Dragon claws

In the past year, real estate investment trusts and office investments have dealt with growing investor concerns about loan performance. High interest rates and poor occupancy performance due to hybrid working arrangements have put pressure on those companies that trust this Characteristics of private offices.

Gladstone Trading Company (Nasdaq: Good) It also owns office properties, but the fund collected 100% of its cash rent in the first quarter of 2024 and its payout metrics still look fairly compelling from a passive income investor’s perspective.

Furthermore, Gladstone Commercial is also more concentrated in industrial properties, so performance issues are less of an issue for investors than with focused office funds.

With the stock also being cheap based on FFO, I think passive income investors are dealing with a solid, long-term investment proposition.

My evaluation history

My last stock rating (March 2024) for Gladstone Commercial was Buy Because the fund had good rent collection and investors were very much inclined to the downside.

Gladstone Commercial adds credibility to my buy case The mortgage REIT has released good results for the first quarter of 2024 which, as some investors expected, did not show a dramatic change in credit performance and in its dividend payout ratio.

An industry focused trust with the highest levels of rent collection and healthy payment metrics

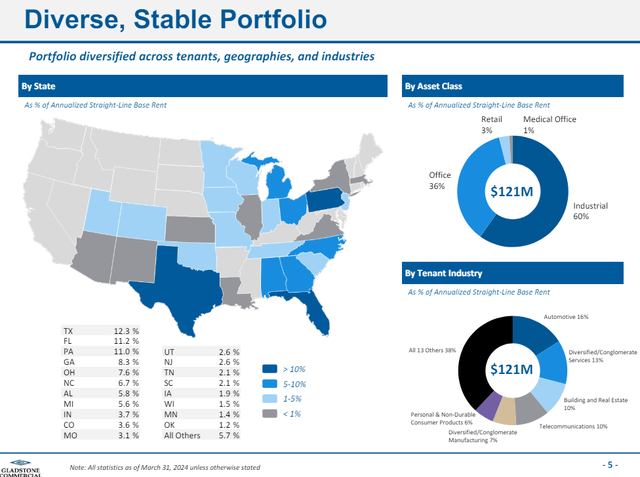

Gladstone Commercial is a hybrid REIT that invests in single-tenant and multi-tenant properties, with a primary focus on industrial properties, which represented 60% of rentals as of March 31, 2024.

Office properties are Gladstone Commercial’s second largest investment portfolio and represent 36% of annual rents. Smaller proportions of real estate investments can be found in unrelated sectors, such as retail and medical offices (reflecting a cumulative total of 4% of rents in Q1 2024).

Gladstone Commercial’s main competitor is STAG Industrial Company (STAG) Which invests entirely in industrial real estate and which I recommend to passive income investors primarily for its exposure to e-commerce growth trends. These same drivers of demand for industrial real estate space work to Gladstone Commercial’s advantage, which can focus on more aggressive acquisitions in the industrial market to offset weakness in the office market.

Gladstone Commercial’s portfolio includes 132 properties across the investment spectrum, reflecting a total investment value of $1.11 billion. The weighted average lease term for Gladstone’s commercial properties as of March 31, 2024 was 6.7 years, compared to 4.4 years for STAG Industrial. I consider the longer lease term to be a competitive advantage for Gladstone Commercial, as the company has a higher degree of cash flow visibility.

Portfolio overview (Gladstone Commercial)

Gladstone Commercial generated $13.9 million in core funds from operations in the first quarter of 2024, reflecting a 4.5% year-over-year decline, primarily due to asset sales. However, the portfolio itself remained a good performer with Gladstone Commercial collecting 100% of its scheduled cash rent during the first quarter (as well as throughout April).

The high degree of cash generation and low FFO-based dividend payout ratio are two considerations that make me believe trust stocks have a place in a passive income investor’s portfolio.

Funds from operations (Gladstone Commercial)

Gladstone Commercial saw its dividend payout ratio rise slightly in the first quarter, rising from 83% to 88%, but earnings as such were well covered by funds from operations, a key metric for determining payouts. Stability for REITs. Currently, Gladstone Commercial pays shareholders $0.30 per share each quarter, which, at the current share price of $14.45, equates to a stock dividend of 8.3%. I don’t expect the REIT to raise its dividend in the future.

However, Gladstone Commercial may see an increase in acquisitions in the future, which could add to funds from operations and improve the Trust’s payout metrics.

Dividend (The author created a table using company supplements)

FFO is a multiple and intrinsic value

Gladstone Commercial had $1.44 EPS FFO in the last four quarters. Based on Q1 2024 FFO run rate, the trust could have $1.36 per share in funds from operations next year.

Based on a share price of $14.45, the fund’s stock is worth just 10.6x FFO. STAG Industrial, which has a better risk-reward relationship given its sole focus on industrial properties, is selling for 14.8x Q1 2024 run rate FFO.

Market-leading industrial REITs, Prologis Corporation (PLD), is selling for 21.2x 1Q24 base FFO at run rate. I think Gladstone Commercial, especially on the back of full rent collection, deserves a higher FFO multiple.

I think 12x FFO is reasonable money from multiple operations for Gladstone Commercial considering its portfolio is doing well. This multiple would take us to an intrinsic value of $16.30.

Why an investment thesis can deteriorate and the downside risks

Gladstone Commercial offers a well-covered dividend, but earnings aren’t growing and you shouldn’t expect them to. Other REITs, such as STAG Industrial, have been growing their dividends, so Gladstone Commercial may continue to sell at a discount to this peer due to a lack of earnings growth.

So far, Gladstone Commercial is also not suffering from the office market. If this changes in the future, the payment trend may deteriorate.

deductive

Gladstone Trading Company looks quite credible as a passive income investment here and the thesis looks compelling in my view.

The REIT collects 100% of its rent and is still able to comfortably cover its profits with funds from operations.

The payout ratio may have risen slightly in Q1 2024, but not to the point where I would fundamentally question the sustainability of Gladstone Commercial’s dividend. I also think Gladstone Commercial’s industrial exposure is a very strong offset to any potential office weakness.

With the stock being as cheap as it is, I think the risk/reward relationship and 8% capped dividend yield equates to a strong value proposition for passive income investors.