Moses81

There are many “buffets” out there, and while most are familiar with his saying “Be greedy when others are fearful, and be fearful when others are greedy,” I think his most profound and insightful statement is that “The market is designed to move… Wealth goes from the impatient to the patient.”

That’s because when many growth stocks are trading at what I consider to be nosebleed valuations, I’m happy to buy value stocks at what I consider to be a fraction of what they’re worth.

In fact, I don’t mind stocks remaining undervalued for a long period of time, because it simply gives me the opportunity to dollar-cost average them to grow my income stream.

This brings me to my next two picks, both of which have a long history of lifting Their profits for more than 25 consecutive years. Both trade at attractive valuations for patient investors willing to go against the grain and get paid to wait with above-average returns, so let’s get started!

No. 1: Medtronic

Medtronic (MDT) is a healthcare technology whose products serve the fields of cardiovascular, medical surgery, neuroscience, and diabetes. This includes special devices such as pacemakers, insulin pumps, spinal implants, ventilators, surgical navigation systems, and more.

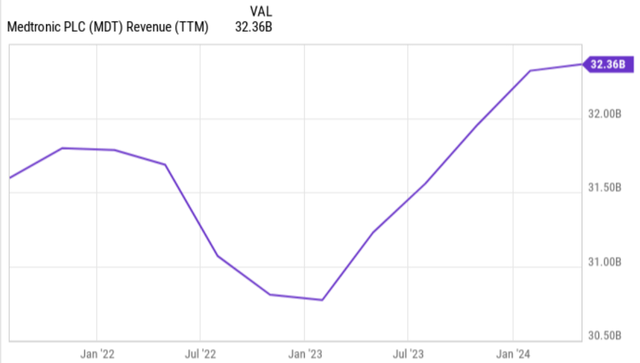

MDT stock continues to trade weakly compared to where it was in the fall of 2021, during which it reached a high of $135. At the current price of $81.37, the stock is down 40% in this time frame. The poor performance of MDT’s share price belies the overall strengths of the business. As seen below, MDT’s revenue has more than recovered from its late 2022 low, with TTM revenue reaching $32.4 billion.

YCharts

MDT continued this growth trend in its fiscal fourth quarter of 2024 (ending April 26), during which organic revenue grew 5.4% to $8.6 billion, beating Wall Street analysts’ expectations by $150 million. Also encouraging is that MDT’s adjusted EPS of $1.46 met the high end of guidance and free cash flow grew 14% year-over-year to $5.2 billion. MDT’s overall growth was supported by mid-single-digit growth in the US and Europe, and by strong 13% growth in emerging markets, including China, where it has since emerged from coronavirus-related lockdowns.

Management is guiding organic revenue growth in the range of 4% to 5% for the current fiscal year 2025. This builds on the expectation that MDT will expand its leadership in key categories, including the introduction of the Aurora EV-ICD, an implantable extravascular defibrillator for the treatment of sudden cardiac arrest, surgical innovations such as the Hugo robotic-assisted surgery system, and the upcoming Simplera sensor integration Sync with MDT’s MiniMed 780G Diabetes System.

Meanwhile, MDT maintains a strong balance sheet with an “A” credit rating from S&P. This includes having a safe net debt to TTM EBITDA ratio of 1.87x, which is well below the 3.0x market generally considered safe for non-REIT/utility companies.

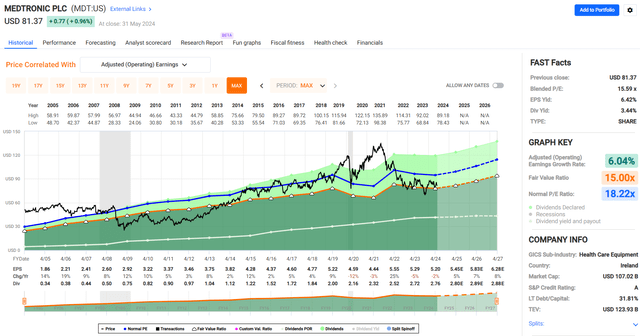

This is supported by MDT’s dividend yield of 3.4%, which comes with a safe payout ratio of 53% and a 5-year dividend CAGR of 6.7%. While MDT is not necessarily cheap at the current price of $81.37 with a forward P/E of 14.9, it sits well below its historical P/E of 18.2, as shown below.

Quick charts

I believe MDT is worth trading at its historical PE level considering its dividend aristocracy status with 46 years of consecutive annual increases under its belt, giving credence to its durability. Moreover, with the encouraging growth mentioned above and analysts forecasting 7% annual EPS growth over the next two years, MDT can deliver reasonable market-wide performance even without a return to its average valuation.

No. 2: Altria

Altria (MO) is officially considered Dividend Aristocrat even though it cut its dividend in 2008, because its spin-off, Philip Morris International (PM) has made shareholders full from a cash flow standpoint with its own dividend, and has increased it every year since. now. then.

Those who follow the tobacco industry likely know that it is currently undergoing its biggest transformation in decades, with smokers enjoying expanded options that include vaping, heat-not-burn bags, and nicotine pouches.

Altria has been somewhat late to the game after its missteps from its failed Juul stake, with peer British American Tobacco (BTI) taking the lead in e-cigarettes, and Philip Morris International taking the lead in heat-based products and not Burn through IQOS and nicotine pouches through Zain.

MO saw a challenging environment as a result of smokers switching to alternatives and illegal e-cigarettes in the US, with revenues net of excise taxes declining 1% year over year during the first quarter of 2024. This was largely driven by a 10% decline On an annual basis. in cigarette volumes, due to the natural decline in smoking, rising gas prices, and the shift to legal and illegal products in the e-cigarette category.

Despite the challenges in the current operating environment, I think it would be a mistake to write off Altria this early in the game as it relates to nicotine transition. This takes into account the encouraging volume growth in MO’s NJOY, which continued to see market share growth increase by 0.6% on a sequential quarter-on-quarter basis to 4.3% at the end of the first quarter. By also promoting MO’s nicotine pouch, On! Market share grew by 0.7% sequentially to 7.1%.

Additionally, MO recently submitted a PMTA to the FDA for NJOY’s raspberry and watermelon flavors with the NJOY ACE 2.0 platform, which has Bluetooth-enabled age restrictions to prevent use among youth. This, combined with crackdowns on illegal vaping, could serve as a tailwind for a company that the market has not fully priced in.

Meanwhile, it’s also worth noting that MO still retains an 8.1% stake in Anheuser-Busch InBev (BUD) as of the end of Q1, which it can continue to monetize for stock buybacks. MO also maintains a strong balance sheet with a BBB credit rating from S&P and a safe net debt to EBITDA ratio of 2.1x. This includes MO taking down $1.1 billion in debt in the first quarter alone.

This supports MO’s dividend yield of 8.5%, which comes with a safe payout ratio of 79% in line with MO’s historical payout ratio of 80%. MO’s earnings are also expected to grow this year, considering that management is guiding for 2% to 4.5% growth in EPS this year.

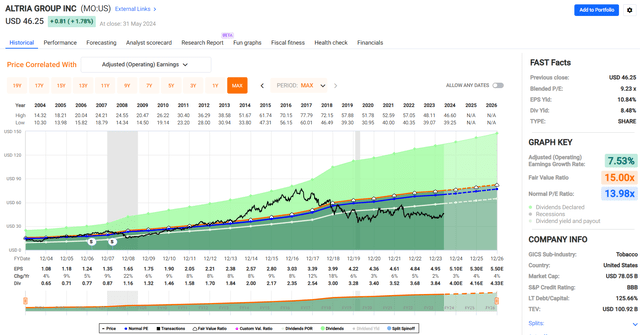

I see value in MO at the current price of $46.25 with a forward P/E of 9.1, which is well below the normal P/E of 14.0, as shown below.

Quick charts

Sell-side analysts who follow the company estimate annual EPS growth of 4-5% over the next two years, which could be driven by price elasticity in traditional smokables combined with growth in newer categories like On! Nicotine Bags, NJOY and Stock Buybacks. As such, MO can deliver above-market total returns when we combine the dividend yield with management’s minimum EPS guidance, and this does not include the potential for the stock price to rise to MO’s long-term historical valuation.

Investor takeaways

Medtronic and Altria offer compelling opportunities for patient investors focused on value stocks with a strong earnings history. Medtronic, a leading healthcare technology company, offers a 3.4% yield supported by 46 years of consecutive annual increases and strong growth prospects in its cardiovascular and diabetes sectors.

Altria, despite recent challenges in the tobacco industry, maintains an 8.5% yield and upside potential from its NJOY vaping business and its strategic investments. Both companies, with their strong balance sheets and commitment to shareholder returns, are well positioned to deliver long-term value through dividends and potential capital raising.