Available on Stock/iStock Editorial via Getty Images

G-III clothing group (NASDAQ:GIIThe company announced its first-quarter earnings on June 6y From June. Although the stock initially reacted positively in pre-market trading as the company reported strong profitability, during market hours, the stock fell to… Severe fall.

I previously published an article about the stock on the 25thy January titled “G-III Apparel: Searching for Better Cash Flow.” In the article, I noted that G-III Apparel’s long-term growth record appears to be showing signs of slowing down, leading the stock to start at a Hold rating. In the article, I looked for better future cash flows from the company, as slower growth would result in less capital being tied up. Given the negative reaction to the stock’s Q1 results, the stock has now returned -13% following my article compared to the S&P 500’s return of 9%.

Record my review on GIII (Searching for Alpha)

Financial report for the first quarter

G-III Apparel announced the company’s first-quarter earnings on June 6y June before the market opens. Revenue grew 0.5% year-over-year to $609.7 million, $6.7 million below Wall Street analysts’ estimates. Adjusted EPS came in stronger than expected at $0.12, beating estimates by $0.15 even though it missed prior-year Q1 EPS by $0.01. Compared to previously provided forecasts for the quarter, sales were lost by $5.3 million and EPS came in $0.17 above the midpoint of the given forecast range.

The company also slightly changed its fiscal year 2025 outlook and issued a forecast for the fiscal second quarter. G-III Apparel previously expected revenue of about $3.2 billion and adjusted net income of $167 million to $172 million, but has now revised profitability slightly to a range of $170 million to $175 million. For the second quarter, revenues are expected to decline by -1.5% to $650 million and average EPS will decline by $0.12 year-over-year.

I think the results reported have been fairly good, and the stronger than expected profitability for the first quarter and higher profitability outlook for FY2025 is great as profitability was expected to decline significantly with costs related to the launch of the new brand. The weak revenue comes on the heels of already weak FY2024 results that missed estimates by a small amount, and FY2025 forecasts still project an upbeat second half of the year. In my opinion, some caution on revenue guidance is reasonable with Q1 results and Q2 expectations. The success of a new brand launch largely determines a company’s revenue, and according to the first quarter earnings call, significant new releases are coming from G-III Apparel. A continued revenue slope over the long term poses a significant risk to the company, in my opinion, but I don’t see such an event likely currently.

Strategic partnership and stake in AWWG

With the first quarter report, G-III Apparel also announced the beginning of a strategic partnership with All We Wear Group (AWWG), a platform for global apparel brands. AWWG has annual revenue of about $650 million, with G-III Apparel buying a 12% stake in the company, and is looking to increase ownership to 20% in the coming months and possibly acquire the company.

The strategic partnership allows G-III Apparel to expand internationally into Spain, Portugal and India with Madrid-based AWWG. AWWG has managed several prominent brands, including Hackett, Pepe Jeans and PVH Corp’s Iberian business. (PVH), making the company a knowledgeable company to help G-III Apparel better expand into the European market. The company will become the agent for G-III Apparel’s DKNY, Donna Karan and Karl Lagerfeld brands in Spain and Portugal.

The overall impact of the partnership should be very small for G-III Apparel since Spain and Portugal are relatively small markets. Acquiring the remainder of AWWG could be significant, although revenue of $650 could contribute significantly to G-III Apparel’s revenue. At present, speculation on the feasibility of such a move is difficult to estimate, as more in-depth financial data and valuation have not been provided.

Cash flows were healthy in the fourth and first quarters

After my previous writing emphasized the importance of improving cash flows, G-III Apparel’s fourth quarter showed elevated free cash flow of $352.3 million as lower inventories and receivables led to increased cash flow. First quarter working capital dilution of $26.6 million continued as inventories declined further. While two quarters alone are not enough to extrapolate into improved cash flow management over the long term, and the fourth quarter usually has strong cash flows, improvements are a good sign especially if performance can be continued through good working capital management in the coming quarters.

The updated valuation shows a great upside

In light of recent performance, I updated my DCF model. I am now estimating very similar revenues for fiscal year 2025, but have pushed the growth estimates back to earlier years due to the positive growth impact of the AWWG partnership on future years. Growth in subsequent years appears to be lower due to recent poor growth performance, making more conservative estimates justified. Revenues now reach $4,003 million in FY 2034 at a CAGR of 2.6% from FY 2024, compared to implied revenues of $4,000 million for FY 2034 in the previous model.

I also estimate more conservative EBIT margins going forward due to weak FY2025 guidance. Although profitability will temporarily weaken due to brand investments, I estimate margin will continue at a steady level of 7.2% from FY2026 onwards After a 7.3% margin in FY 2025. Due to better working capital management recently, I have now raised my cash flow conversion estimate slightly.

Estimates place G-III Apparel’s fair value estimate at $8.95, 45% above the stock price at the time of writing. The new fair value estimate is up 8% from my previous estimate of $36.05, and combined with the lower share price, the stock now makes an attractive investment with a caveat – future growth should be viewed closely as continued revenue declines could kill margins, cash flows And ultimately the investment case.

Discounted cash flow model (author’s account)

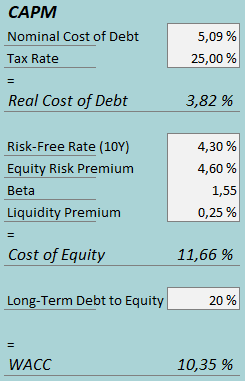

A weighted average cost of capital of 10.35% was used in the DCF model. The weighted average cost of capital (WACC) used is derived from the capital asset pricing model:

CAPM (author’s account)

In the first quarter, G-III Apparel had $5.4 million in interest expense, giving the company an interest rate of 5.09% with the current amount of interest-bearing debt. The company continues to benefit from a significant amount of debt, and I keep my long-term debt-to-equity ratio estimate at 20%.

To estimate the cost of stocks, I use the 10-year US bond yield of 4.30% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the US, updated on 5y January. Seeking Alpha estimates G-III Apparel’s beta to be 1.28, and I’m using the average of the previous estimate of 1.81 and the most recent estimate, which makes a beta of 1.55. Finally, I add a liquidity premium of 0.25%, creating a cost of equity of 11.66% and an average cost of capital of 10.35%. The WACC decreased significantly from 11.76% previously due to lower beta and interest rate estimates.

Away

G-III Apparel reported first-quarter results, showing continued revenue weakness as revenue declined slightly year over year. A gradual improvement is expected in the second half of fiscal 2025 with new launches, however, higher-than-expected first-quarter profitability is a very positive sign. The company also raised its previously provided profitability guidance for fiscal 2025 to a slightly lower level with the report.

In addition to the first quarter financials, the company announced a strategic partnership with AWWG and a 12% stake in the company to drive growth in new markets. The partnership should help growth in the coming years, but only a full takeover of the company will significantly change the overall investment case in my opinion. Since cash flows were healthy with better working capital management and the stock declined from my previous article to an attractive level, I upgraded my rating to buy. However, I suggest being cautious about growth as the recent weak performance is expected to continue through at least the second quarter.