Pollard

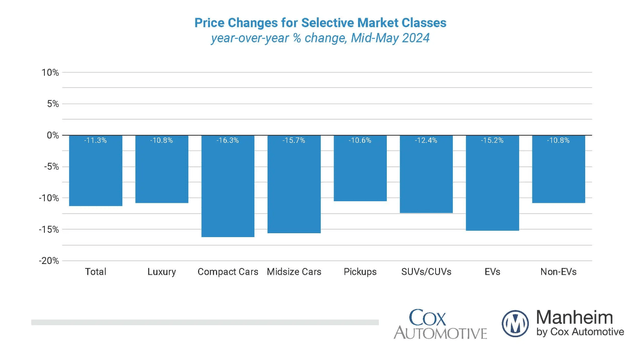

It’s already a A tense electoral atmosphere. Both presidential candidates pledged to pressure China, primarily via… Definitions, which may benefit some local automakers. Moreover, consumers are increasingly Stay away from electric cars. According to the latest Mannheim used Vehicle Value Index, the price of a typical electric vehicle has fallen by more than 15%.

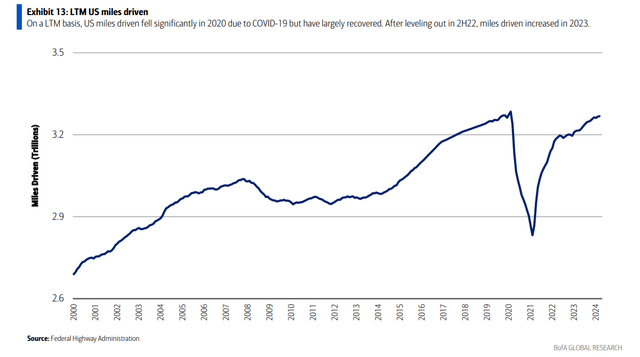

Naturally, most car categories suffered huge losses as the car market returned to normal. However, the mileage numbers are impressive, and a large number of American travelers hit the road for long weekends. So there are some tailwinds for US automakers, but the risks remain clear.

I have a buy rating on General Motors stock (New York Stock Exchange: General Motors). I see the stock as having compelling value while the technical chart is showing signs of life. Furthermore, GM’s management team bought back stock.

Used vehicle values Decreased sharply year on year

Mannheim by Cox Automotive

U.S. mileage numbers over the last 12 months continue to recover

Bank of America Global Research

According to Bank of America Global Research, General Motors is one of the world’s largest automakers, with annual production volume of about 9 million units. The company reports operations in four segments: North America, International, GM Financial, and GM Cruise. It has made significant strides in restructuring its business since the last decline in 2009, leaving it well-positioned to deal with the vicissitudes of the cycle and an evolving industry landscape.

In April, G.M mentioned A strong set of first quarter results. First-quarter non-GAAP EPS of $2.62 It easily beat Wall Street estimates of $2.11, while revenues of $43 billion, up 7.5% from year-ago levels, beat expectations by an impressive $1.22 billion. The big gains were driven by strong operating results and stock buybacks.

Adjusted EBIT increased 2% to $3.9 billion with a healthy EBIT margin of 9%. Its profits from the North American region rose 7% as car sales rose modestly, despite a decline in market share. GM International suffered from lower EBIT, but that was reportedly due to corporate actions.

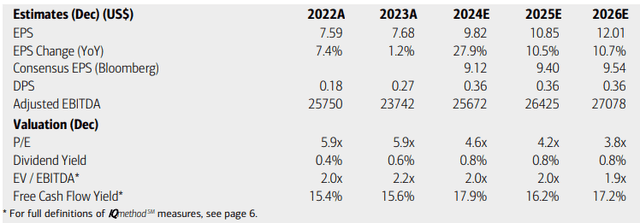

But what was impressive was that GM’s management team increased its full-year 2024 guidance and revised its EBIT range. Adjusted EPS now shows between $9 and $10. Free cash flow forecasts were also raised as the company’s balance sheet remains strong – highly liquid with a slight reduction in debt in the first quarter.

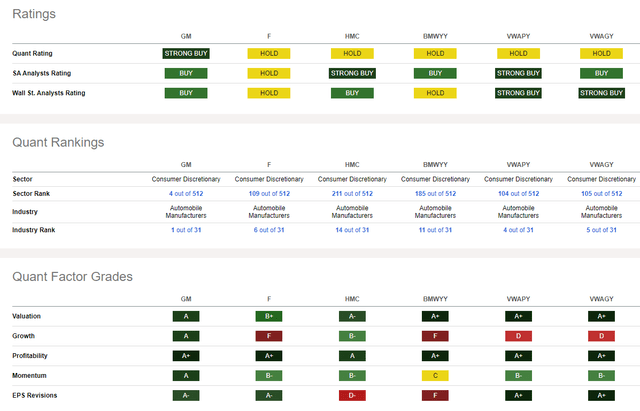

Shares rose more than 4% after the “Show me” quarter proved the bears wrong. Analysts now expect to report $2.63 operating EPS in July, up from just $1.91 from July last year. GM Now pUnkid #1 Out of 31 in the Seeking Alpha industry, according to a quantitative ranking system.

Risks to the investment thesis primarily include a weaker than expected macroeconomy, leading to lower consumer spending and lower auto sales. Moreover, the recent rise in prices of certain commodities could squeeze GM’s margins if not managed well, and while supply chains have loosened, geopolitical factors could lead to problems in sourcing markets. Stressed capital markets could also hurt GM’s debt position.

on evaluationAnalysts at Bank of America see… Jump in profits by more than 25% this year with continued high EPS growth in recent years, likely exceeding $12 by 2026. However, Seeking Alpha’s current consensus earnings numbers are not optimistic, with non-GAAP EPS in the Generally between $9.40 and $9.52.

I expect more earnings upgrades after the impressive first quarter report. There have been 21 upward revisions to EPS in the last 90 days compared to just one downgrade from sell-side analysts.

Meanwhile, the dividend is expected to remain steady at $0.36 per year, so income investors likely won’t be as enamored with GM today, even though the total shareholder return is more impressive given the buybacks. With a single-digit P/E and an EV/EBITDA ratio of just 2.0x, the stock is a compelling value. The free cash flow yield is very high, not far from 20%.

Managing Director: Earnings, valuation, dividend yield, and free cash flow forecasts

Bank of America Global Research

If we assume common EPS of $9.50 and apply a five-year average earnings per share multiple of 7.9x, shares should be trading near $75. GM isn’t cheap on an EV/sales basis, but even that metric confirms that the stock is attractively priced. Advances in electric and autonomous vehicles could boost the P/E ratio in the coming years.

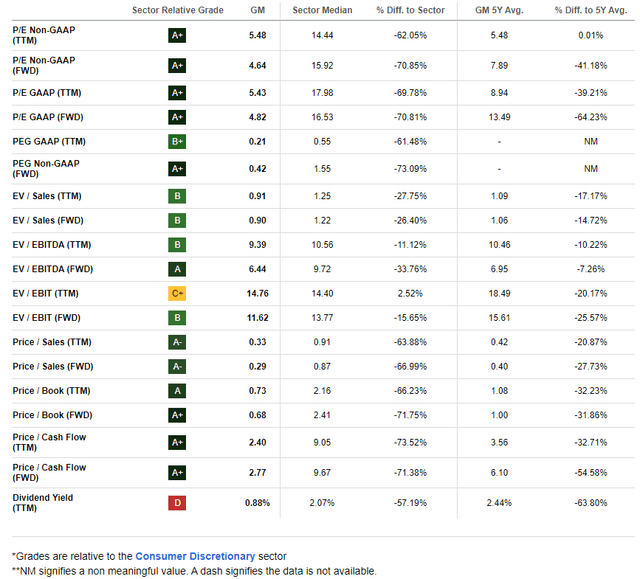

GM: Very low valuation metrics, high free cash flow

Seeking alpha

Compared to its peersGM has a strong valuation rating while its growth trajectory is nearly the best you’ll find in the auto industry. Profitability metrics Great, highlighted by trading stocks with just 6x free cash flow. EPS Reviews Positive, as mentioned earlier, and GM’s Stock price momentum Finally it appends to the upward evaluation hypothesis.

Competitor analysis

Seeking alpha

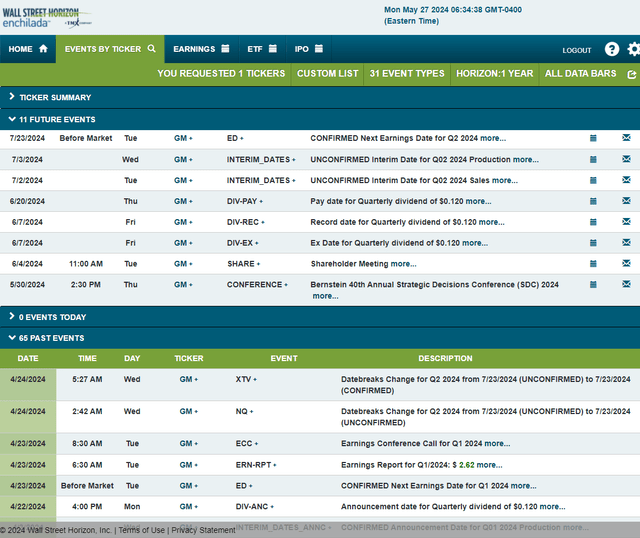

Looking ahead, corporate events data provided by Wall Street Horizon shows a confirmed Q2 2024 earnings date of Tuesday, July 23 for BMO. Before that, the company’s management team is expected to participate in Bernstein’s 40th Annual Strategic Decisions Conference (SDC) 2024 in New York from May 29-31. GM also holds its annual shareholders meeting on June 4, before the dividend date. From June 7.

Assessing the risks of corporate events

Wall Street Horizon

Technical take

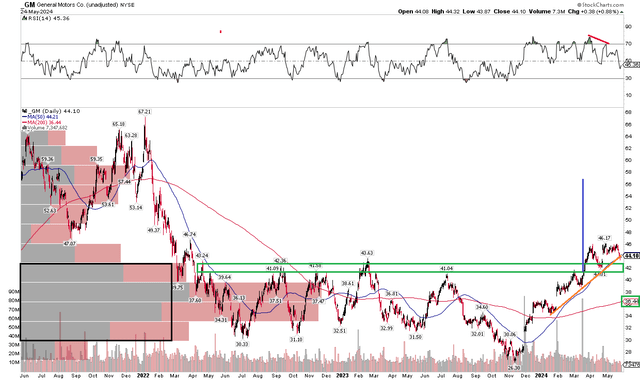

After a string of high earnings, continued shareholder-friendly activities, and an inexpensive valuation, GM’s technical outlook looks good. Notice in the chart below that after ranging sideways for the better part of two years, between $30 and $44 (with a false low of $26 last November), GM is now near two-year highs. The stock’s long-term 200-day moving average is positively sloping, indicating that the bulls are in control of the underlying trend. Stocks are now testing the bullish 50DMA and an uptrend support line from months ago.

Also take a look at the Relative Strength Index (RSI) momentum indicator at the top of the chart – there is some bearish divergence, so we could see further weakness in the near term. I’m also concerned about the earnings-related price gap at the $36 level. But after the bullish breakout in Q1, a measured upside price target to near $58 is in play based on the previous pattern high and breakout.

Overall, I see support at $42 and $36, while $53 represents near-term resistance while the technical pattern price target sits at the top of $50.

GM: Stocks are trending higher, but the RSI is weaker, rising by 200 days

Stockcharts.com

Bottom line

I have a Buy rating on GM. I see the stock as a strong value given where earnings could be headed and with the management team buying back shares. Free cash flow is strong while the technical picture is generally favourable.