Miscellaneous Photography/iStock Editorial via Getty Images

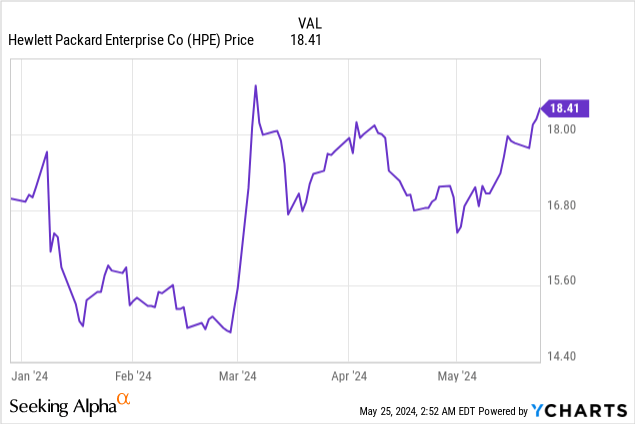

HP Foundation (New York Stock Exchange: HBE) The stock rose about 20% after it expanded its partnership with Nvidia (NVDA) and since it has fluctuated in a range of $16.5 to $18.5 as shown in The table at the bottom.

Now, it was already integrating AI into its products long before OpenAI’s ChatGPT, and its potential merger with Juniper Networks (JNPR) puts HPE in a better position to reap opportunities in hybrid AI and cloud networking as I explained in an article. Previous piece in January.

At the time, I was optimistic, but this thesis, which comes ahead of the company’s second-quarter 2024 (FQ2’24) financial results on June 4 and is intended to provide an opportunity update, emphasizes caution. Hence, more visibility is needed after the revenue decline it suffered during the fiscal first quarter of 2024 It suffered relatively more than its industry peers.

Returning to price action, I explain how it is justified by outlining the benefits associated with generative AI.

Opportunities in Edge-to-Cloud with Gen AI

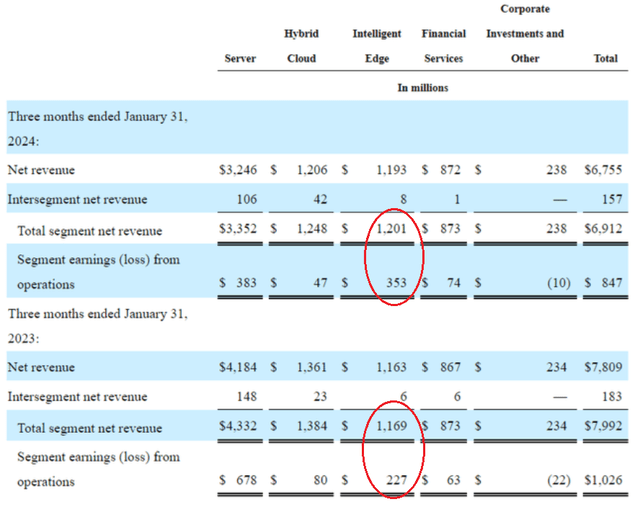

First, as shown in the table below, the company boasts an Intelligent Edge segment where sales grew 2.7% year over year or from $1,169 million to $1,201 million. More importantly, earnings from operations grew by 55.5%, or from $227 million to $353 million, demonstrating that this is a highly profitable segment for a company with a superior Profitability Score of A.

Segment income statement for the fiscal first quarter of 2024 according to Securities and Exchange Commission filings (seekingalpha.com)

This segment offers a range of products based on a cloud-native approach including connectivity and security functions for (large) campuses, branches, data centre, branch offices and work from home. The smart grid also includes SD-WAN (Software Defined Wide Area Network) products with HPE being a leader in Gartner’s September 2023 Magic Quadrant alongside Fortinet (FTNT), Cisco (CSCO) and Palo Alto (PNWN) with Juniper ranked No. 1. Insight.

So, in addition to gaining market share in everything from campus, data center, enterprise routing or wireless LAN, HPE can expand its capability from the edge to the cloud. Going further, integrating AI into SD-WAN architecture enhances AI networking capabilities, which is key to managing high-traffic and dynamic networks at the edge (periphery).

However, this concept of AI networks has been around for years, but its development should accelerate from the new generation of AI, specifically for inference purposes. Simply put, this is the actual use of LLMs (Large Language Models) by software developers to create AI applications like ChatGPT. This is done after training these models using a lot of domain data. Moreover, unlike the training part which takes place in metro data centers, the inference process is expected to take place at the edge of the network, or in regional data centers and branch offices. This is where the partnership with Nvidia comes in handy, as it supplies HPE with accelerated GPUs for its AI servers. It is worth noting that this is in addition to the opportunities for artificial intelligence in communication.

Speaking of numbers, the company boasted a backlog of $3 billion in AI and HPC products and solutions in the fiscal fourth quarter of 2023 as part of a $180 billion market opportunity.

Consolidation opportunities still exist but revenues are declining

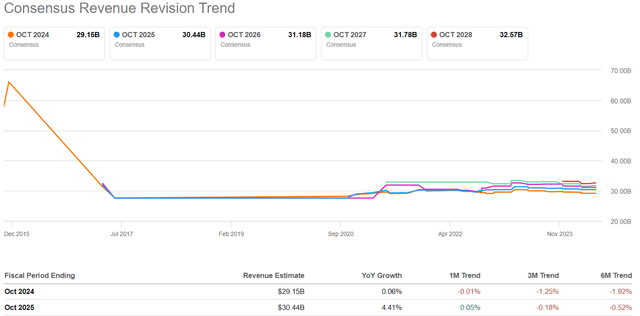

This was the main reason for my bullish stance in January, and was based on combined sales of $36.3 billion for HPE’s 2025 fiscal year ending October next year, which would have represented 18% growth versus 3.6% without the merger. The total consists of adding HPE’s projected sales of $30.63 billion for FY 2025 to Juniper’s $5.5 billion for FY 2025, considering that the merger is expected to be completed by the end of this year or the beginning of 2025. However, since then, Analysts have lowered sales forecasts for both companies. Thus, HPE is expected to receive $30.45 billion for fiscal year 2025 and $5.41 billion for Juniper. This means a total of $35.86 billion, representing a growth of 17.8%.

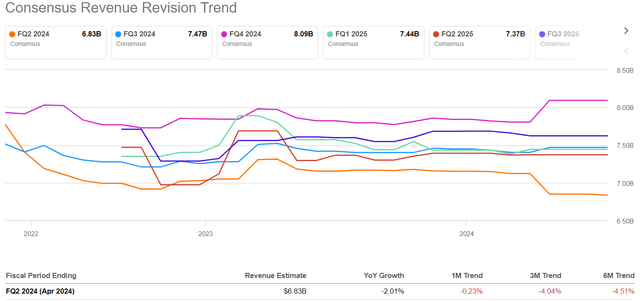

So, if the merger goes through, it would still mean double-digit growth for HPE, but I think it’s important to take the cuts seriously. For this purpose, I look at the current fiscal year, and as seen below, its headline estimate for Q2 2024 was cut from $7.12 billion in March to $6.83 billion in May.

www.seekingalpha.com

Furthermore, the $6.76 billion in revenue generated in the fiscal first quarter of 2024 represented a 13.4% decline year-over-year and a loss of $340 million from what was expected. This was driven by weakness in the server and hybrid cloud segments, both of which suffered year-over-year revenue declines, as shown in the income statement extract above.

Part of the softness is also due to GPU deal times being too long or not getting accelerator chips fast enough to be packed into servers to ship to customers, resulting in a lack of revenue. As for Juniper, its sales declined by 16.1% year-on-year, while exceeding estimates by about $80 million.

Reason for the decline in revenue by looking across the industry

Looking across the industry, it appears that others have not suffered to the same extent. Thus, Cisco, which also has a partnership with Nvidia, suffered a 12.7% revenue decline during its most recently reported quarter, but still managed to beat headline estimates by $70 million, while Fortinet achieved revenue growth and beat (by 10 millions of dollars). . As for Extreme Networks (EXTR), while reported Q4 revenue was down 36.53% year over year, it still managed to beat estimates by $6.40 million.

Moreover, HPE’s estimate of FY24 revenue growth of 0.06% (image below) does not match the 8% IT spending expected to grow in 2024. Therefore, according to Gartner, data center systems and communications services should grow By 10% and 4.3%, respectively.

www.seekingalpha.com

Looking for an explanation for the weakness of networks, it may be related to regulatory approval of the merger.

In this case, the regulatory review process saw the US Department of Justice request additional information from stakeholders. This assumes antitrust concerns and potential risks of competition within the industry. This could also mean that regulators require HPE to dispose of a portion of assets for the deal to go through. Furthermore, the two companies have overlapping products, specifically in the conversion portfolio.

Although the issue may not be as major, this can still create uncertainty in customers’ minds regarding product roadmaps, or whether the product will be supported post-merger and for how long. This was the case when Broadcom (AVGO) acquired VMWare last year. Furthermore, the semiconductor giant’s pricing (licensing) strategy could have incentivized customers to switch from the ESXi product, which is primarily on-premise, to VMware Cloud. This uncertainty led rival Nutanix (NTNX) to launch a promotion that included free deployment and migration services for customers wanting to ditch VMware.

This idea that uncertainty over overlap could benefit competitors including Cisco, Extreme, Fortinet and Palo Alto was also mentioned by Dell’Oro Group, depending on whether they benefit from the situation that typically occurs in the competitive landscape.

Comment while waiting to see during FQ2’24 earnings call

Now, the longer it takes to complete the $14 billion merger, the greater the uncertainty, and the more likely customers will think twice before ordering from HPE or Juniper, especially for long-term projects. As a result, demand could be affected, making it more likely that analysts will revise the headline line down. Alternatively, the company may once again miss key estimates of $6.83 billion because weakness in networks is likely to persist. It also may not live up to its $0.39 EPS forecast if it has to offer discounts to meet sales goals. This could create volatility risk for the stock, just like it did on February 29 when it lost 3% after missing key estimates.

Therefore, it is crucial to evaluate whether the company continues to lose market share in the networking space. In this regard, HPE and Juniper should account for only 9% of the enterprise networking market share after the merger, compared to 43% for Cisco whose AI Ethernet switches could provide about $3 billion in sales opportunities according to my previous thesis. Therefore, HPE faces competition in ultra-intelligent networks as well, and to this end, updating the development of AI backlog is crucial.

To stay within the AI world, an update is needed on the supply of GPUs to equip the HPE ProLiant Gen11, which is compatible with Nvidia’s high-end H100 GPU chipsets. This is an area to watch closely during the upcoming earnings call, as the company’s warehousing business should benefit as well, based on on-demand integration. In the same vein, another item to look out for is HPE GreenLake, or customer pay-as-you-go device purchase plan, which topped $1.4 billion in revenue in the fiscal first quarter of 2024 as it also leveraged AI.

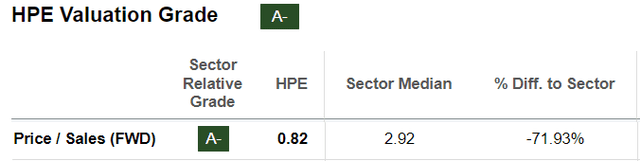

Looking at valuations, HPE remains underpriced based on several metrics including its forward price to sales of 0.82x as it trades at a 72% discount compared to the IT sector. However, it traded at a lower P/E of 0.71x in January and was priced at $17.72.

seekalpha.com

Given revenue estimates of $35.86 billion for the merger instead of $36.3 billion, as I mentioned above, I lowered the January target from $19.8 to $19.56 (35.86/36.3 x 19.8). Now, this represents a 6% upside from the current share price of $18.4, but I have a holding position while I wait to see more. This is especially true in the IT market that is expected to grow faster this year than in 2023, because in such cases, laggards tend to be severely punished by the market.

Finally, M&A needs to be updated, especially if there are any blocking points, but the Juniper portfolio integration will enhance HPE’s edge-to-cloud computing strategy as it provides an improved way for suburban-based software developers to access centralized Gen AI servers.