FG Latin Trade

Investment thesis

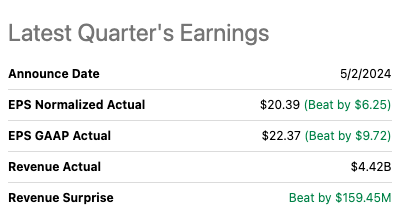

Holding Book (Nasdaq: PKNG), the travel giant behind Booking.com, Priceline and Kayak reported a strong first quarter of 2024. Revenue rose 17% year over year to $4.4 billion, beating analysts’ expectations. Earnings per share (EPS) also jumped significantly to $20.39, compared to $7.07 last year. Q1 2023. Total travel bookings reached $43.5 billion, reflecting a 10% increase. Room nights booked increased 9% year over year. The company also announced A Divided money From $8.75.

Searching for alpha

It was a strong earnings report and Booking stock rose more than 9% in after-hours trading following the report’s release. During the earnings call, Booking’s CEO said they are seeing high growth in “high-frequency” users and increased loyalty program enrollment. The company remains optimistic about continued demand for travel, especially in the summer season. Airline ticket bookings witnessed a significant increase of 33% year-on-year.

we See the encouraging behavior from our Genius Tier 2 and 3 travelers, including higher frequency and a higher direct booking rate than we see in our business overall.

Besides the positive results, it is important to take into account some risks. Booking is facing increased regulatory scrutiny in Europe, where regulators call it a “gatekeeper” and open investigations into potential anti-competitive practices. I believe this should not have an impact on profits and regulatory scrutiny usually comes after larger companies like Booking.

In a separate article, I recently explored the contrasting fortunes of Booking’s distant second competitor, Expedia (EXPE). Although bookings exceeded expectations, Expedia underperformed, particularly in total bookings for its platform. I think Booking is gaining market share from Expedia.

Booking in the first quarter of 2024 exceeded analysts’ expectations, sending shares higher. I find that their leadership position and focus on direct bookings, supplier partnerships and especially innovation in generative AI for customer experience, can lead to further growth in the future. I also find the company a strong candidate for a growth at a reasonable price (GARP) strategy. However, caution is advised, as as you will read later, I find the stock to be fair or even overvalued at the moment. Furthermore, while long-term growth is possible due to their leadership position and financial resources, an all-time high share price necessitates a conservative approach.

So, considering all these factors, I would initiate coverage with a “buy cautious” because I would buy the stock on weakness.

Management evaluation

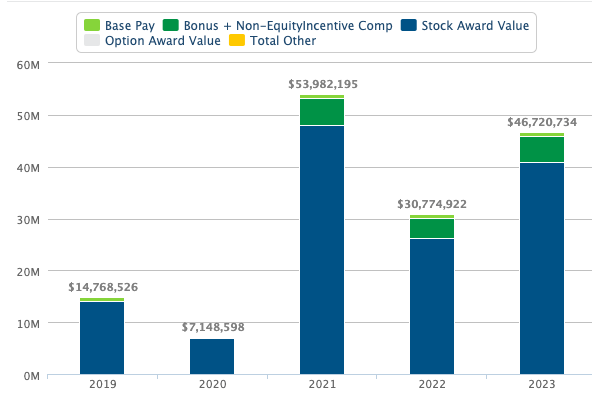

Glenn Vogel, CEO of Booking Holdings, brings 24 years of professional experience to the company. He has overseen Booking’s growth strategy, including key acquisitions, and currently leads the company’s global operations. Employees seem to appreciate his leadership, which is reflected in the high Glassdoor ratings. Interestingly, most of his compensation comes in stock options, aligning his financial success with the company’s long-term performance. This pay structure suggests to me a strong focus on Booking’s future success, although it also makes him one of the highest-paid CEOs in the industry.

Salary.com

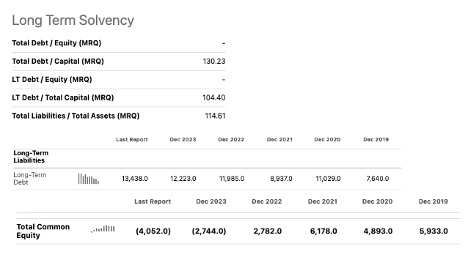

Ewout Steenbergen takes over as CFO at Booking Holdings, where he inherits a company with a complex financial situation. Sequestration is buying back shares, financed by issuing bonds, which has hurt free cash flow (FCF). While I don’t find this method of stock buybacks necessarily negative as a one-time event to show confidence in the company’s future, it is concerning given that the company’s debt has been steadily rising post-pandemic and the stock is now negative.

I believe that every dollar spent on interest payments is a dollar not available for growth initiatives. Steenbergen will need to handle this situation effectively to ensure Booking maintains its financial health while promoting future success.

Now we turn to our cash and liquidity position. Our first quarter cash and investment balance of $16.4 billion increased versus our fourth quarter ending balance of $13.1 billion due to $3 billion of debt issuance in the first quarter and $2.6 billion of free cash flow generated in the first quarter. This was partially offset by the $1.9 billion return of capital including stock repurchases and dividends we initiated this quarter as well as $315 million in additional stock repurchases to satisfy employee withholding tax obligations.

Searching for alpha

Overall, I find Booking to be a mixed bag. CEO Glenn Vogel’s impressive career includes strategic acquisitions and high employee morale. His large stock compensation aligns his interests with long-term success, even though it makes him the highest-paid CEO in the industry. However, the financial position of the company requires monitoring. The new CFO Ewout inherits a situation in which bond-financed stock buybacks reduced free cash flow and impacted the stock into negative territory, limiting growth resources. Furthermore, the company has also started paying a dividend this year, which I find positive at the moment because it is also an indication that management has not found other ways to grow. Taking all the factors into account, I give management a “meets expectations” rating. Fogel’s leadership is strong but future growth plans beyond stock buybacks are critical.

glass door

Cooperative plan

Booking is the leader in the online travel agency (OTA) market by offering a wide range of flexible accommodation, from budget-friendly options to luxury stays. This serves a wide range of travelers. It also strengthens its grip on the market by offering flexible booking options and rewarding repeat customers.

They have been constantly growing, expanding into new markets and acquiring complementary businesses to expand their offerings beyond just accommodation. Additionally, the company is prioritizing investment in technology such as artificial intelligence and machine learning to help users plan their vacations and personalize their experience to improve search results.

I created a table comparing my current booking strategy to some current competitors in a previous article here but I’m also updating and adding it here:

|

Expedia (EXPE) |

Booking Holdings (BKNG) |

Airbnb |

Trip.com (TCOM) |

|

|

Market share (accommodation bookings) |

15% |

27% |

13% |

10% |

|

Cooperative plan |

Focuses on bundled travel packages and brand diversification. |

Aggressive on direct bookings and supplier partnerships. Focus on enhancing the loyalty program through artificial intelligence. Become a one-stop shop for all your travel needs. |

Changing traditional hospitality with unique stays and expanding experiences |

Focused on the Asia Pacific market, strong mobile presence, and expanding vacation rentals. |

|

Competitive advantage |

Extensive network of travel suppliers, brand recognition and loyalty program (OneKey) |

Largest online accommodation marketplace, strong mobile presence, and effective marketing. Solid finances. |

Unique accommodation options and a growing experiences market |

Strong brand recognition in Asia, competitive pricing, and focus on mobile users. |

Source: From the SeekingAlpha presentations website

Market Share: Statista (2023)

There are several key factors that distinguish Booking from its competitors. Compared to Expedia, Booking features a wider range of flexible accommodations, especially in non-Western markets. While Airbnb offers unique accommodation options, Booking caters to those looking for standardized hotel experiences. Finally, Booking has a clear advantage in user experience and global reach over Asia-focused Trip.com.

However, Booking also faces some challenges. Their reliance on commissions from accommodation providers could limit profit margins if these rates fall. Additionally, their focus on hotels may not appeal to travelers looking for a unique experience. Finally, strict regulations in some regions may hinder Booking’s ability to operate or collect data.

evaluation

Booking is currently trading at around $3,800, trading at all-time highs since earnings were last reported in early May.

To evaluate its value, I used a discount rate of 11%. This rate reflects the minimum return an investor would expect to receive for his or her investment. Here, I use a risk-free rate of 5%, plus an additional risk premium for holding stocks versus risk-free investments, and I use 6% for this risk premium. While this could be improved further, either lower or higher, I only use it as a starting point to get a measure of unbiased market expectations.

Then, using a simple 10-year, two-stage DCF model, I inverted the formula to solve for the high growth rate, which is the growth in the first stage.

To achieve this, I assumed a final growth rate of 4% in the second stage. Predicting growth beyond a 10-year horizon is challenging, but in my experience, the 4% rate reflects a more sustainable long-term path for mature companies that should be close to historical GDP growth. Again, these assumptions could be higher or lower, but from my experience I feel comfortable using a 4% rate as the base case scenario. The formula used is:

$3,800 = (Sum^10 FCF (1 + “X”) / 1+r)) + TV (Sum^10 FCF (1+g) / (1+r))

Solution for g = 14%

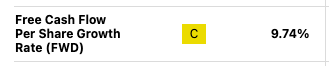

This indicates that currently market prices for BKNG FCF will grow at a rate of 14%. According to Seeking Alpha analysts’ forecasts, FCF is expected to grow by 9.74%.

Searching for alpha

Therefore, I think BKNG is overvalued at this point. However, it is important to note that the company has artificially bought back shares by issuing debt which affects the FCF growth. I would be a buyer at a weak point because I believe the company has a competitive advantage and will maintain its leadership in the OTA industry.

Technical Analysis

BKNG has jumped about 10% since earnings were last reported in early May. Its RSI appears to be under control at around 56 after crossing its 14-day average of 49 and is pointing to continue rising indicating that the stock may continue to increase in value. BKNG’s all-time high is around $3,904; This represents a move of approximately 2% from current levels. Momentum according to SeekingAlpha is positive:

Searching for alpha

I think BKNG will reach all-time highs due to positive momentum, but once there, it will remain neutral and move in a range between approximately $4,100 and $3,700. I would be a buyer of the stock on any weakness despite the current challenges because I believe FCF will improve faster than expected based on management’s ability to generate excess EPS over time.

Searching for alpha TradingView

Next earnings are August 5th

He stays away

Booking impressed with a strong first quarter, beating analysts’ expectations. Although the company has a strong track record, is led by an experienced CEO and has high employee satisfaction, I would exercise some caution. The company is positioned for future growth and appears to be gaining market share from its competitors. However, the stock price is at an all-time high, and it has recently begun paying dividends, but free cash flow is declining due to debt-financed stock buybacks. Overall, Booking is a leading company with a strong fundamental even though the share price appears inflated. Therefore, despite the mixed signals in the stock, I would tend to initiate coverage with cautious buying especially in case of any weakness.