ryasick

I find it interesting that there are ETFs that have a fixed life, designed to mature like bonds without being reinvested to maintain a fixed duration on an ongoing basis. These types of ETFs are attractive because of their liquidity and diversification Through a group of bonds that mature at some point in the future. One ETF that is designed this way is the iShares iBonds 2026 Term High Yield and Income ETF (Bats: IBHF). The IBHF’s primary investment objective is to provide investment results that track an index of US dollar-denominated, high-yield corporate bonds and other income-earning corporate bonds scheduled to mature in 2026. This approach is not only more transparent, but also allows bondholders to manage their price risk. interest efficiently, allowing them to allocate their bond ladder using ETFs rather than individual positions.

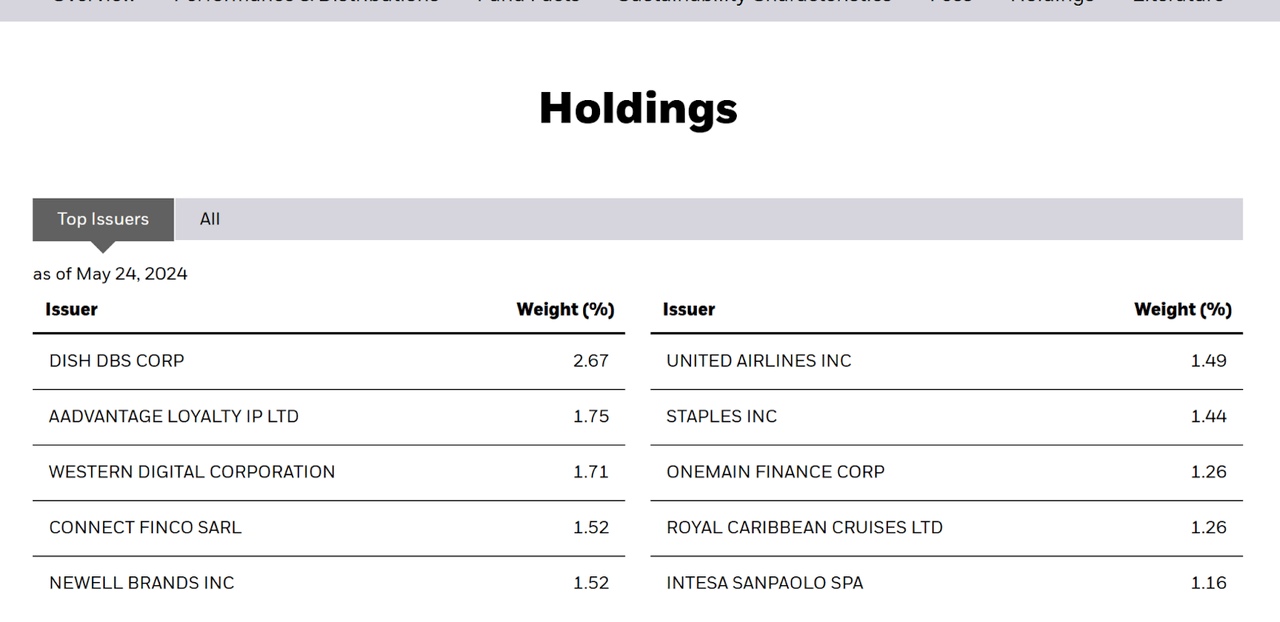

Look at the holding

No position makes up more than 2.67% of the fund, making this a well-diversified fund overall.

iShares.com

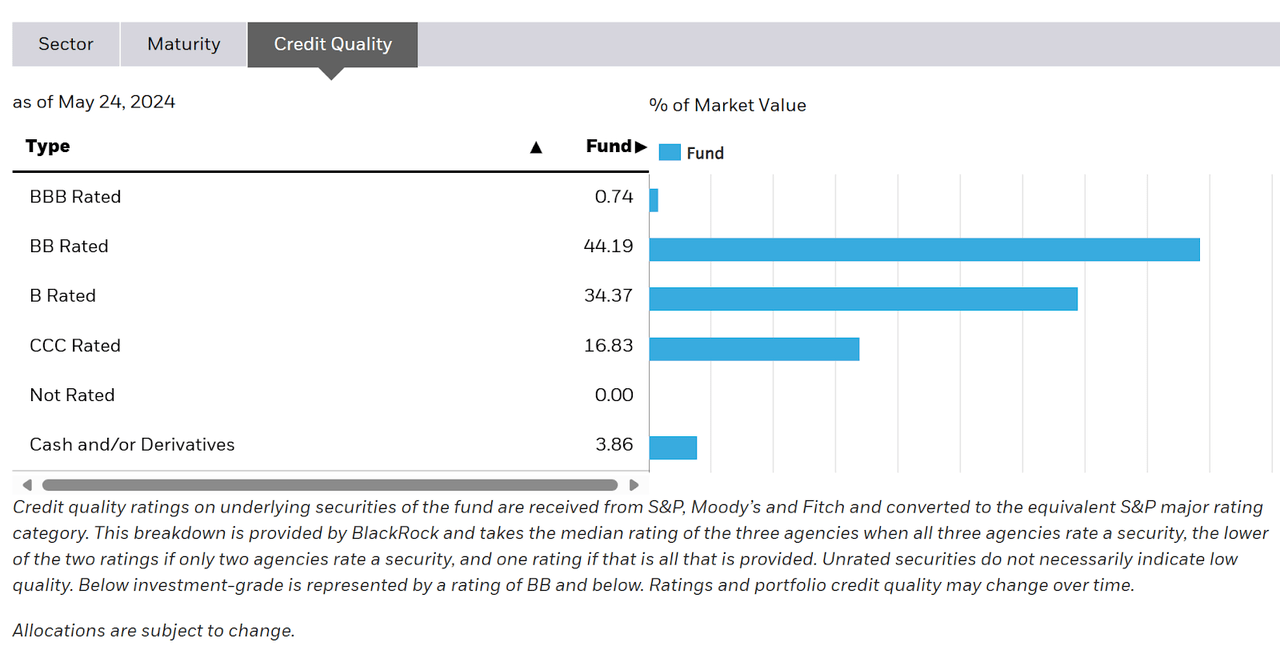

In terms of maturity distribution, the bulk matures in the range of one to two years. Again – this is a bond fund that will mature, so don’t expect to hold it for years. This may be an advantage, especially at this stage of the cycle. Note that credit quality is generally on the riskier side. It makes more sense for me to consider a term bond ETF like this rather than a continuing junk debt fund given the default risk, which can rise for issuers if there are concerns about refinancing risks on new, revolving debt.

iShares.com

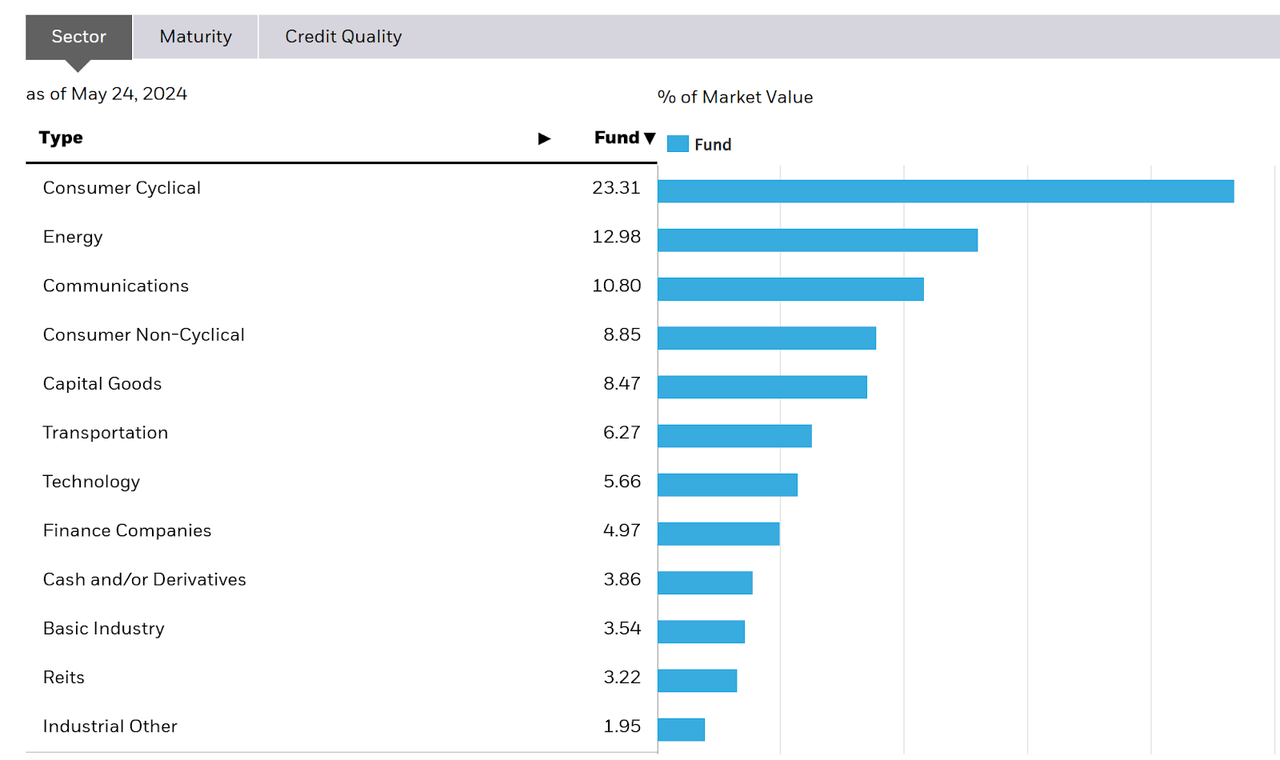

Sector collapse

As for the division of the sector, there is nothing surprising here given the quality of credit that the fund targets. The largest allocation goes to consumer cyclical supplies at 23.31%, followed by energy at 12.98% and communications at 10.80%. The sector composition is interesting here. If you expect a yield curve inversion (the longest in history) to be a recession warning, you should worry about exposure to consumer cyclical debt issuances. However, since this does not mean rolling over debt to maintain an ongoing duration/position, a fund like this may actually hold up just fine as bonds are “pulled down” as long as recession defaults are minimal for these companies .

iShares.com

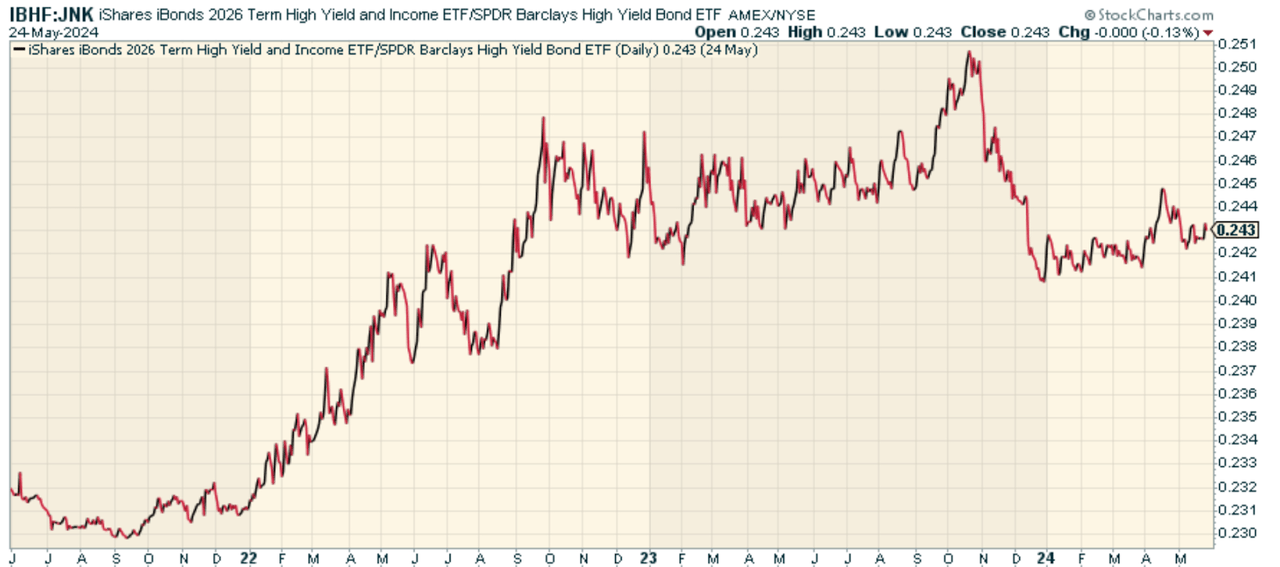

Peer comparison

It’s really hard to make a good comparison between this fund and another fund that will also mature later, so it might be worth considering how it fares against the SPDR Bloomberg High Yield Bond ETF (JNK) to see how it performs against a fund that doesn’t have a specific maturity date. When we look at the IBHF to JNK price ratio, it has outperformed. Again, this makes sense because there is really no reinvestment risk given the specific lifespan of IBHF relative to JNK.

StockCharts.com

Weigh the pros and cons

On the positive side, the fund offers a new way to serve high-yield bond investors through a defined maturity structure and guaranteed income distributions on a regular basis. This makes IBHF attractive for building a bond ladder or deploying a more sophisticated interest rate risk management strategy. IBHF’s portfolio is also highly diversified, reducing concentration risk and providing exposure to a wide range of high-yield bond issuers. The fund provides transparency and tradability for a specified period.

But again, high-yield bonds are riskier than corporate bonds that don’t offer the same big dividends. There is significant credit risk here in the event of disruption in bond markets due to repricing of default risk. And remember, IBHF’s maturity structure means it will convert to cash and cash equivalents at the end of its target maturity period in 2026.

Conclusion

I think this type of money is interesting. You know that the ETF will not reinvest its holdings, and has a set period after which it will stop trading and convert to cash. And with a 30-day SEC yield of 7.54%, I’ve got a nice income that, while it won’t last forever, looks fairly solid right now. However, I still find this part of the market to be broadly risky, although I think the specific maturity profile helps a lot. If the risk of default is high, in my view it is better to know that the bonds you hold are close to the face value of the payment, and the ETF wrapper in this case provides comfort in that.

Expect crashes, corrections and bear markets

Expect crashes, corrections and bear markets

Are you tired of being a passive investor and ready to take control of your financial future? Introducing the Lead-Lag Report, an award-winning research tool designed to give you a competitive advantage.

The Lead-Lag Report is your daily resource for identifying risk drivers, uncovering high-return ideas, and getting valuable macro feedback. Stay ahead of the game with important insights into leaders, laggards, and everything in between.

Move from risk-taking to risk-averse with ease and confidence. Subscribe to the Lead Lag Report today.

Click here to access and try the Lead-Lag report free for 14 days.