High-Quality Energy Input – Unleash double-digit productivity with Kimbell Royalty Partners

Valerie Loisello

introduction

I love oil and gas stocks.

So far, this is not surprising.

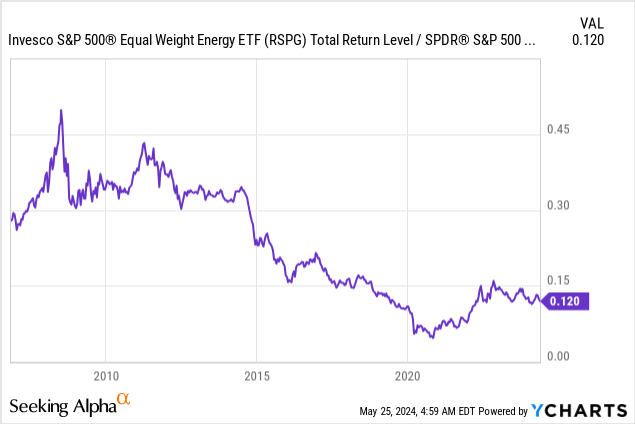

After a period of underperformance lasting more than a decade, energy stocks have not underperformed the S&P 500 since 2019, as the ratio between equal weight Energy Rolling Fund (RSPG) The S&P 500 index is shown below.

Given factors such as strong long-term demand, increasingly favorable supply developments, and valuation advantages, I believe fossil fuels are the place to be for the foreseeable future.

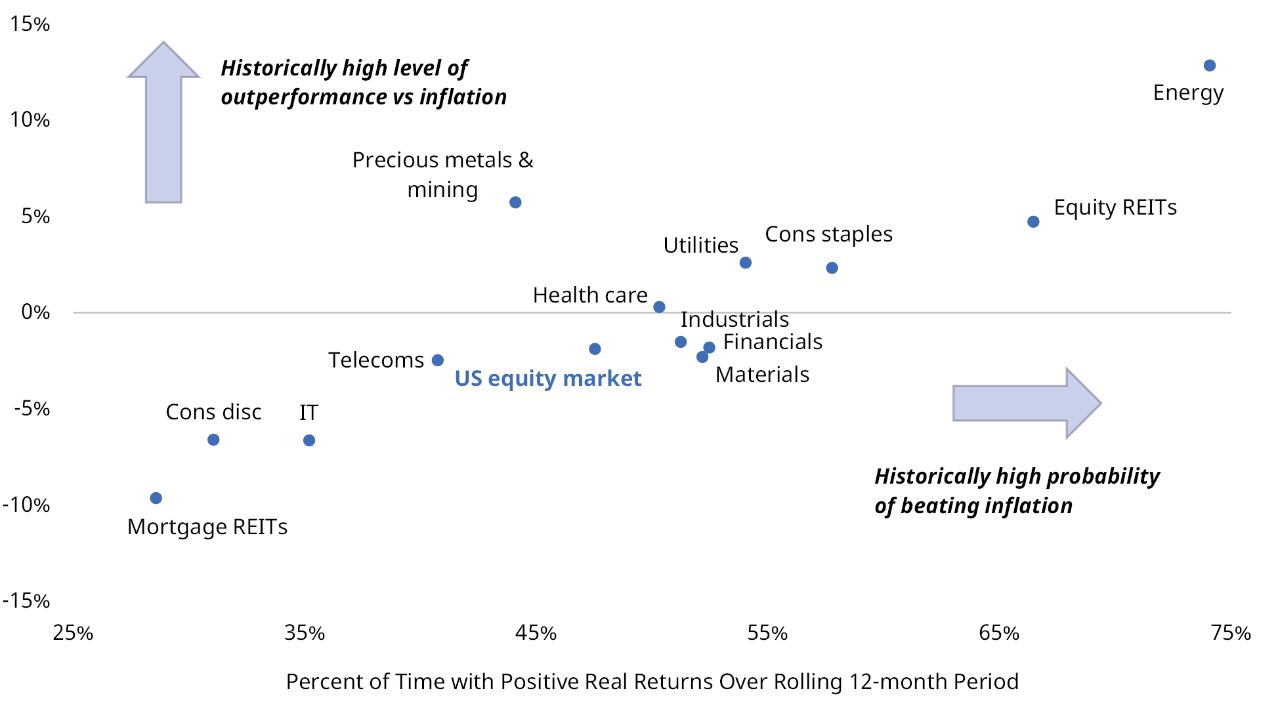

Furthermore, historically, energy stocks are the best place to be when inflation rises.

Hartford Funds

While the entire energy sector has tailwinds, I like one sector a lot. This sector is royalty companies.

Royalty companies are organizations that own mineral rights. They allow oil and gas producers to use them in exchange for a production fee oil and gas.

This allows them to benefit from oil and gas production without having to deal with capital expenditures and operational risks.

I love this region so much that I made Texas Pacific Land (TPL), one of the largest landowners in the Permian Basin, my largest investment, representing 12% of my entire investment portfolio.

After discussing some of the royal plays, readers raised a lot of stock. That company Kimball Royalty Partners, L.P. (New York Stock Exchange: CRB)the star of this article.

Hence, in this article I will explain how KRP makes money, what makes it so special, and why investors have a realistic chance of receiving a double-digit distribution (dividend).

So, let’s dive into the details!

What makes Kimble so special?

First of all, many European investors – like myself – may not be able to invest in Kimball due to its tax structure.

Unlike Texas Pacific Land, it is not a C-Corp. However, it is also not a “traditional” key boundary partnership.

While the company does not issue a K-1 but a Form 1099-DIV instead, they are master limited partnerships with a variable rate.

This also means that dividends are called “distributions”, and shares are called “units”.

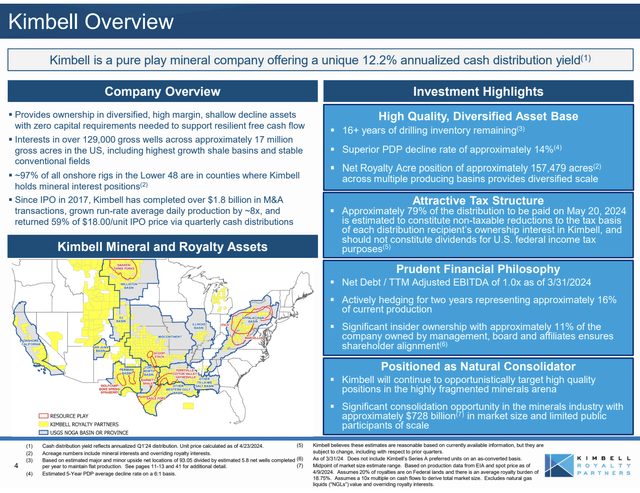

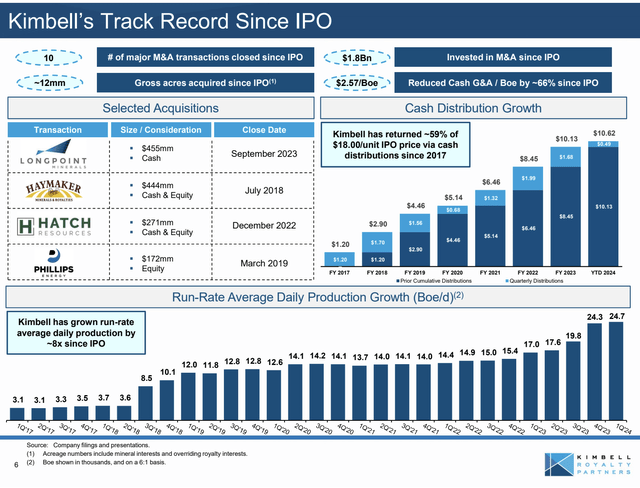

With that in mind, Kimbell was founded in 2015, and began this year with mineral interests and royalty interests in approximately 12.2 million gross acres and majority royalty interests in 4.7 million gross acres.

- Mineral interests These are perpetual royalties that give the company ownership of all oil and natural gas found beneath the surface. Essentially, these interests allow KRP to lease exploration and production rights to oil and gas companies, and receive royalties from production without having to deal with operational costs. While the company has no rights to the surface or water, it has access to the most valuable commodities and a massive cost advantage – forever (!).

- Transcending royalty The interests are free production rights that are carved out of existing leases. These interests allow KRP to obtain a fixed percentage of production revenues. These typically last as long as the underlying lease remains active.

In other words, the company is what you call a “pure metals company.”

Kimball Royalty Partners LP

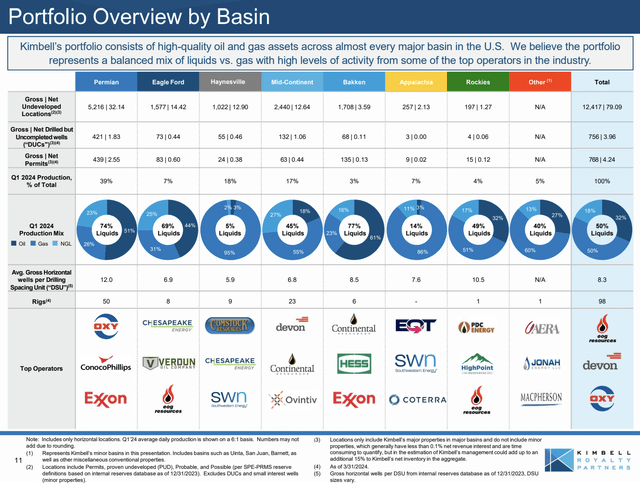

Furthermore, its assets are well diversified, with operations in all major basins, including the Permian Basin, Eagle Ford, Hinesville, Bakken, Appalachia, and others.

The overview below shows the breakdown of the company’s production (i.e. 39% of production comes from the Permian Basin) and its largest operators, which include some of the largest US energy companies.

Kimball Royalty Partners LP

In these areas, it has a drilling reserve of more than 16 years – excluding any additional discoveries or mergers and acquisitions.

When talking about mergers and acquisitions, the company’s strategy to improve cash dividends in the long term is based on three pillars:

- Acquisitions: The company leverages its relationships with sponsors and contributing parties to purchase high-quality minerals and royalty benefits that allow it to increase production over time.

- Organic growth: The company benefits from the continued development of its properties by third-party operators to improve reserves and production without additional capital expenditure.

Since the first quarter of 2017, the Company has improved average daily production growth from 3.1 barrels of oil equivalent (“BOE”) to 24.7, and has added inventory through four major acquisitions.

Kimball Royalty Partners LP

- Conservative capital management: In relation to the above two points, the Company aims to maintain a sound capital structure to support long-term growth and financial flexibility. In the absence of a sound balance sheet, a company cannot engage in mergers and acquisitions or distribute its cash to unitholders.

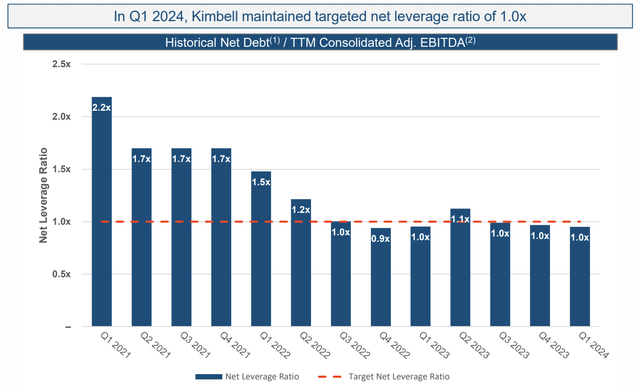

Since early 2021, the company has reduced its net leverage ratio from 2.2x to 1.0x. It has maintained its leverage ratio below its target since 3Q22 (including one outlier).

Kimball Royalty Partners LP

With that in mind, let’s take a closer look at shareholder benefits.

Lots of shareholder value

The company is doing very well at the moment.

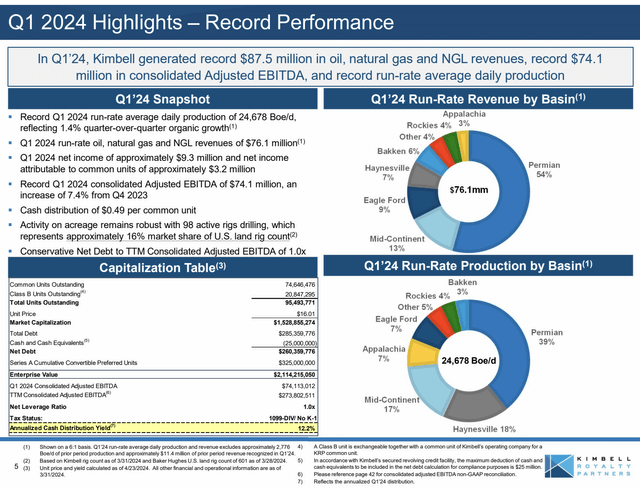

In the first quarter, the company reported impressive numbers, including record revenue ($87.5 million, +4.2% qoq), record EBITDA, and a throughput of 24,678 BOE per day (record), which Mean organic growth of 1.4%. Compared to the fourth quarter of 2023 (5.6% y/y).

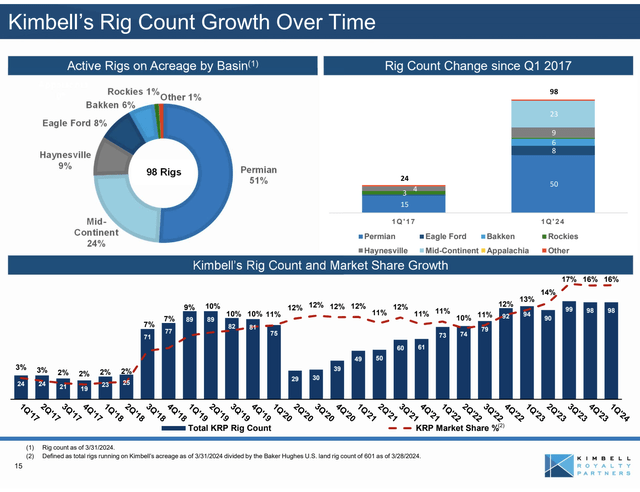

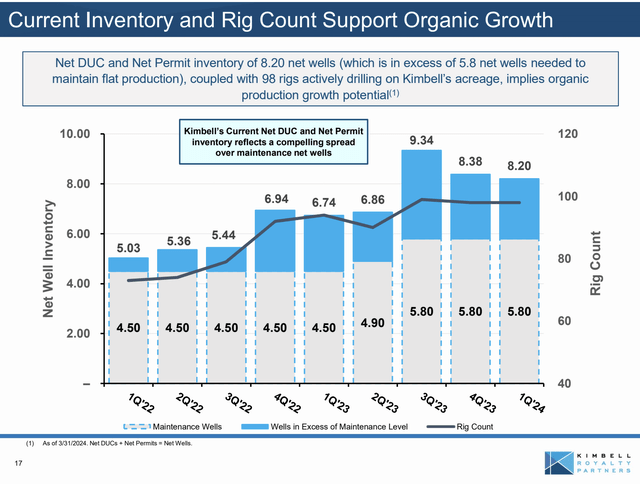

Furthermore, the company ended the quarter with 98 rigs active in its territory. This represents a 16.3% market share of all land-based drilling rigs in the continental United States!

Kimball Royalty Partners LP

As the portfolio overview in the first part of this article showed, 50 of these rigs are located in the Permian.

Kimball Royalty Partners LP

The company also confirmed its guidance for 2024, with an average daily production target of 24,000 barrels of oil per day.

It also used the earnings call to make clear that it remains optimistic about its development prospects, supported by the number of rigs actively drilling on its acreage and positive operator sentiment, particularly in the Permian Basin.

We continue to believe that industry trends, overall energy demand and positive operator sentiment represent a positive outlook for revenues, the mineral acreage and Kimbell specifically. We are excited about our drive through 2024, and are focused on a long-term horizon of continued growth and opportunities to enhance unitholder value. – KRP 1Q24 earnings call

The company remains in a great position to grow its business and reward shareholders, especially with the support of good demand, which is exactly what it has been doing.

This includes sufficient drilled but incomplete (“DUC”) wells to support organic growth.

Kimball Royalty Partners LP

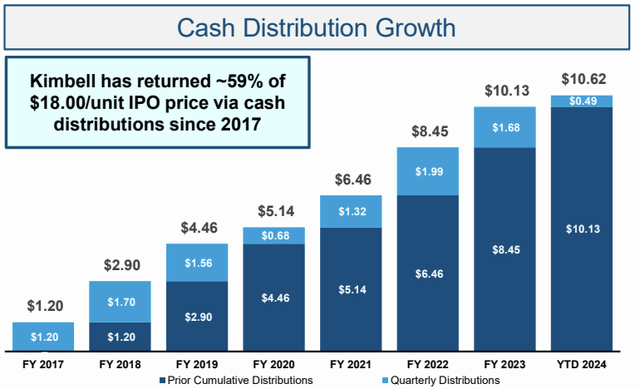

Regarding shareholder income, in the first quarter the company announced a cash distribution of $0.49 per unit.

This represents 75% of the cash available for distribution, with the remaining cash used to reduce borrowings under the senior secured revolving credit facility.

This distribution is 14% higher than in Q4 2023 and implies a return of 12%.

Kimball Royalty Partners LP

Furthermore, and this is somewhat unique, 79% of this distribution will be considered a return of capital, which is not subject to dividend taxes.

However, the company has an attractive advantage – lots of revenue at low prices.

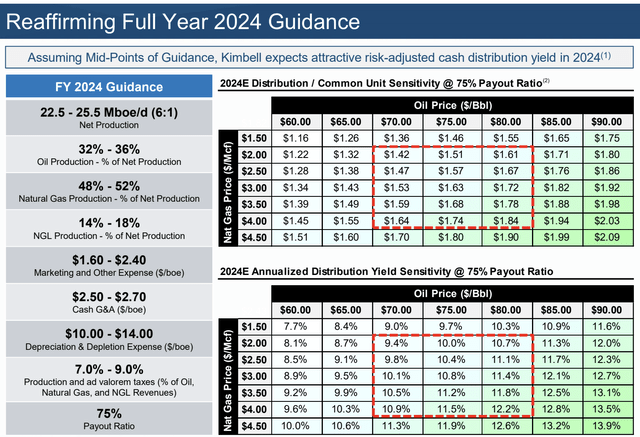

Using the helpful overview below, we see the company’s expected distribution at various oil and gas prices – based on 2024E production numbers, a 75% payout ratio, and the current unit price ($16.42).

- In the Current environment At $80 for WTI and $2.50 for Henry Hub, the company has an implied annualized return of $1.67, which equates to $0.42 per unit per quarter. This means a 10% return based on the current price.

- in Very favorable pricing environment From $90 for WTI and $4.50 for Henry Hub, this figure rises to $2.09 (12.7% yield). Personally, I think we could look at WTI near $100 and $5.00 at Henry Hub once we get stronger global growth.

- even in Low price environment ($60 for WTI, $1.50 for Henry Hub), the company can distribute $1.16 per unit. This translates to a return of 7.1%!

Kimball Royalty Partners LP

This is one of the most favorable income projections of any North American energy stock, making it a great source of income and favorable returns for its investors – especially if oil and gas prices rise over time.

Based on the company’s attractive distribution outlook – even at low prices, I give the company an A Solid deal The rating, because it is fully consistent with my expectations for long-term support for production growth and pricing benefits.

He stays away

For various reasons, investing in oil and gas stocks remains the best option for me.

Among these companies, royalty companies stand out, offering significant benefits without the operational risks faced by oil and gas producers.

Kimbell Royalty Partners is particularly attractive given its diversified assets, strategic growth through acquisitions and impressive distribution outlook.

When favorable market conditions are added, I rate KRP a Solid deal.

Pros and Cons

Positives:

- Attractive income: KRP offers a large dividend, with potential double-digit returns even at low commodity prices.

- Diverse assets: The company operates across major basins, including the Permian Basin, Eagle Ford, and Bakken.

- Low operational risk: As an equity company, KRP benefits from production without dealing with high capital expenditures and operational risks.

- Tax advantages: Currently, a significant portion of the distributions is a return of capital, which reduces the tax liabilities of KRP investors.

cons:

- Tax structure: Non-US investors, like myself, may face difficulties due to the variable rate limited partnership structure. However, for others, it can be useful.

- Reliance on commodity prices: Earnings and distributions are very sensitive to fluctuations in oil and gas prices.