Anthony Rosenberg

I have renewedHe recently wrote about weakness in the consumer discretionary sector (XLY). sPandemic-era excess savings have evaporated, consumer sentiment is at a six-month low of 67.4 points, and retail sales are stagnant. Any company that thrives under these conditions should do so Something true.

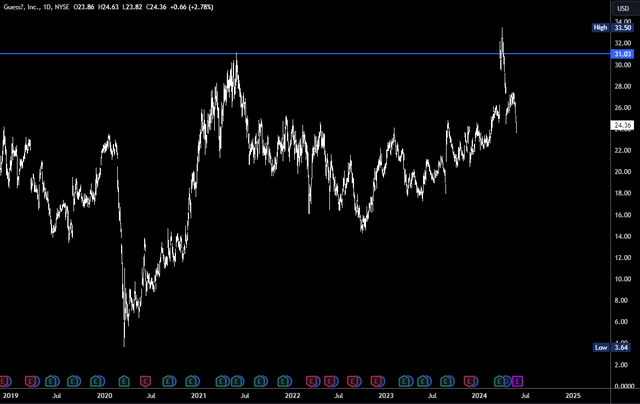

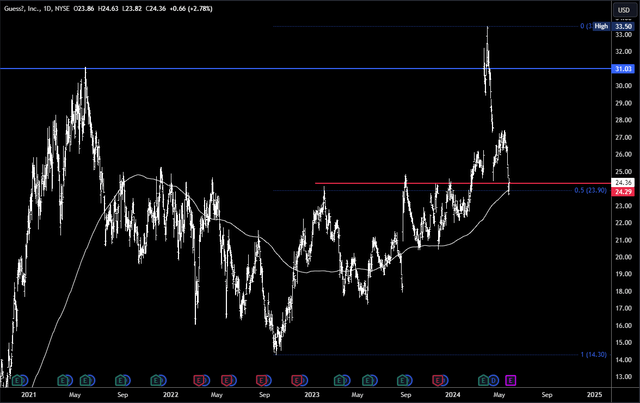

Guess? (New York Stock Exchange: GES) So it caught my attention when it hit 10-year highs in April.

Relative strength in GES

There are a lot of consumer discretionary stocks and apparel stocks on downtrends. Inflation has pressured margins and dampened consumer spending. However, GES managed to break out and made a new 10-year high in April.

GES daily chart (TradingView)

The new high above $31 has led to a strong reversal and GES is now seeing a sharp decline, but this could be a buying opportunity if the underlying fundamentals remain positive.

GES – Impressive performance in Q4 and FY2024

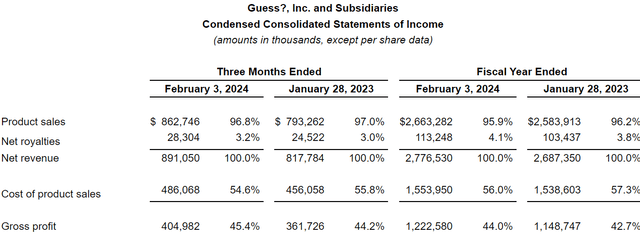

Fiscal 2024 results were released on March 20 and included crucial holiday sales results. Q4 was impressive.

Revenues increased to $891 million, an increase of 9% in both U.S. dollars and constant currency; Operating margin 16.3%; 14.6% GAAP adjusted operating margin of $1.71 and adjusted EPS of $2.01

In fact, the board was so pleased that it declared a special dividend of $2.25 per share. The fourth quarter capped a strong year with 3% revenue growth.

Estimate FY24

Paul Marciano, co-founder and creative director, spoke about GES’s “brand elevation strategy” and it seems to be working. Guess? She’s positioned her brand in a sweet spot – not so luxurious or expensive that it’s out of Gen Z’s reach, but still exclusive and trendy. My sixteen-year-old son owns several Guess t-shirts and alternates them with Calvin Klein and Hugo Boss when he goes out with friends.

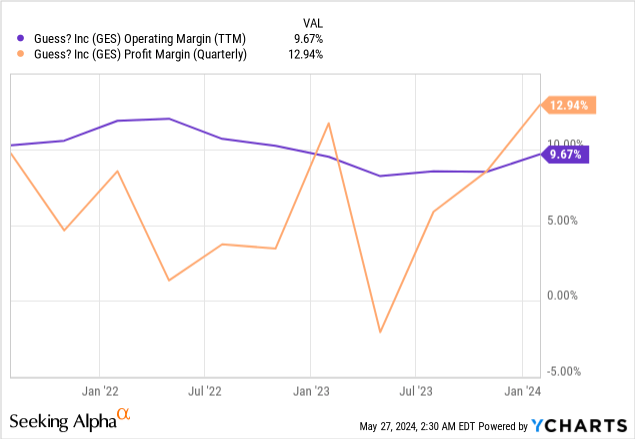

Due to Gen-Z approval, GES has good pricing power. The margins in the fourth quarter were a big plus.

GAAP operating margin in the fourth quarter of fiscal 2024 increased 3.6% to 16.3%, from 12.7% for the same quarter the prior year, driven primarily by higher revenues and pro forma margins and lower expenses, including a net positive impact From the derivatives litigation settlement previously disclosed to stockholders, partially offset by the unfavorable currency impact and higher write-downs.

During FY2024, margins were flat, but this can be viewed as a positive in a high inflation environment. GES has been able to maintain its margins through high initial profit margins and controlled expenses. I recently wrote about Burberry ( OTCPK:BURBY ) which saw margins collapse from 20.5% to 14.1% in FY24.

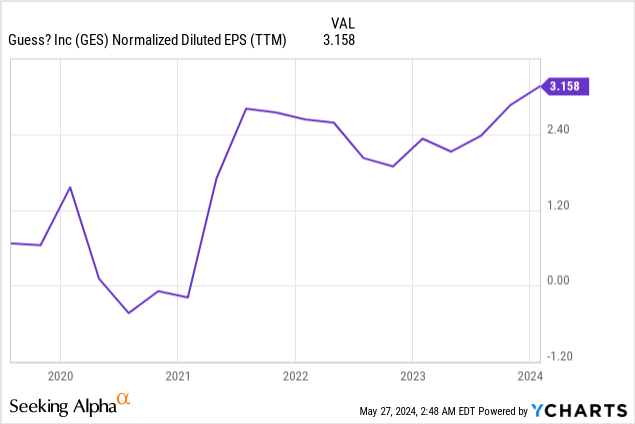

Earnings per share rose to $3,158 which was last achieved in 2012. This gives GES a T/T ratio of 12.9.

This would be an attractive valuation if GES is set to grow at a similar pace in fiscal 2025. Unfortunately, the outlook is less rosy.

Black clouds on the horizon

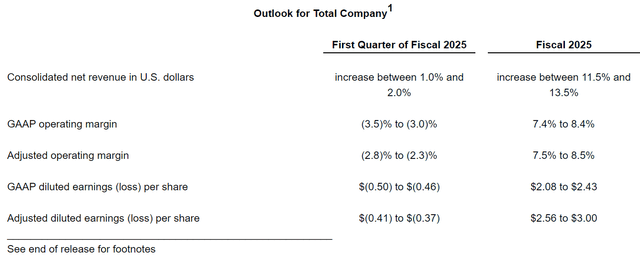

Guidance for FY25 is mixed. Revenue growth is expected to continue in the low single digits, but a number of headwinds are expected to hurt margins and earnings per share.

Guess?

First quarter margins are expected to be negative. When asked about this on the earnings call, COO/CFO Marcus Neubrand said:

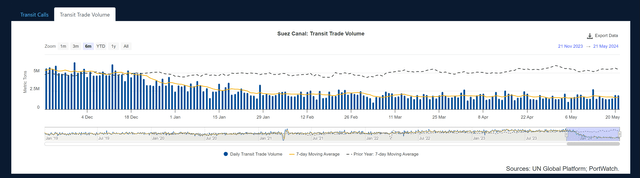

…The Red Sea crisis is having an impact on our freight rates and on the inbound costs that we included in today’s guidance, as we expect freight rates to increase, especially in the first half of fiscal year 2025, and were therefore expected to be managed in the second half of the year. Fiscal 2025.

Marcos said this last March, but the situation in the Red Sea has not improved.

portwatch

Rag and Bone Acquisition – Guess’s first ever acquisition? -It is also likely to distort some results.

…the rag and bone acquisition, we expect it to be a modest accretion, so there will be some margin dilution from the rag and bone. There are some other benefits that we have included in our guidelines, such as KYDC and Kentucky DC processes being outsourced to a logistics partner. All of this is incorporated into the guidance we’ve given of an operating margin that we see between 7.5% and 8.5% for fiscal year 2025.

Sales in North America were also a weak point, and with consumer data declining, it could get worse.

EPS for FY25 is expected to fall to a range of $2.56-$3.0.

Put everything together

In the long term, GES is in a strong position. Growing revenues and stable margins are an attractive prospect in a sector where many companies are struggling. Most of all, guess what? It’s trendy with Gen-Z and the brand is located in a sweet spot for high street sales.

In the near term, headwinds expected in the first half of 2025 lead to a decline. This seems justified because EPS could shrink by 20%. But where exactly could GES offer an attractive entry?

The price is already down 30% from the April high to $24 which is potential support at the 200-day moving average and the 50% retracement of the 2022-2024 high. It is also an area of 2023 highs.

Technical analysis jess (TradingView)

This looks like an attractive entry, even though first-quarter results are due on Thursday, May 30. Revenues are expected to be $577 million, along with earnings per share of -$0.38. This has lowered the bar considerably and can lead to a win. Moreover, the 30% decline since the April high has at least factored in some of the expected bad news. The risk is that a mistake or weak guidance could break $24 and the next convincing support level is $20.2.

I personally like GES, but industry headwinds mean I’m in no rush to take the risk of buying before earnings. I would either buy above $24 if the release is positive, or near $20 if it is negative.

Conclusions

The relative strength in GES reflects its strong long-term fundamentals. The near-term decline should serve as a buying opportunity as industry headwinds should be temporary and improve in the second half of 2025. Whether the decline continues to $20 or reverses from $24 will likely depend on earnings later this Week and revised guidance.