bjayam/iStock via Getty Images

Investment summary

the next My last post On Guardant Health, Inc. (Nasdaq: GH) The stock has drifted sideways and it appears that the ‘hold’ option was the right decision.

In this report, I note several factors that I believe will keep GH stock compressed. In particular, the implied price Expectations are that the market has a high required rate of return built into the GH stock price. This means that the company had to achieve excellent results to surprise investors. Sales growth was noted to be very strong, and the revenue curve has been linear since 2021. This was a positive thing.

Since then, there have been multiple updates to the investment debate, which I will address here today. I will also share the revisions I made to my model of the company incorporating these new developments.

Investors have clearly recognized and priced in GH’s sales growth potential The company is more than 5x in sales as I write. This assessment reflects exceptional growth expectations ranging between 22 and 24% over the coming years.

Net-net, I continue to view GH favorably as a company and am inspired by its recent successes in colorectal cancer testing. Unfortunately, this does not mean it is a successful investment at this time in my view, based on the basic investment principles I use. With this in mind, I evaluate the GH contract based on fundamentals and valuation.

Recent developments

1. Blood test shield by vote of approval

In late May, an FDA majority-assembled panel voted that GH’s sideline cancer screening test, the Shield blood test, is safe and effective for patients. According to the World Health Organization (“WHO”), CC is “the third most common cancer worldwide accounting for approximately 10% of all (cases).” It is also the second leading cause of tumor-related deaths in the world.

The World Health Organization also states that CC is often diagnosed at an advanced stage, making treatment options available to only a few people. Therefore, there is a great need to achieve a therapeutic and medical breakthrough in this field, and this can be achieved through diagnosis, in my opinion. It is crucial to have an early diagnosis, therefore, screening tests targeting this “upstream” point of CC diagnosis is a no-brainer in my view.

In this context, this may increase sentiment in the short term to raise the company’s stock price. This is evident in the drift that followed the announcement, which actually saw investors add another $2 to $3 per share in market value after the vote.

However, demand for the stock arrived long before the announcement when it began to rise from lows of $15 to $16 per share. The company’s first-quarter numbers (discussed in more detail below) were the main catalyst leading up to the Shield announcement. In the call, the word “Shield” was mentioned 29 times. More importantly, in my view, are the updated management guidelines for 2024 (which I summarize below).”It does not include any revenue contributions from screening, which depend on the timing of Shield FDA approval and medical reimbursement coverage.“

The move was interesting after FDA staff commented earlier in the month on the potential risk of the Schild test of not detecting advanced adenoma (“AA”) in patients. For reference, AA is the primary precursor of CC.

However, the FDA has supported the idea that the Shield test could improve screening rates and thus early detection of CC in adults over 45 years of age.

Therefore, the shield approval is a short-term incentive that keeps me interested in this company and its stock. And with shares rising from $16 to $31, as I write, it would be unwise to remain ready to launch from the sidelines, in order to 1) improve fundamentals (i.e. operating profits), and 2) cool valuations.

Figure 1.

TradingView, via Seeking Alpha

Q1 2024 Earnings Insights

In terms of growth, the first quarter of 2024 was a good period for the company. GH did $168 million in business, up 31% from last year’s first-quarter sales. The growth was underscored by a 20% increase in clinical tests reported to about 47,000 and a 37% rise in biopharmaceutical tests sold to about 8,500. This generated a gross profit of $103 million, a 61% margin that eased the pressure of 300 basis points on an annual basis. This was driven by better price mix in both operating segments.

Management revised its guidance for fiscal 2024 after the quarter. It now expects 20%-21% growth on the top line, calling for revenue of $685 million at the top end of the range, versus $670 million previously. It is looking to achieve gross margins of between 61% and 63% on this, an increase of 100 basis points from the previous range. It expects to generate free cash flow of about $285 million, an improvement from the previous forecast of $330 million.

As I mentioned earlier, these projections do not include any screening revenue, which has yet to be achieved following the vote to approve the Shield test in May. Without clarity on this matter, I do not want to speculate on this matter yet, and I prefer to wait until the second quarter earnings announcement for more insight.

Regarding divisional division of the top line for the first quarter-

-

Precision oncology Sales rose to $156 million for the quarter, up from $113 million last year. This was confirmed by the 40% growth in the volume of biopharmaceutical tests. Management said this was due to the strong pipeline with which it entered the year and continues to expect additional volume growth in biopharma testing for the remainder of this year.

-

Development services About $12.2 million of business was released, in line with management expectations. There were no visible exits from this division during the quarter.

Management also noted that it has continued to increase the average selling price (“ASP”) for the Guardant360 liquid biopsy test for approximately 12 months. It is now in the range of $2,900-$2,950 – above the expected range of $2,050-$2,900 shown in previous calls. This is a potential catalyst for revenue going forward, and the fact that it is meeting demand at these prices is good evidence of the market’s uptake of the product, in my view.

Despite the excitement following 1) the company’s approval of the Shield trial with the FDA, 2) continued sales growth, and 3) revised fiscal year 2024 guidance, in my view, it’s not enough to change the company’s fundamental economics yet. Not for my basic investing principles – we need more flesh to put on the skeleton.

Fundamental economics support a hold rating

In a recent GH post, I explained the contrast between top-line growth and top-line growth over the past two years. For the company, this is not necessarily a negative thing. Sales growth is clearly the goal of the game with this name, given its efforts to establish its footprint in the market and introduce CC and liquid biopsy tests to the market. Higher revenue indicates more tests/screens shipped out the door.

The actual pattern of how the administration embarked on this path is very interesting. What I want to see in a company focused on fast-growing sales is the total asset value that is kept in check. In other words, assets should not grow faster than revenues.

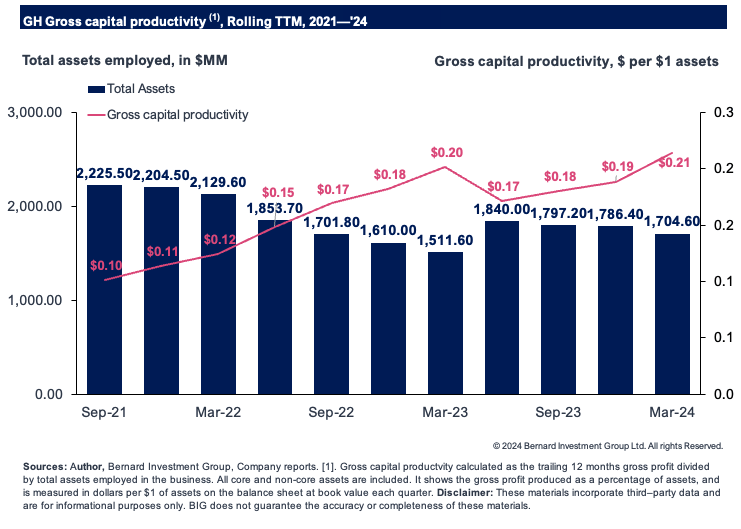

Second, I look for how much gross profit has been rolled over from the assets used on the balance sheet. I did this for GH in Figure 2. As can be seen, the company generates about $0.21 in total profitability for every $1 of assets used in the company. All operating and non-operating assets are included here. As a positive, the company is operating on lower total assets today than it did in 2021.

Figure 2.

Company Files, Author

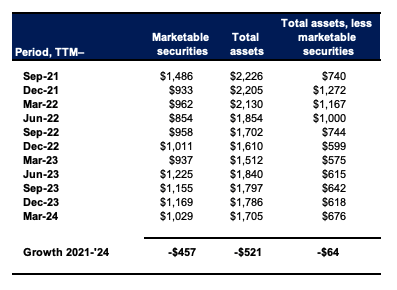

This is important because the company has fantastically high cash and marketable securities as a function of the total value of its assets. When you strip away capital tied up in marketable securities, the company becomes much “leaner” from an asset intensity perspective.

For example, in the March 2024 quarter, it reported total assets of $1.7 billion on the balance sheet versus marketable securities of about $1 billion. Excluding the former from the equation, this comes to $676 million in assets over total liabilities of $1.6 billion (Figure 3). Given that the company’s cash flow is negative, it is quite reasonable to suspect that it is keeping this cash ratio too high as its liquidity buffer.

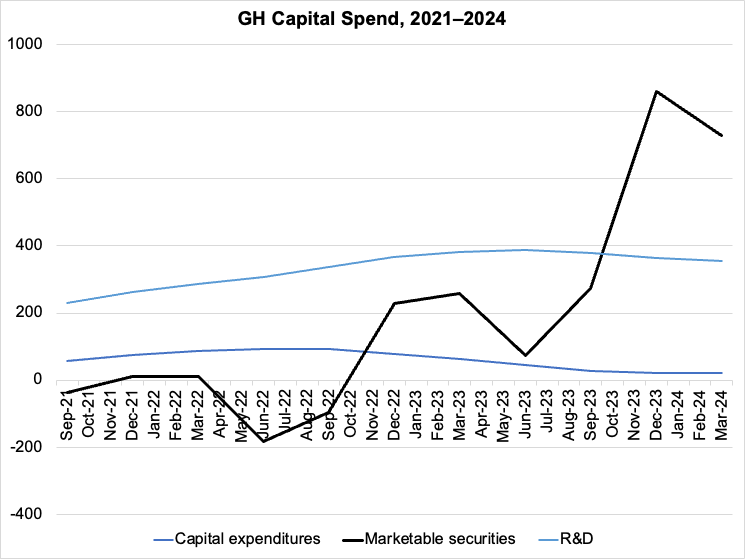

However, I don’t see management deploying the advantage, or really deploying it at all in areas outside of 1) R&D and 2) marketable securities. Figure 4 shows. You can see from 2022 that as we entered the new interest rate cycle, management began shifting cash significantly into marketable securities on a gradual basis. At the same time, investment in research and development and capital expenditures declined.

Figure 3. Most of the asset value is tied up in cash and marketable securities

Company files

Figure 4. Note the difference in cash etc. between R&D and capital expenditures

Company files

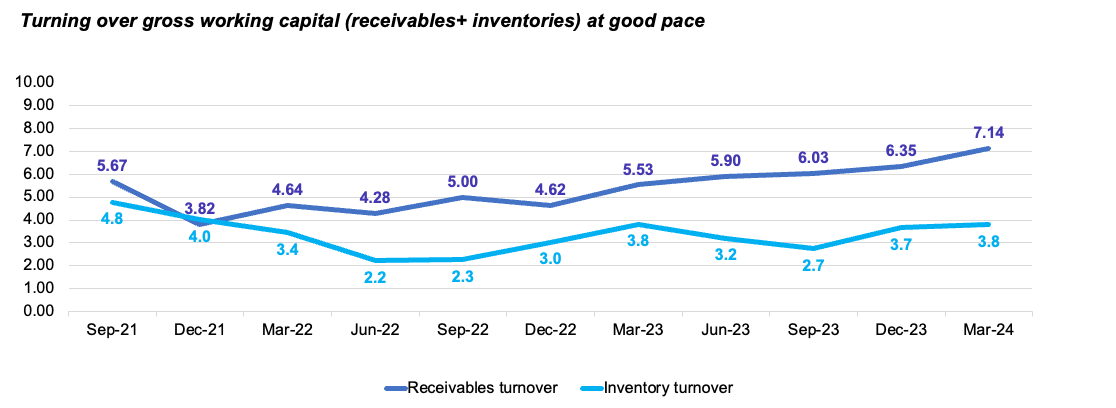

For inventory and receivables for which a company has earned cash, it delivers those values relatively quickly. Figure 5 shows the inventory and receivables turnover rate on a 12-month basis since 2021. As we have seen, the company rotates its inventory about 3-4 times every 12 months. It has delivered receivables faster, from about 4x in 2022 to more than 7x in the past 12 months.

Figure 5.

Company Files, Author

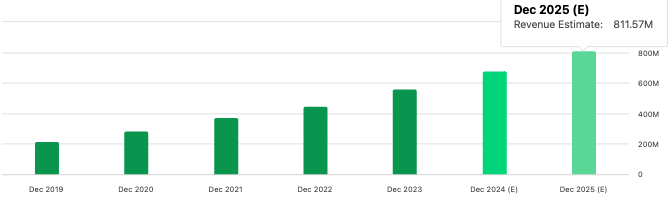

Updates to future estimates

Consensus expects strong growth in the company’s revenues over the next three years, averaging about 20% annually, versus growth in profits of a similar amount. This would push the company’s sales to $680 million this year and $811 million in 2025. If the consensus turns out to be correct, this would represent a sharp increase in revenue, as shown below.

Figure 6.

Seeking alpha

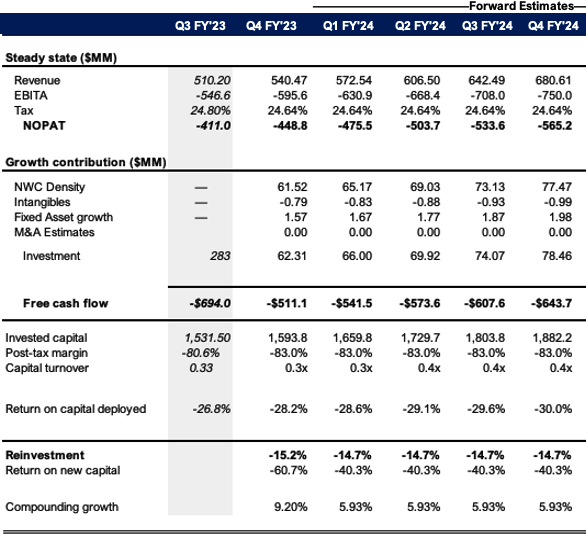

I made the following revisions to my model after the company’s Q1 numbers (Figure 7). I’m in line with the consensus estimate for sales of $680 million by the end of this year. In my view, this would require an investment of $80M-$160M on a capital turnover of 0.4x.

The problem is that if the consensus numbers (and my numbers) are what GH’s current market capitalization is priced in, that doesn’t leave me much room to expect investors to price the company incorrectly. In other words, my numbers do not deviate from Wall Street, and therefore, I cannot say that I hold a different position than what is actually priced in. I hold a neutral point of view.

Figure 7.

Author’s estimates

evaluation

The stock price continues to deliver exceptional growth and has high expectations built into it with the current 5x trailing sales multiple of $564 million. If the company achieves the projected revenue growth rates shown in this report (~21%), at the same 5 times multiple – which is high in my opinion – the company would be worth about $3.4 billion today, which is marginally higher than where it currently stands (5×680 = 3400 dollar).

Furthermore, if the multiple contracts were 3.7 times the industry average, even if the company achieved the expected strong growth numbers, it would only be worth $2.5 billion to us under these assumptions. (3.7 x 680 = $2,516).

This indicates that the valuation is skewed towards the negative side. Even with massive growth rates, a contraction in the multiple would wipe out market valuation by about 25% from a 26% decline in the multiple. Both of these factors support a Neutral rating in my opinion.

Conclusion

After examining the company’s recent developments and updated financials, my rating for GH remains outstanding, and is neutralized by the high valuations it currently sells for. At 5x sales, this is highly vulnerable to multiple contraction, which could compress the company’s market capitalization by a potential 25% if it falls to a sector multiple of 3.7x.

As such, despite the impressive growth in unit sizes and dollar volumes, along with the high growth rate expected going forward, my view is that this is well captured at the current market value, leaving little room for additional upside to the implied price expectations. Repeat waiting.