Focusert/iStock via Getty Images

thesis

We’ve covered a number of CLO funds, with the latest articles mentioning the largest funds in the space, the Janus Henderson AAA CLO ETF (JAAA) and the BlackRock AAA CLO ETF (CLOA).).

In today’s article, we’ll review Invesco’s offering in this space, namely the Invesco Aaa CLO Floating Rate Note ETF (Bat: Iklo), which currently pays an attractive 6.7% yield over 30 days on the stock. Please note that the fund name is a play on Invesco (‘I’) and CLOs (‘CLO’), and should not be confused with VanEck CLO ETF (CLOI).

The article will cover the fund’s composition, historical performance, risk factors, and analyses, and highlight why it is an attractive investment in today’s high-rate environment.

Collateral composition – contains AA CLO tranches

Unlike its counterparts, ICLO contains… Small sleeve of AA rated chips:

Collectibles (Fund website)

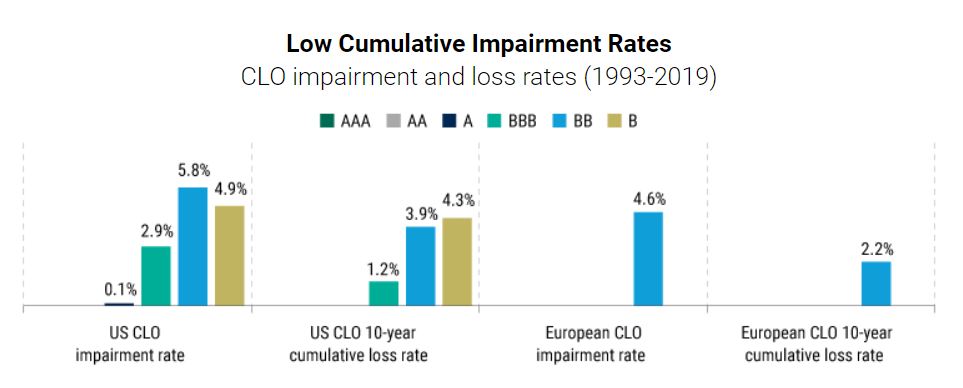

Currently, AAA CLOs make up 86% of the fund, followed by AA names at 13.7% of holdings. Despite the small AA range, please keep in mind that there are no historical losses for collateralized loan obligations rated AA:

Default prices (Pine Bridge)

The only investment grade tranches with CLO losses are represented by BBB names (green bar in the chart above) at 2.9%, and A tranches at 0.1%. Therefore, from a hypothetical prospect perspective, ICLO represents a strong option.

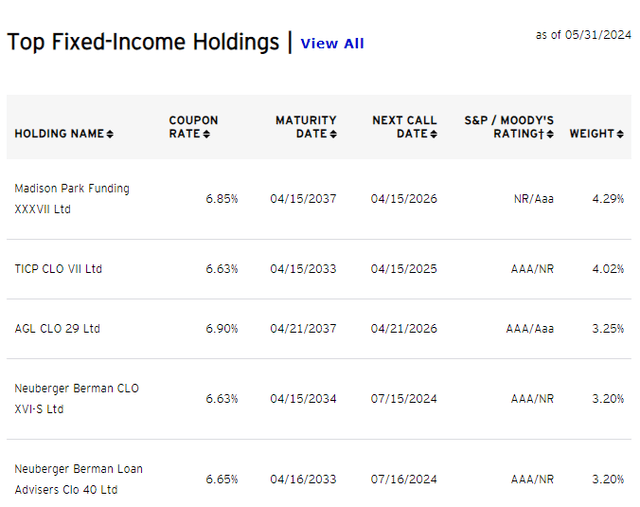

None of the individual CLO tranches constitute more than 5% of the fund:

Collectibles (Fund website)

While this aspect is less important for CLOs due to the diversification inherent in all CLOs, we nevertheless do not want to see concentrations of a single manager. Madison Park Funding XXXVII represents 4.29% of the holdings, followed by TICP CLO VII at 4.02%.

We will see a significant difference between AAA CLOs only in the scenario where there is a severe economic downturn and there are significant corporate defaults. In such a scenario, there will be names that are managed by good asset managers and will be able to navigate such a scenario with a high level of dependency, and certain names from weaker managers that will trade more widely due to lower loss mitigators.

Excel in a high-rate environment

Not all AAA assets are made the same. While Treasuries have suffered in the past few years on the back of rising interest rates, AAA collateralized loan obligations have boomed. Although ICLO has a weighted average life of 3.9 years (‘WAL’), its duration is almost zero. WAL indicates the average time that the underlying collateral will be outstanding, focusing solely on repayment of the loan principal. Since ICLO is based on floating rate assets, it has a low duration and is therefore able to offer higher rates.

Moreover, since CLOs fall within the securitized asset class, they need to yield more than Treasuries to entice buyers. The fund’s spread over SOFR is currently 142 basis points, and generally, AAA CLOs will yield over 100 basis points over SOFR (historically). There will always be a spread since the asset class is not simple, and one needs to understand the structural elements in order to feel comfortable when investing.

The openness of the ETF market to CLOs was unexpected, as traditional buyers were insurance companies outside Japan, as well as regular buyers in the United States. We expect further growth here, and ICLO will be one of the beneficiaries.

The fund will remain on offer until the Fed starts lowering interest rates, but until then, it will see a decline in yield rather than price. Unless we experience a severe recession, expect rates to remain very tight, while the fund will end up passing lower interest rates through dividends when the Fed ends up reducing Fed funds. In a negative recessionary environment, we would have a widening of the credit spread, which would put pressure on the name, but judging from the performance of the peer fund, we should only expect a price decline of -2%.

Historic performance

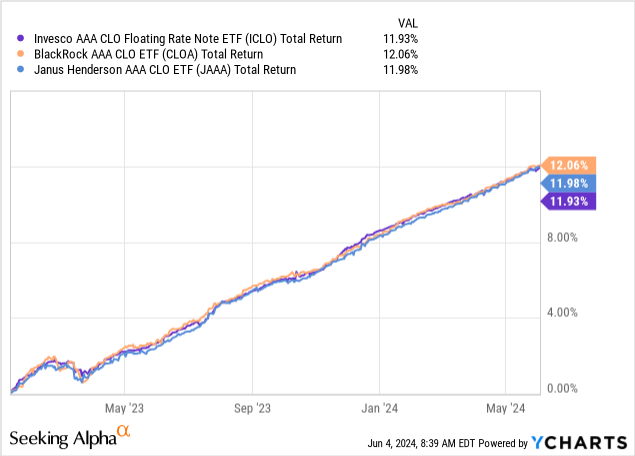

Since the start of 2023, ICLO has shown performance in line with CLOA and JAAA:

This tells us that Invesco is doing a good job of picking up good names in the AAA space. As a reminder, AAA CLOs are not fungible, but due to their seniority in structure, they tend to perform in parallel during expansions or scale markets. If we experience a hard decline or recession, we will have a split in performance between better and weaker names.

ICLO Analytics

- Assets under management: $0.12 billion

- Sharpe Ratio: NA (1Y)

- Sexually transmitted diseases. Deviation: 0.69(1Y)

- Yield: 6.7% (30 days per second)

- Leverage ratio: 0%

- Configuration: Fixed Income – AAA CLO

- Duration: 0.08 years

- Expense ratio: 0.27%

Which ETFs should you choose?

As we can see from the analysis above, ICLO, JAAA, and CLOA have very similar total returns in the past year and, more importantly, very similar downside risks. Right now, JAAA outperforms the competition with a volume of roughly $10 billion, while investors who like some asset management platforms like Invesco can opt for ICLO. There is value to be gained through allocation, with names like Invesco able to benefit from desirable releases from certain asset managers.

However, at the end of the day, for the retail investor who does not trade volume, the three names can be used interchangeably. Institutional investors who might be looking to trade $50 million within a single day will frequently choose JAAA, while retail should be neutral between the three names.

Conclusion

ICLO is a fixed income ETF. The vehicle invests in AAA CLOs, but also has a small 13% holding of AA names. The fund has delivered outstanding performance since the start of 2023, posting gains of 12% in a rising interest rate environment. Although the WAL period is 3.9 years, the fund has almost zero duration, representing a convenient way to pass on higher rates to investors. The current yield for the 30-day ETF is 6.7% paid monthly. The fund leverages the Invesco name and platform and represents a suitable fund to own in the current macro environment.