earnings to remain strong for some time, as dividends have also been very good.

Dividend payment date (seekingalpha.com)

So the stock has done well, but the real question is: how likely is this to continue?

The FRO fleet includes 41 VLCCs, 23 Suezmaxes and 18 LR2 tankers. The average age of the fleet is 5.9 years, and almost all ships are environmentally friendly (56% equipped with scrubbers). The ECO classification is important for contracting with major oil companies. Scrubbers increase the flexibility that fuel vessels can use, which can sometimes improve or greatly improve profitability.

The company has just taken delivery of the Euronav fleet, which was delivered from its site in Singapore. This means that the fleet was short on “real” capacity during the quarter. FRO management believes the integrated fleet will be operating at “record” utilization rates by the third quarter of this year.

The most important driver in the short term will likely be the war in Ukraine because of the ton of mileage it adds. The second most important factor is likely the disruption of the Suez Canal caused by Houthi strikes.

I see no signs that the impact of the war in Ukraine will abate in the short term, and it could be viewed as the new reality in shipping. Suez Canal disturbances I’m not sure about. The long-term trend has been to shift capacity increasingly away. Frontline gives the impression that they are not close to getting back there. Prices have been falling recently, although they are clearly volatile, and for longer-term contracts, prices look strong.

The state of the Red Sea (front line)

Other short-term impacts are the Dangote refinery in Lagos, Nigeria. I have just started shipping the product. This adds significant refining capacity to an area that has significant production but does not have much refining capacity. In theory, it could take a few tons of miles off the market. Especially on the product tanker front. According to Frontline, surprisingly, the refinery also imports crude oil from the United States which may mitigate some of this impact.

Then there’s the completion of the TMX Pipeline, which brings Canada’s captive oil production to the seaborne market. This should be a strong positive in terms of ton and mile demand.

In terms of display and charging capacity, things look good too. The VLCC order book shows that large orders for Suezmax and LR2 aircraft have been placed at shipyards. The same does not apply to supertankers. Frontline is primarily a VLCC company.

Giant crude oil tankers (front line)

Orders may change. New orders can be added. Rising rates or significant increases in long-term rates are likely to lead to higher VLCC orders as well. However, building these massive ships takes time and knowledge. There was something very interesting on the earnings call regarding shipyard capacity that I want to highlight (emphasis mine):

And then let’s move on to Slide 11. And I think if there’s one important slide in our quarterly presentation this time, it’s this one. And I looked at the bottom left chart. So, from 2024 onwards, we are actually hitting the substitution barrier. Based on the tonnage that needs to be phased out at 20 or 25 years of age, depending on the asset class, there are a significant number of dwt vessels built between 2004 and 2011 that have essentially reached age. 2011 was the absolute peak year for new builds, and this again includes all asset classes.

At that time, we had 519 shipyards in the world. Now we have 247 shipyards in the world. Therefore, in the number of shipyards globally, the number of yards has been reduced by 52%. (Yardage Capacity) Ton Capacity Since some of these yards are larger, the reduction is somewhat lower at 40%.

Since the market has been strong since its acquisition, Frontline has aggressively returned cash to shareholders. In the most recent quarter, they return 100% of adjusted net income and management is guiding to return between 80% – 100% of adjusted net income depending on market conditions.

Yes. I think you should — kind of a rule of thumb, which is, again, not an 80% of adjusted net income policy. And I think you – that’s what you should have in the back of your head. (Especially) This, this is what happens. But I also think the reason we chose to go to 100% this time is because we have a good vision. We are in a good position in terms of liquidity. Our mission is to give shareholders the money we make. But obviously, depending on how the markets develop going forward, you can speculate whether we want to do 100% again or whether we will reach 80%. But I think it will be related to the overall market temperature.

I really like this policy, which makes it very likely that the investment here will naturally unwind over time because it gets rid of cash and because it seems to me that the odds are that profits could remain relatively good in the near to medium term. Analysts have earnings estimates for this year at $3.35. The lowest estimate is $2.45 while the highest estimate is around $3.85. I would say the range is probably a little narrow. Shipping can be volatile and a lot of things can happen. More importantly, I think estimates will be easily beaten on the upside.

In conclusion, Frontline will likely continue to benefit from strong market conditions thanks to the terrible war in Ukraine and Houthi activity in the Red Sea. The company is still absorbing Euronav’s fleet. This leaves little upside to be taken away from the young, environmentally friendly fleet in the short term. The Dangote refinery or the completion of the TMX pipeline could have a good or bad impact on the market. These are issues to keep tabs on. In the longer term, the shallow order book and limited shipyard capacity suggest that this may be an asymmetric bull/bear situation. No less important is that the company follows a strong policy of returning shareholders through dividends. Although the stock has performed well, I think this is still a hold or even a buy.