Images by Tang Ming Tung/DigitalVision via Getty Images

Investment overview

I wrote about Al Baqala Holding Company (Nasdaq: Go) Previously (March 14, 2024) with a Sell rating as I was very negative on the potential operational impact from the UGO acquisitionwhich could cause GO to miss its FY24 guidance. While the main reason for the stock price decline was not the acquisition (which was completed on April 1st), the 1Q24 performance highlighted gaps in management execution capabilities, I think that affected the stock price.

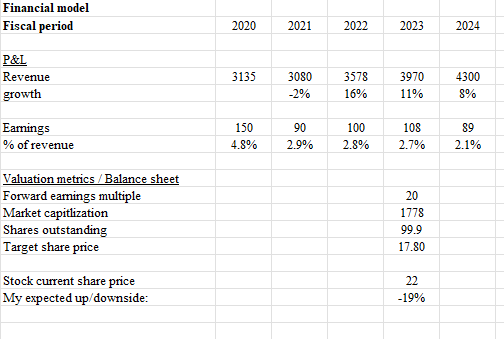

The key takeaway from the latest earnings was that GO reported a disappointing quarter, with earnings per share coming in at $0.09, well below the consensus estimate of $0.18. The reason behind this failure was the weak performance of the EBIT margin, which fell by 330 basis points from 4.6% last year to 1.5% in the first quarter of 2024. It is worth noting that GO reduced its FY2024 EPS guidance by 21%. % at the midpoint, from $1.14 to $1.20 to $0.89 to $0.95 due to maturity. For poor implementation in implementing the technological system.

At the current share price of $22, I still believe GO deserves a sell rating, as I remain uncertain about the impact of the acquisition on same-store sales (SSS) and the potential miss of FY24 guidance.

The performance of SSS will be tested

SSS performance for Q1 2024 was really strong, coming in at 3.9%, at the high end of the guided range. The notable aspect of this performance that was very bullish is that it was driven by a 7% traffic contribution, and average weekly sales improved modestly throughout the quarter. This strength was supported by notable growth across all customer types, with particular strength from middle and upper income groups. Another positive is that the normalization effect from SNAP clients has returned to pre-coronavirus levels.

However, the real test for SSS only begins in the second quarter of 2024, as GO only completed the acquisition of UGO on April 1. Which means healthy SSS performance for 1Q24 not A good baseline for thinking about GO’s SSS performance for next quarter, and remember that the transition time for GO to implement its IO model into UGO will take two years.

The basic argument I made earlier is that GO will face a lot of operational pressure as it acquires 60 new stores at once. In other words, the execution has to be very precise for them to do this successfully, but 1Q24 showed us that management able to Making execution errors (system integration issues and failure to notice a 110 basis point margin impact). Hence, I believe this will continue to impact GO’s valuation and stock sentiment until the market shows consecutive quarters of successful integration with SSS’s growth shows no signs of weakening.

FY24 guidance remains at risk

To give more detail to the guide, management lowered FY24 adjusted EPS guidance by -21% at the midpoint to $0.89-0.95 due to the Q1 failure and also lowered its gross margin forecast to 30.5% versus previous guidance of 31.3%. Additionally, management also guided for Q2 2024 SSS growth of 3.2% and a gross margin of 30%. This updated forecast includes a 2H turn with an implied SSS range of 3.5-5.5% and gross margin drainage. Management’s rationale is that they are seeing strong traffic trends and a healthy lockdown environment; Hence, it is possible that 2H24 will perform much better. In my opinion, there is still a risk that GO will miss its FY24 guidance.

First, potential operational headwinds from the consolidation of all UGO stores remain uncertain at this moment. Repeated execution errors will almost certainly lead to lower key performance and profit performance.

Second, I believe GO will see macro headwinds in the second half of 2024 as inflation continues to move lower. This would turn the previously enjoyed trade tailwinds into headwinds. A study by PYMNTS Intelligence indicated that about half of consumers consider pricing when making a purchasing decision, and 25% of consumers said price is the most important consideration. As prices fall, which new inflation data indicates as cheaper grocery prices, consumers who previously cut their prices must return to their usual purchasing habits.

Third, the competitive environment will worsen for GO as other discount retailers increase their investments. A hint of this competitive pressure can also be seen by management commenting that they are seeing an increase in promotions.

Finally, major grocery chains are also facing pressure from US regulators, which I expect will result in prices being lowered to satisfy regulators, and I believe this will lead to a rebound in customers who left these chains open (because prices are falling again) and then).

evaluation

May investment ideas

Based on my research and analysis, the expected price target for GO is $17.80.

- My model focuses on FY24 earnings due to uncertainty in GO’s earnings outlook (given the reasons mentioned above) and also because FY24 performance appears to be the focus of the market given the strong reaction to FY24 guidance revisions.

- Despite the positive performance of SSS in Q1 2024, I don’t think this represents a good baseline to extrapolate to the rest of FY24, as there are clear headwinds that could negatively impact growth. As such, I continue with the GO model of reporting the minimum growth guide for FY24 ($4.3 billion).

- Given the weak execution we’ve seen to date, potential headwinds on the top line, and the weak margin performance we’ve seen in 1Q24, I’m also not positive on GO’s ability to meet the midpoint of EPS guidance either. I expect GO to provide a minimum guide to its EPS.

- If my predictions come true, I see little reason for GO to continue trading at this multiple. I expect the market to price multiple GOs lower due to weak growth and margin performance. Using the same logic I used previously, I believe GO should trade at a discount to the current level, at approximately ~20x forward P/E.

risk

GO could see a near-term increase in SSS from the impending bankruptcy of 99 Cent Only Stores. This could convince the market that GO is not facing any headwinds for the reasons I mentioned above, and at the current valuation (almost all-time low), could spark a strong rally on improving sentiment. In addition, further contraction in the economic situation is positive for GO as well, especially if inflation picks up again.

Conclusion

I give GO a Sell rating due to uncertainties surrounding its near-term outlook. Specifically, the impact of the UGO acquisition on SSS remains uncertain, and while SSS’s recent performance has been strong, potential macro headwinds such as lower inflation and increased competition could weaken SSS’s strength in the near term. Given these risks and the weak execution we saw in Q1, I remain rated Sell.