ref

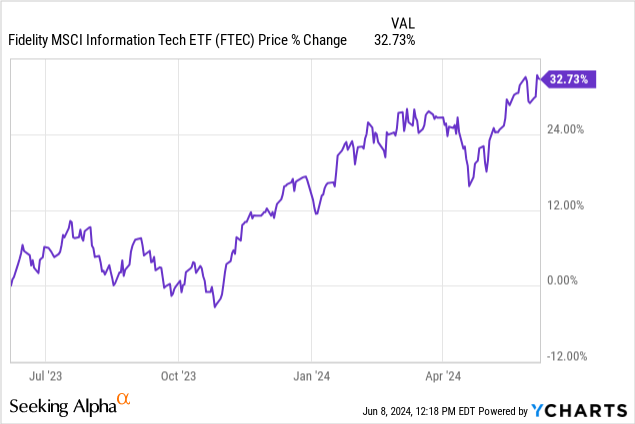

Shares of the Fidelity MSCI Information Technology Index ETF are trading at around $163 at the time of writing (NYSEARCA:FTEC) by 32.73% over the past year, as shown below. This was possible largely because of its summit Collectibles have benefited from AI enthusiasm, but after this performance, it becomes important to evaluate whether the momentum can continue.

Also, things changed recently after AI-invested company Salesforce (CRM) reported poor earnings and was severely punished by the market, with volatility also sweeping other software stocks at the time. As a result, this thesis aims to show that now is the time to be cautious based on emerging risks as AGI begins to disrupt the enterprise software industry with related stocks making up a significant portion of FTEC’s overall weighting.

First, he points out that although valuations have become expensive for AI stocks, there are still opportunities.

AI has become very expensive

Nvidia (NVDA) posted a stunning one-year performance of 222% after emerging as a dominant manufacturer of parallel computing chips for major AI players like OpenAI. In the wake of this, other stocks such as Advanced Micro Devices (AMD) and Broadcom (AVGO) also gained 42% and 77%, respectively. The first has positioned itself as an alternative player in the GPU accelerator space trying to win market share from Nvidia and the second is a dedicated chipset provider to cloud providers, be it for computing or networking.

Institutional.fidelity.com

Now, Broadcom is the cheapest of these three stocks, and comes with a price-to-earnings multiple of more than 50x, which beats the IT sector average by more than 75%. While such a high valuation may seem incomprehensible to the average value investor, it can still be justified by the growth and productivity prospects generated by AI.

There are still opportunities in the field of artificial intelligence

In this regard, according to Bloomberg Intelligence, spending on artificial intelligence is expected to reach $1.3 trillion by 2032, i.e. an average growth rate of 42% over the next ten years. Equally important, research from McKinsey shows that labor productivity could increase by 0.1% to 0.6% annually from 2024 to 2040 depending on the pace of adoption of new generation AI.

Moreover, the companies that are likely to benefit are not just those that provide related technologies like the three chips mentioned above, but others in fields as diverse as robotics, cybersecurity, education, finance, and even health. However, to be realistic, not all companies can afford to invest hundreds of millions of dollars in chips and data center infrastructure. Therefore, to make AI available to these companies without having to invest large amounts of capital and in an as-a-service manner, hyperscalers (giant cloud providers) like Microsoft (MSFT) are key.

If we look further, the market has been optimistic about companies that are likely to integrate AI into their development strategy, and among these companies, we can particularly mention Apple (AAPL) with its high-end devices (iPhone and iMac) and iOS ecosystems. .

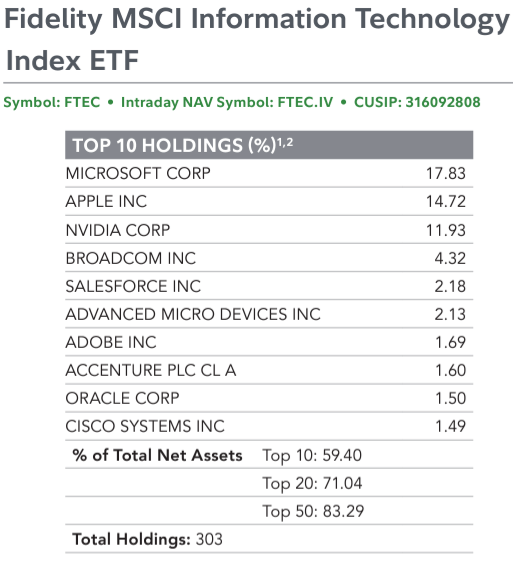

Now, with about 50.93% of its assets allocated to the five stocks I was talking about, FTEC has delivered an upbeat performance.

Looking ahead, the number of times the annual revenue estimates and EPS consensus estimates for these five stocks have been revised upward (“up”) by analysts, often exceeds the number of downgrades (“down”) as shown in the table below.

The table was prepared using data from (seekingalpha.com)

Thus, only AMD saw a decline in its revenue and EPS rankings, but they make up only 2.13% of FTEC’s total weight. Therefore, with more green than red, analysts generally remain optimistic that their financial results will continue to improve, meaning the uptrend may continue.

Risks associated with application software

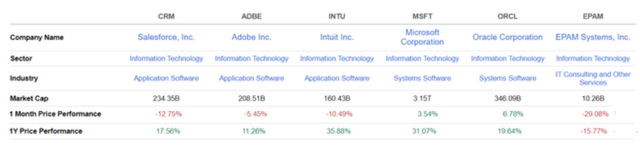

However, back to Salesforce, which makes up 2.18% of FTEC’s weight and is part of the ten largest holdings, it was down more than 19% on May 31 after reporting financial results and guidance that beat estimates. Earlier last month, shares of EPAM Systems (EPAM), one of FTEC’s 305 holdings, fell more or 27% in reaction to earnings with analysts downgrading its revenue forecasts for the second quarter.

Furthermore, according to Seeking Alpha News, other software stocks that fell in the wake of Salesforce’s decline include software giant Microsoft, database giant Oracle (ORCL), Adobe (ADBE), and Intuit (INTU). It’s worth noting that FTEC lost about 4.5% of its value in that time before eventually recovering its losses, showing that the performance of software stocks is indeed affecting its trajectory.

Now, for clarity, it is important to differentiate between the two systems software and application software industries that belong to the IT sector as shown in the comparison table below. When combined, these two groups are referred to as Enterprise. Here, investors will notice that Microsoft and Oracle are classified in the systems software industry because, in addition to software, they are also providers of operating systems and databases respectively. As such, their one-month price performance shows that they have suffered less than application software players like Salesforce and their peers.

seekalpha.com

One reason application software companies are performing poorly (relative to system software) is that they are already facing the disruptive power of the AI generation.

One example is chat-based tools like ChatGPT developed by OpenAI that dramatically improve customer experience through features such as interactivity, personal interactions, and improved response times with improved accuracy. This is causing CEOs to rethink the way they interact with and even purchase software. Another example is Microsoft’s Copilot which is a Gen AI chatbot developed in the wake of ChatGPT that helps software developers write code faster and helps them with many office productivity tasks.

Hence, we are in the era of super-intelligent, AI-powered personal assistants that are reshaping customer engagement models to deliver more productivity, according to IDC. The consequences are changing organizational structures, reorganization of various industries, and other changes. In a similar vein, a new study by McKinsey highlights that while AI generation can accelerate growth in the enterprise software industry, it also presents new challenges that can instill a realignment of product categories and competitive dynamics.

Translating this to FTEC’s holdings, customers may suspend subscription renewals when they get more clarity, which in turn impacts their revenues. In this case, it’s not just about immediately investing in Gen AI-based applications as Salesforce did with Einstein GPT for CRM or EPAM with Vivien’s digital assistant, but also the ability to quickly realign priorities and deliver returns, especially when investor expectations run high. very.

This is not a good time to invest as there are also risks associated with the price

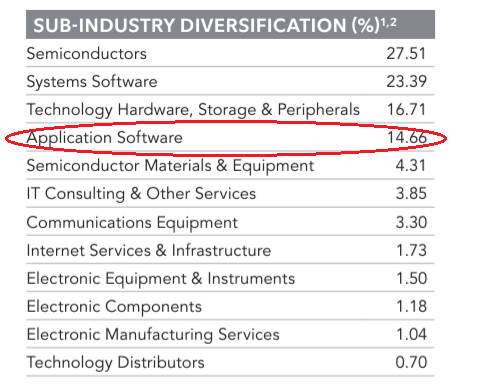

This is why it is not a good time to invest in the ETF right now due to its exposure to Application Software of 14.66% as circled below in red. I think that so far, volatility has been largely limited by the strength of the hype around AI, but things may change during the next wave of financial results reports.

Institutional.fidelity.com

To further justify my cautious stance, the ETF trades at a P/E of 28.61x which beats the category average, and the SPDR S&P 500 ETF Trust (SPY) by 6.7% and 31.5%, respectively.

Now, with their relatively high valuations, technology is particularly sensitive to interest rate risk and can be volatile if there are fewer chances of the US central bank cutting interest rates. This was the case on Friday, June 7 when non-farm payrolls figures showed that the labor market had added more jobs than expected indicating economic resilience, which in turn reduces the need to cut interest rates.

In this case, investors expect the technology to grow faster, requiring relatively more capital and higher borrowing costs with interest rates remaining above 5%. This is especially true for FTEC’s hundreds of small IT companies that may not benefit from the same level of cash flows as big tech like Apple or Microsoft. Meanwhile, inflation remains above 3%, which increases operating expenses because IT experts specializing in AI are not only scarce, but are paid higher wages than the average worker, which in turn puts pressure on profitability.

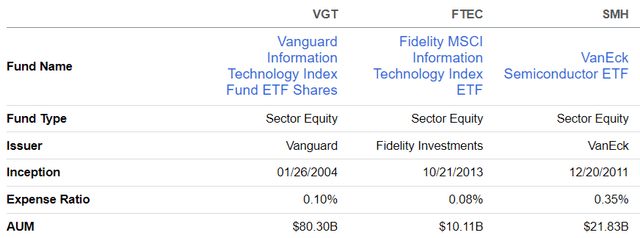

If we look across the ETF space for those looking for an alternative fund, there is the Vanguard IT Index Fund (VGT) which charges only slightly higher fees as shown below. However, the problem is that in the same way as the FTEC, it also negatively tracks the MSCI USA IMI Information Technology 25/50 Index. Thus, for those who want to invest in the AI story without exposure to application software, an alternative is the VanEck Semiconductor ETF dedicated to chip operation. It’s worth noting that it shares some common names operating in the software industry such as Fidelity ETFs such as Synopsys (SNPS) and Cadence Design Systems (CDNS), but specializes in the chip industry.

seekalpha.com

In conclusion, this thesis has shown that while the opportunities for AGI remain intact for some of FTEC’s key holdings, new risks have emerged for those in the application software industry. This is evident in the way its share prices have been affected in the past month, and the pain could continue when next quarter’s results are announced as investors’ patience runs out. In addition to the risks posed by the disruptive nature of innovative technology, the market also has to contend with the possibility that interest rates will remain higher for longer. In these circumstances, I have a holding position.