Monte Racusen/Digital Vision via Getty Images

Investment thesis

More recently, H. F. Sinclair (New York Stock Exchange: Dino) announced a $1 billion stock buyback program and a regular quarterly dividend of $0.50 per share, indicating the company’s intention to return capital to shareholders. Despite this attractive return on capital For shareholders, I continue to believe the share price fully reflects these benefits and I rate the shares as fair value. The action continues to perform well, but nothing special enough to get excited about. With its attractive dividend and cash flows, profitable business model, and fair valuation, I recommend investors continue to hold shares at today’s prices.

Company overview

HF Sinclair, according to its annual report, is “an independent energy company that produces and markets high-value light products such as gasoline, diesel fuel, jet fuel, renewable diesel and other specialty products.” As an oil refining company, it “operates throughout the United States through seven complexes refineries, and also has production facilities in Canada and the Netherlands,” she said website.

The company classifies its operations into five segments: “Refining, Renewable Energy, Marketing, Lubricants & Specialties, and Transportation & Conversion.” Like any refinery, HF Sinclair makes money by converting crude oil into usable products such as gasoline, diesel and jet fuel. The company says it has “678,000 barrels per day of crude oil processing capacity” and owns a family of brands that include various lubricants, specialty products and various specialty oils on its website.

Renewables refers to our Cheyenne Renewable Diesel Unit Operations, which primarily manufactures renewable diesel fuel that is more environmentally friendly than traditional petroleum diesel fuel. According to their website, their renewable diesel “produces 50% to 80% lower greenhouse gas emissions than petroleum diesel,” and the company produces “380 million gallons of renewable diesel energy annually across three facilities,” according to the website.

The marketing refers to “sales of branded fuel to Sinclair-branded locations in the United States and licensing fees for use of the Sinclair brand at additional locations across the country.” These branded fuel sales are marketed under the Sinclair Oil brand, which is sold through “1,500 independent Sinclair-branded gas stations in 30 states in the U.S.,” according to their website.

Lubricants and Specialties refer to “products such as base oils, white oils, specialty products, and finishing lubricants” that the company sells. The term “midstream” refers to “logistics and refinery assets consisting of petroleum products, crude oil pipelines, terminals, tanks, loading facilities and refinery processing units.”

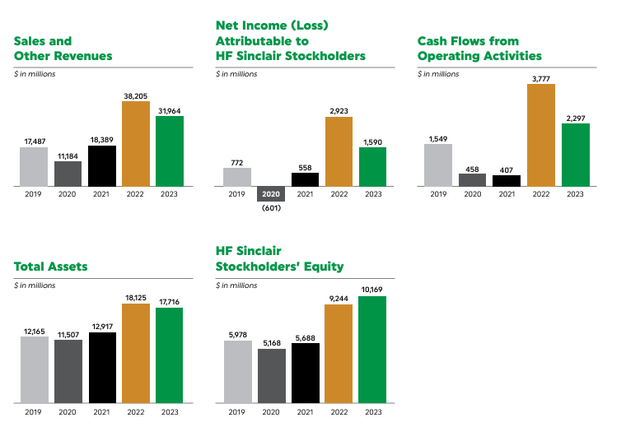

In short, I see the business as being very cohesive in terms of vertical integration, with control over many parts of the refining process. They enhance brands and help handle logistics and transport their finished products to the end consumer. Its fundamental performance is heavily influenced by the price of oil, as it earns the difference between purchasing crude oil, refining it, and selling the finished product to consumers. This business is currently very profitable and generates significant profits for investors, despite the fact that oil prices have risen considerably. Their vertically integrated operations should allow them to operate more efficiently compared to their competitors, and has helped HF Sinclair increase assets and shareholder equity over the past few years.

Annual report 2023

First quarter earnings review

HF Sinclair reported first quarter 2024 earnings on May 8, 2024, with this press release:

- Net income attributable to HF Sinclair shareholders of $314.7 million, or $1.57 per diluted share, and adjusted net income of $142.3 million, or $0.71 per diluted share, were reported for the first quarter

- EBITDA of $617.4 million and adjusted EBITDA of $399.1 million were reported for the first quarter.

- It returned $269.0 million to shareholders through dividends and stock repurchases in the first quarter

I think adjusted net income is a better number to rely on, because it more accurately depicts a company’s true profitability. It “excludes non-cash below-cost or market inventory valuation adjustments, HEP’s share of Osage’s environmental remediation costs, acquisition integration and regulatory costs,” according to the press release.

When using adjusted numbers, investors can see that earnings are not as good as they seem. Both net income and adjusted EBITDA are much lower, which gives me pause on the accounting H.F. Sinclair reports. By excluding the benefit of using a lower inventory valuation, adjusted earnings are much lower, which leads me to believe that the company is benefiting from cheap crude oil purchased before oil’s big rally.

Earnings can contain a lot of accounting noise like this, so investors can look at cash flow to get a better picture of reality. Cash flow from operations was $316 million, which equates to adjusted EBITDA of $400 million. Therefore, investors can see that cash flows remain resilient and have increased on a quarterly basis of $230 million, or a 37% increase.

Going forward, I expect dividends to hold up and buybacks to continue, demonstrating management’s strong intent to return capital to shareholders. However, at this price, I think the buybacks are a bit suboptimal as the shares appear to be fully priced out. However, the company continues to deliver strong performance and reports significant net income in the quarter due to “a lower cost or market inventory valuation benefit of $220.6 million.”

Spreads should remain stable

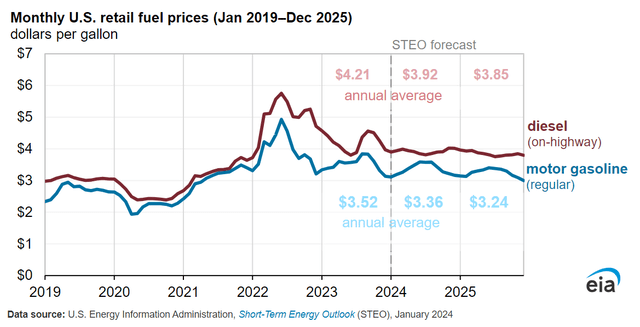

I think oil prices should remain steady, so spreads should remain relatively stable as well, assuming demand for refined petroleum products will remain the same. Oil prices should remain somewhere between $70 to $90 for the next year or two, based on EIA projections that “voluntary OPEC+ crude oil production cuts and ongoing geopolitical risks will keep the Brent crude spot price near $90 per barrel for the remainder of Year 2024.” Before falling to an average of $85 per barrel in 2025 as global oil production growth picks up.

Despite oil prices being quite high, refiners are seeing strong stock price rises and general optimism as they manage their spreads smartly. Many of HF Sinclair’s peers are rising to new relative highs, as Bank of America’s Doug Leggett says in the same SA news article:

“For the next seasonal phase of elevated refining volatility, we believe mid-cycle upside risks and tailwinds from another round of earnings revisions see U.S. refiners positioned favorably for at least the next period of seasonal gasoline strength,” Bank of America’s Doug Leggett wrote. Of America.

My view is that refineries should have a strong performance in 2024 due to stable gasoline demand, and stable crude oil prices, which should lead to a stable spread. The EIA expects gasoline and diesel prices to remain flat through 2025, which leads me to believe HF Sinclair’s earnings should remain flat for next year.

Environmental impact assessment

Investors should be able to rely on dividends and buybacks to continue as HF Sinclair benefits from a period of stability and profits accordingly. Despite the rise in crude oil prices, I ultimately think HF Sinclair will have a good year or two as it reaps the rewards of a favorable environment for oil refineries. Therefore, this is a good time to hold HF Sinclair shares as cash flows continue to flow.

Valuation – Fair value $60

For this valuation, I will assume that most of the fundamental metrics are holding steady, as I believe the company has reached its peak in terms of earnings and cash flow. Stable spreads and increasing returns of capital to shareholders indicate that management knows they can no longer intelligently reinvest profits at high rates for growth, so they are returning them now while they still can.

Using earnings estimates from Seeking Alpha, I think the company could earn $6 per share for the next few years, due to good market conditions for its oil refineries and continued efficiency gains from the Holly Energy Partners acquisition.

Apply a 10x sector multiple to $6 per share to get a fair value of $60 per share, which is close to the current stock price. I don’t see much upside from here and I expect the stock to perform in line with the broader market. Buybacks don’t look very attractive given that the fair value shares look high, so I think management should pay the dividend aggressively instead.

Although the cash flows are huge now, I wonder if they are sustainable. Oil refineries are known to be highly cyclical, with HF Sinclair seeing cash flows as low as $400 million during the pandemic. Many investors may expect cash flows to grow indefinitely, but my understanding of the cyclical nature of oil and refineries leads me to believe that a potential decline in refineries could put cash flows at risk. Overall, I simply question the sustainability of the cash flows over the long term, which leads me to rate the stock as Neutral.

Risks

It is known that oil refineries are cyclical and are affected by the general economy, oil prices, oil refining capacity and gasoline demand. Predicting these variables is extremely difficult over the long term, and a decline in any of these variables could negatively impact HF Sinclair’s cash flows. Investors should be careful about projecting the past onto the future, as the future may look very different. The so-called “golden age” of refineries may not last long, and certainly not forever in my view.

Environmental regulations could limit HF Sinclair’s profits as it must comply with new rules on crude oil refining. Government agencies have significant power to determine new regulations that could prevent HF Sinclair from expanding.

The growing popularity of electric vehicles will likely make petrol and diesel obsolete in the long term. HF Sinclair may fail to adapt to changing trends as gasoline may be in long-term decline as electric vehicles become more affordable to the general population.

HF Sinclair contract

I’m fascinated by oil refineries because of their strong cash flows and good earnings, but at the same time wary because of their cyclical nature. At least in the near to medium term, I see shares holding up well at around $60 per share, but I’m unwilling to expect anything higher. At the very least, shareholders should continue to retain their dividends after Q1 earnings as they will be well rewarded, but I wouldn’t recommend buying more shares at today’s price.