MesquitaFMS/E+ via Getty Images

I last covered the VanEck High Yield Muni ETF (Bat: HYD) in late 2023. In that article, I argued that HYD’s good tax-advantaged yield made the fund a buy. Since then, the fund has recorded reasonable rates Good returns, superior to many other bond sub-asset classes before Taxes. After-tax returns may appear stronger, although they will clearly differ.

Previous article HYD

Currently, HYD offers investors a tax return of 4.3%. Although the dividend yield itself is lower than most bonds and bond subasset classes, it is a good after-tax yield for most investors, especially those in higher tax brackets. As such, HYD remains an interesting buy and opportunity for investors in taxable accounts, and those facing higher taxes on their income.

HYD – The Basics

- Investment Manager: VanEck.

- Fundamental Indicator: Broad-based ICE rise Yield Crossover Municipal Index.

- Expense ratio: 0.35%.

- Dividend yield: 4.27%.

- Total returns at 10-year CAGR: 2.51%.

HYD – Quick Overview

HYD is a high-yield municipal bond ETF, tracking the ICE Broad High Yield Crossover Municipal Index. SAEED includes all dollar-denominated, tax-exempt municipal bonds in the market, which are subject to a basic set of liquidity, size and maturity criteria.

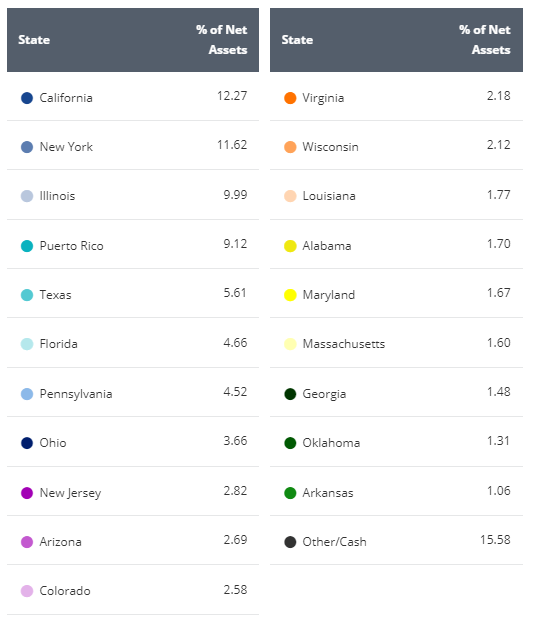

HYD is well diversified across states:

HYD

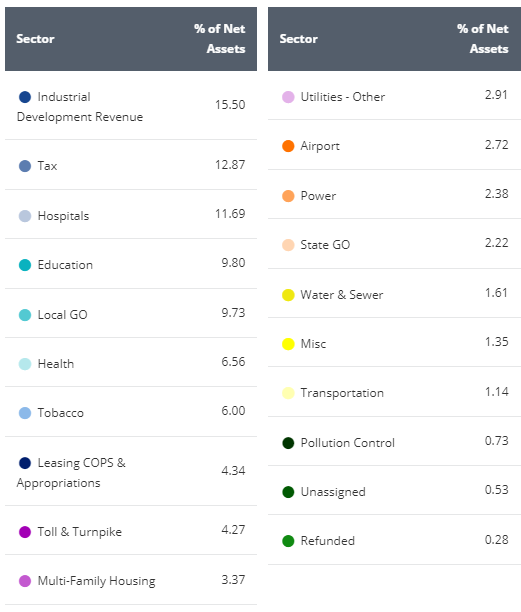

…and across industries:

HYD

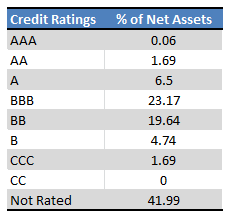

Credit ratings on the fund’s holdings are a mixed bag. Looking at rated bonds, the fund leans towards investment grade, with significant investments in those with BBB ratings. More than 40% of the fund’s portfolio is unrated, and these bonds tend to have below-average credit ratings. In general, credit ratings appear to be evenly split between investment grade and non-investment grade, perhaps leaning toward the latter.

HYD

Notwithstanding the above, the Fund’s actual credit quality is high, as municipal bonds rarely default. Default rates are much lower than those for corporate bonds with similar ratings.

HYD

HYD – Investment Thesis

HYD’s investment thesis is very simple, and is based on the fund’s tax-exempt return of 4.3%. Income from municipal bonds is always free of federal income taxes, which is the case for HYD/its underlying bonds. Tax savings depend on the type of investment account used for investing (401k, personal investment portfolio, etc.), and on the investor’s tax bracket. For some investors, these tax savings will be significant, for others, they are irrelevant.

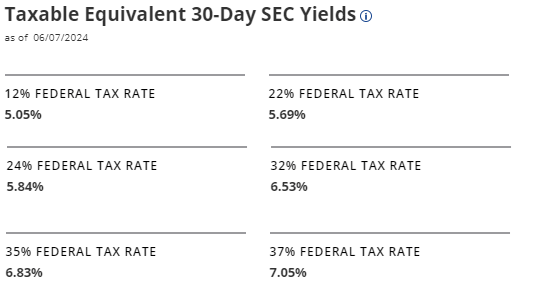

HYD provides us with a simple table of taxable SEC equivalent returns, a standardized measure of the Fund’s underlying income generation, for investors in different tax brackets. These numbers may help us quantify these benefits.

HYD

A quick explanation of the table above.

For investors facing a 12% federal income tax rate, HYD provides equivalent after-tax income as a more traditional, taxable bond fund with a 5.1% yield. For investors facing a 37% federal income tax rate, the number rises to 7.1%.

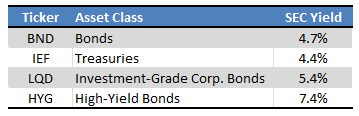

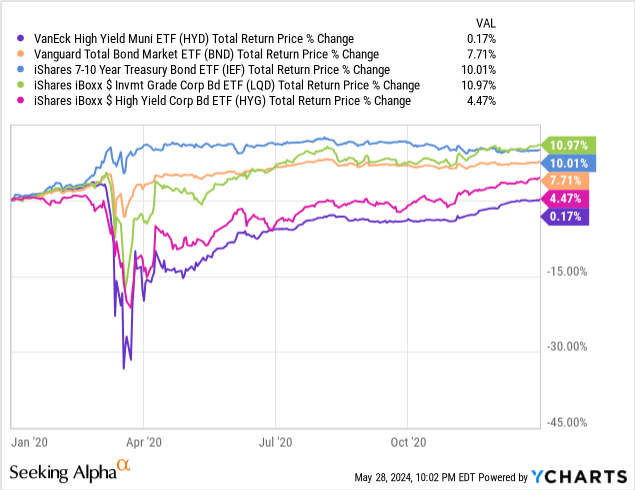

Overall, HYD’s dividends are competitive for investors in middle tax brackets, and higher than average for investors in higher tax brackets. High yield bonds offer higher yields without qualifications, but with much greater credit risk. A quick look at the SEC returns for ETFs representative of the major bond subasset classes.

Fund deposits – table by author

HYD’s tax-advantaged 4.3% yield provides more after-tax income than most bond funds, at least for investors in higher tax brackets. This is a huge benefit, and the fund’s basic investment thesis. The benefit mentioned depends on the circumstances of each specific investor, so some may not find these tax benefits relevant or impactful.

HYD – other considerations

Performance scorecard

The returns of HYD and some of its peers are as follows.

Searching for Alpha – table by author

HYD’s performance record appears to be somewhere between adequate and good.

compared to Most Bonds and Bond Sub-Asset Classes The fund has outperformed since its inception and over the past twelve months. Medium-term performance appears much weaker, partly due to an above-average period of 9.3 years, and partly due to timing issues.

HYD

As is the case with most bonds, long-term returns are very weak, as interest rates have been lower in the past. Yields have improved over the past 12 months, as interest rates have stabilized at a relatively high level. Expected returns also look good, although much will depend on future interest rate policy.

The numbers in the table above are: before taxes, so it does not take into account or take into account the potential tax advantages of the Fund. HYD’s returns may look stronger with that in mind, at least compared to its peers.

Although the HYD’s performance is nothing special, it seems good enough to me. Remember, the most important benefit of a fund is its potential tax advantages, not its total returns. Very poor returns may jeopardize said tax benefits or be too expensive to pay for, but adequate returns are good, in my opinion at least.

Credit risk

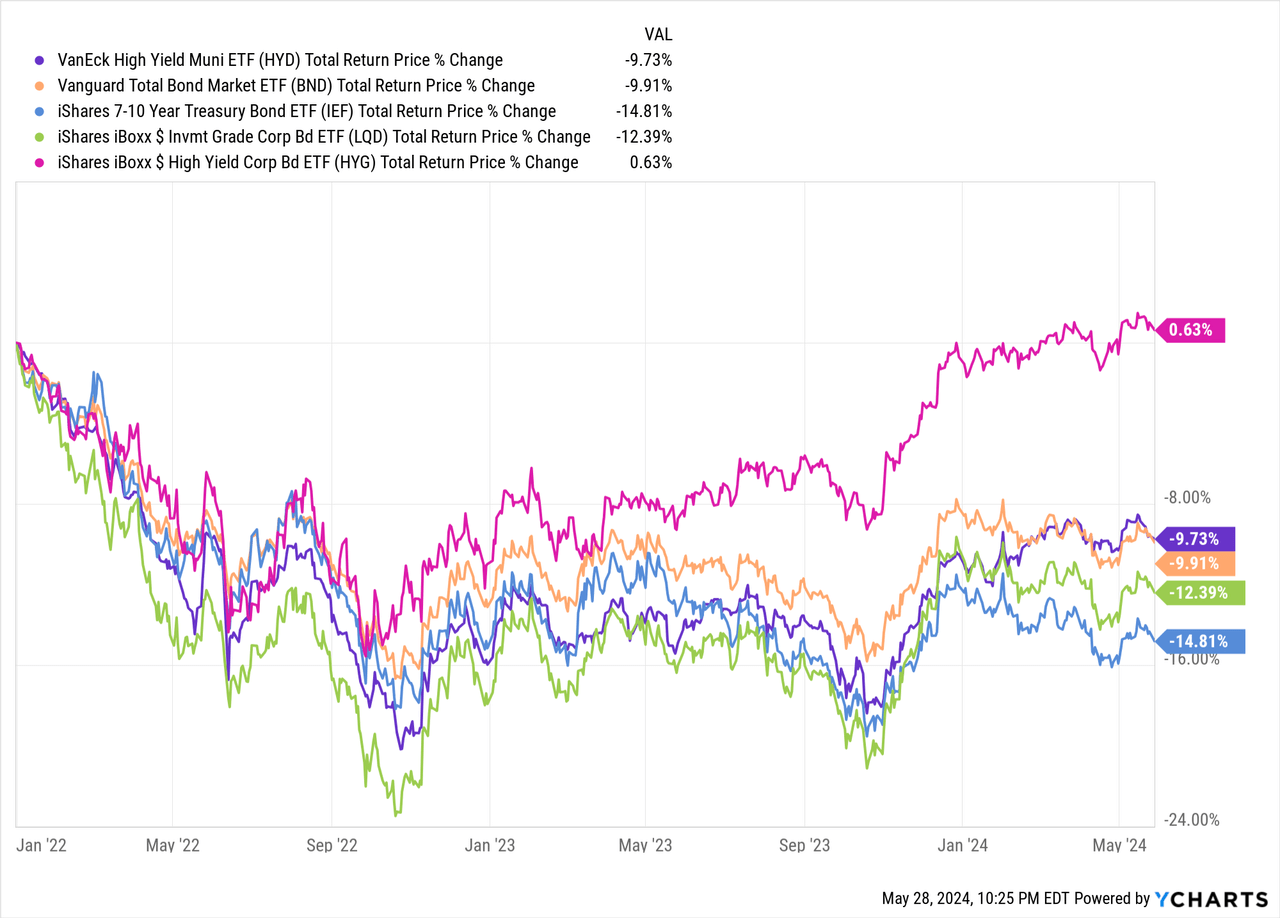

Although HYD’s overall credit quality is reasonably good, the fund experienced above-average losses during early 2020, the start of the coronavirus pandemic and the most recent recession. The losses were higher than expected and continued for a long time.

Data by YCharts

HYD’s above-average losses were at least partly due to its weak credit ratings, despite actual default rates, but only partly. The fund’s performance was lower than that of high-yield corporate bonds as well, which are… definitely More dangerous than HYD.

I’m not really sure why the above happens, but markets sometimes react irrationally, especially in the short term.

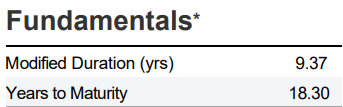

Interest rate risk

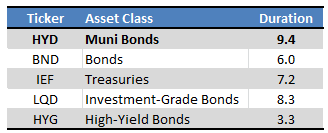

HYD’s interest rate risk is above average, with the fund’s duration being 9.4 years.

Fund deposits – table by author

what mentioned before He should It results in higher than average losses when prices rise. This may no This has been the case during the current walking cycle, where HYD slightly outperformed most bonds instead.

Data by YCharts

As with the fund’s credit risk/quality, I’m not entirely sure why performance differed from expectations. The tax benefits of Muni bonds increase as yields rise, which explains why some Of this, but perhaps not all of it (these issues simply are not all that influential).

It’s also possible that HYD’s slight outperformance was due to higher-than-expected losses during the pandemic: prices simply returned to normal.

However, HYD has below-average credit risk and above-average interest rate risk, although performance has varied somewhat from these characteristics in the past.

Conclusion

HYD is a simple ETF of Muni High Yield Bonds. It provides investors with a taxable dividend yield of 4.3%, which may be of particular interest to investors in taxable accounts facing higher income tax rates. I rate the fund a Buy, although its benefits depend on the specific circumstances of each individual investor.