JHVEphoto

After the previous quarter, we cautioned investors not to buy into the hype around artificial intelligence International Computer Foundation (New York Stock Exchange: IBM). The tech giant has long had a leading artificial intelligence, or AI, product in Watson without producing it Any meaningful income. My investment thesis remains neutral on stock after stock Weak quarter And all indications are that the company is not really investing in AI opportunities.

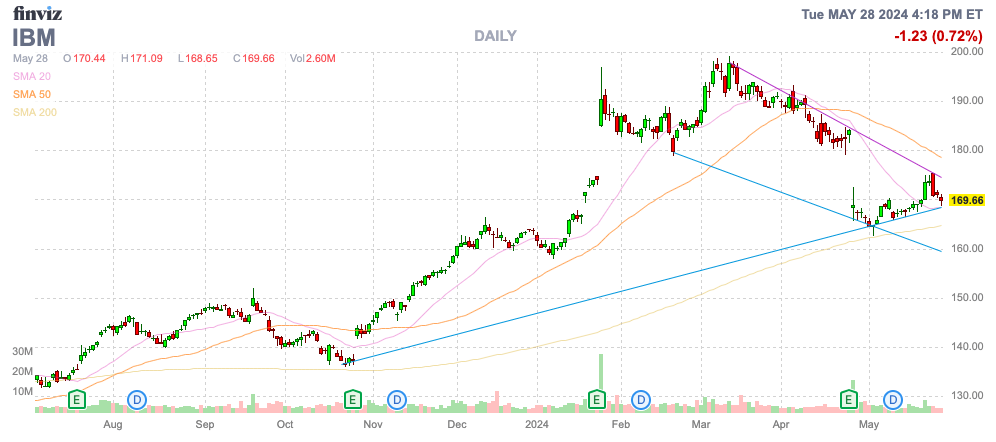

Source: Finviz

Noise ally

IBM makes a lot of headline-grabbing announcements regarding artificial intelligence, but the tech giant isn’t actually doing much to generate sales. Since the beginning of May, IBM has made the following deal announcements:

- May 21 – IBM expands its Watsonx portfolio to extend AI into Amazon Web Services.

- May 15 – Palo Alto Networks and IBM announced a partnership to bring AI-powered security offerings to customers

- May 9 – IBM launches new Microsoft software Co-pilot capabilities amid artificial intelligence drive

- May 8 – ServiceNow partners with IBM and Microsoft to integrate GenAI capabilities

- May 8 – IBM and SAP expand collaboration to build next-generation AI capabilities

Every week, IBM establishes some partnership or collaboration with a major technology company to develop AI products. The problem is that the company announced similar deals in the first quarter, and AI-related revenues aren’t moving the needle.

In late April, IBM announced these numbers for the first quarter of 2024:

- Q1 non-GAAP EPS of $1.68 beats $0.09.

- Revenue of $14.5 billion (+1.5% YoY) misses by $80 million.

The company is guided only by mid-single-digit revenue growth for the year. IBM has revenues of more than $60 billion, but the AI-related software category represents only a small portion of the business.

Red Hat’s cloud business is a prime example of the difficulties the technology company faces. Cloud services are booming, with… Microsoft (MSFT) and Google (GOOG) reports growth rates of 20% to 30%, but Red Hat’s smaller business only grew 9%.

GenAI’s business is still relatively small with backlog only in the $1 billion range per CEO Arvind Krishna on the 1Q24 earnings call:

Underneath that is our GenAI book of business, which is off to a very good start overall. It’s been three quarters since we announced our GenAI technology stack, Watsonx, last July. We’ve now surpassed $1 billion in overall business.

The company reported GenAI backlog in the $500 million range after the fourth quarter. The backlog is growing rapidly, but the amounts are much too small to move the needle and are largely related to the consulting business with a book-to-invoice growth rate of 1.15, but very little sales growth of 2% last quarter. Additionally, IBM is not providing many details on the timeline for this backlog, as the extended contract period could indicate a much smaller increase in annual revenue.

The main software segment achieved revenue growth of 6%, with annual revenue reaching nearly $14 billion with growth of 8%. IBM is still tied for just 25% recurring revenue due to its consulting and infrastructure business collecting $8.3 billion last quarter, while its quarterly ARR is only in the $3.5 billion quarterly range.

At a price that’s right for the AI boom

IBM traded at just $125 last year. The stock fell back to $170, but IBM reached a high of nearly $200 due to the AI boom.

Consensus analyst EPS targets don’t expect earnings growth to reach 5% until 2025. Investors need to realize that IBM missed revenue targets last quarter by $80 million, suggesting estimates may be too aggressive.

Source: Searching for Alpha

The stock still trades at 16 times 2025 EPS targets, yet AI is expected to deliver limited additional growth. IBM actually trades at 3x its expected earnings growth rate, while 2x is considered expensive.

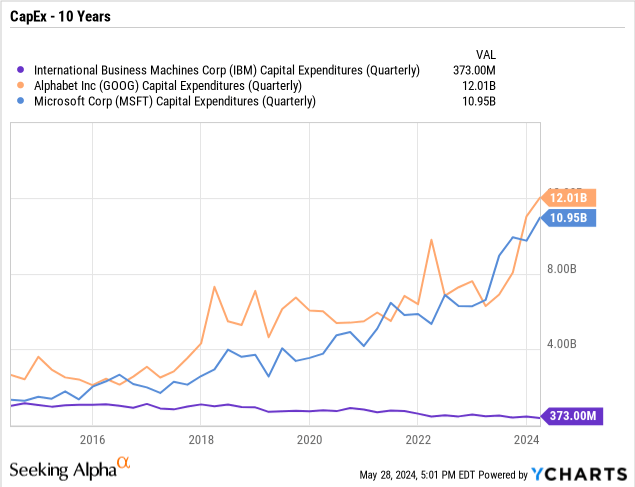

IBM is expected to generate $12 billion in free cash flow this year, partly due to a lack of new investment. Net new capital expenditures during the first quarter were just $0.4 billion, down $0.1 billion from last quarter.

With the massive AI opportunity, IBM should invest aggressively in Red Hat’s new Watsonx AI products and data center functions, and the company is instead cutting back on capital expenditures.

More than 10 years ago, IBM spent similar amounts on capital expenditures as Google and Microsoft, and now the two tech giants spend 25 times as much as IBM, and the stock is worth at least 15 times more. Google and Microsoft each spent more than $10 billion in quarterly capital expenditures last quarter, while IBM continues to cut spending in the face of the massive opportunity.

Under the best-case scenario, where IBM accelerates growth, the stock is already priced in for the AI boom. Under the likely scenario in which IBM never achieves 5% annual growth due in part to a lack of investment, the stock weakens and would likely fall back to the previous $125 range.

He stays away

The main take away from investors is that IBM has no logical reason to go higher from here. The stock will likely fall, suggesting that a Neutral rating is likely too aggressive, even as AI hype supports much of the stock’s valuations.

IBM has every reason to invest heavily in AI, yet the company remains flat. In this regard alone, an investor should avoid IBM stock.