More ISO

Investment thesis

The company operates within a duopoly in the real-time sports data and technology market. It continues to benefit from secular growth in online sports betting in the United States, as well as globally. The business has shown strong revenues Growth, with EBITDA growing faster due to the fixed cost nature of its business model. The company is expected to be free cash flow positive this year and is trading at an attractive valuation given its promising growth prospects. Furthermore, I have identified several catalysts that could ultimately lead to further upside.

Company overview

mathematical genius (New York Stock Exchange: GENIE) is a B2B sports data aggregator that provides live sports data to sports betting and media companies. The company has exclusive rights to sports data through exclusive partnerships with major leagues such as the NFL, NCAA, WNBA and the English Premier League. the The company operates in a duopoly with Sportradar (SRAD) for global sports data. While Genius has a stronger presence in Europe and Asia, Sportradar Much stronger in the US due to its partnerships with the NBA and MLB.

Along with its main focus on collecting, managing and distributing real-time sports data, the company has recently introduced offerings such as BetVision, which provides an interactive and immersive live streaming experience alongside in-game betting in the NFL. Likewise, the company’s Dragon technology has been deployed to enable enhanced features for fans watching live or post-match videos on social media. Mark Locke, CEO of Genius, described this during their Q1 2024 earnings call when he said:

One really exciting example of how we’re taking this a step further is our new partnership with Premier League team Brentford Football Club and one of their sponsors, Gtech, to provide more highlights for fans in stadiums and on social media. We have now combined our player tracking and broadcast augmentation tools with our advertising technology to create a brand new sponsorship inventory for Brentford Stadium’s naming partner.

Performing recent work

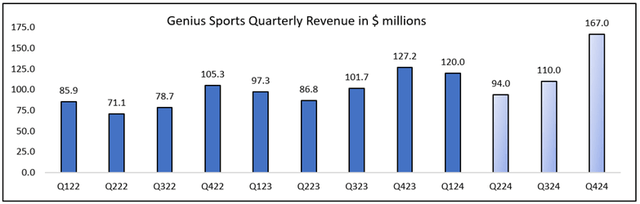

Strong revenue growth is set to continue

Created using company data

The company has shown significant growth since its IPO via SPAC in April 2021, with revenue levels doubling in the past three years. The US sports betting market continues to grow at over 12% and has been a consistent catalyst for business. Last quarter, Genius’ revenues grew 23% year-over-year, driven by a 14% increase in betting-related revenues and a 63% increase in media-related revenues. Management’s guidance calls for FY24 revenue of $500 million, an increase from previous guidance of $480 million. This means annual revenue growth of 21% in 2024.

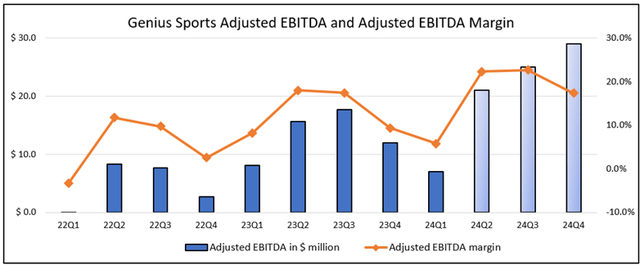

Additional revenue streams lead to improved profitability

Created using company data

In general, Genius Sports operates on a fixed cost model, where most of the fixed costs are related to payments made to sports leagues for the rights to their data. The company was able to leverage its business model by fueling its growth through additional revenue streams, resulting in rapid growth in EBITDA margins. The company’s fiscal 2024 adjusted EBITDA guidance is $82 million, 53% higher than the prior year.

The company’s margins today are in the low 20s, while management’s long-term target is 30%. Key to the company’s ability to lift adjusted EBITDA margins is increasing the share of in-game bets through offerings like BetVision. This tends to have a higher take rate (5%), which is three times higher than the take rate on pre-match bets (1.5%), as shown on Slide 30 of our 2022 Investor Day presentation. Most importantly, This additional revenue comes at no additional cost. So, this is a significant accretive margin for the company and this was made clear by the company’s CEO during the Q1 2024 earnings call when he said:

The headlines are that for every extra dollar we earn betting, whether it’s due to a higher operating margin, increased TAM, or sports betting mix, the extra dollar, most of it goes down, which is nearly 100%. Now obviously individual betting products will vary on this basis, but this is the general rubric.

Net cash position

The company has a healthy balance sheet with $73 million in cash and no debt. It also recently entered into a $90 million revolving credit agreement, giving it additional financial flexibility.

Catalysts

Higher margins than in-game betting

As described above, increasing revenue through additional features and services such as in-game betting will significantly increase the company’s profits. In-game betting in particular has a long run in the US for Genius, compared to levels reached in mature markets such as the UK.

Florida

The state of Florida granted an exclusive license to the Seminole Tribe, which resumed operations in December of last year through its Hard Rock brand. Genius benefits from the dominant position of its Hard Rock customers in the state, where competing sports betting companies are unable to enter the market. There are a lot of professional teams based in Florida, where sports betting is estimated at around $10 billion annually.

Newly regulated markets

The sports betting market continues to show strong growth with the addition of newly regulated markets like North Carolina. States like Missouri and Oklahoma will likely introduce regulations later this year. Outside of the US, Brazil represents a huge opportunity where regulations were introduced last year, with Genius anticipating revenue contributions from the region in the second half of this year.

evaluation

As discussed above, the company is expected to generate $500 million and $82 million in revenue and adjusted EBITDA this year. Given the company’s history of consistently exceeding its guidance, it is very likely that it will exceed the guidance provided. Factoring in net cash of $73 million and assuming 230 million shares outstanding, the company trades at an EV to sales and EV to adjusted EBITDA ratio of 2.2 and 13.7, respectively, as shown below.

Created using data from the company and Seeking Alpha

The current valuation is very attractive given analysts expect the company to enjoy high-teen growth rates over the next three years. Rival Sportradar is more than twice its size and trades at similar valuation multiples, despite expectations of slowing growth.

Given the operating leverage in Genius’ business model, EBITDA should grow at much faster rates, likely approaching 40% over the next three years. I estimate that 2026 adjusted EBITDA will reach approximately $200 million with the company reaching its target margins of 30%. Applying a conservative multiple of 12, which is slightly lower than today’s multiple, would result in a stock price above $10, implying an upside of more than 100% in 2026.

Risks

Overpaying for data rights

The company may overpay for data rights, as it has done in the past for its deal with the NFL. In the case of the NFL deal, even though the company overpaid, it issued stock that was significantly valued in April 2021 (five times higher than today’s stock price) and also brought the NFL’s interest more aligned with the company as it became Genius’ largest shareholder.

a race

The company faces competition for sports rights from Sportradar, which is twice its size. However, Genius has so far managed to maintain its position in terms of securing deals, and even succeeded in extending its most important deals until 2029.

Regulatory changes

The betting industry remains vulnerable to regulatory changes in the United States as well as globally. One such potential headwind could be a ban on betting on college sports.

Genius Sports stock is a buy

The business is trading at an attractive valuation suggesting investors can expect upside of up to 100% by 2026 if management continues to execute on its growth strategy. Although there are some risks associated with it, there are multiple levers that can push a company’s growth and margins to a much higher level, thus rewarding its shareholders handsomely. So I think Genius Sports offers a good risk reward for starting a long position.