com. tupungato

My last article about Intel (NASDAQ:INTEC) in October 2022, and was trading at about $25 per share at the time. I was bullish on Intel when I wrote this article, and in about 13 months, the stock price has soared It nearly doubled in value, trading at around $50 in December 2023. However, things changed, and the stock returned to around $30 per share. Once again, I think this is a good time to buy Intel shares, which is what I have been doing lately. I know many investors are bullish on Intel and can point to a number of reasons why, including relatively poor performance compared to NVIDIA (NVDA). However, this is looking in the rearview mirror, and I’m mostly interested in how Intel stock performs To move forward. One thing is for sure, expectations from Intel seem very low, and expectations from NVIDIA seem very high. This is often a great setup for shares of a low-expectation company to actually outperform. With that in mind, let’s take a closer look at Intel:

The elephant in the room

A potentially big problem for Taiwan is of course China, which has made clear that it wants reunification one way or another. A recent Newsweek article sums up the situation and states:

The People’s Republic of China claims Taiwan as its territory, although it has never ruled there. Xi said unification is inevitable, through force if necessary. US officials believe he has directed his forces to be able to invade by 2027. However, this does not necessarily mean that this or any other year was chosen for the mission.

We saw some supply chain issues when Ukraine was invaded, but this type of disruption in Taiwan will have a much greater impact. Taiwan produces an estimated 60% of the world’s chips and about 90% of the world’s advanced chips, so disruption to these supplies would impact the global economy. As tensions rise between China and Taiwan, this appears to be causing great concern for some Taiwan Semiconductor (TSM) customers. In a recent article, this concern was confirmed as some customers wanted TSM to move its factories out of Taiwan; It states:

The Taiwanese semiconductor maker has indicated that it has held discussions with some customers about moving its chip facilities from the island nation amid escalating tensions with China, however, such action would be impossible, Reuters reported.

“Instability across the Taiwan Strait is indeed a consideration for the supply chain, but I want to say that we certainly don’t want wars to break out,” CC Wei, chairman and CEO of TSM, told reporters following the company’s annual general meeting where they were elected unanimously. . “

Intel is the “home team”

Being an American company and not just a chip designer but also a manufacturer and a company that makes chips for other companies, Intel has a lot to offer. When you see companies being so concerned about potential supply chain disruptions that they wonder if Taiwan Semiconductor could exit Taiwan, this seems to indicate that they might want a backup plan, which could give Intel some of their business. like that.

It is a big business risk when you are supplied from only one source. If anything happens to this resource, your company could be greatly affected. This is why it stands to reason that even if you prefer one product supplier over another, you may want to hedge and source at least some products from a second supplier. For this reason alone, it makes sense for the company not to rely too heavily on just one chipmaker, such as Taiwan Semiconductor Corporation, but to hedge and source supplies from Intel as well.

Intel could have an advantage in terms of pricing, internal transportation and catching up with new AI chips

Whether you’re a chip designer like Nvidia, or an end user who needs to buy chips to manufacture specific products, it makes sense to do at least some business with Intel. Taiwan represents a major geopolitical and potential supply chain risk, meaning engaging with Intel is a smart hedge against these risks.

Another reason Intel might win is because of the very competitive pricing and advanced chipsets like the Gaudi 3. One recent article points out the performance and pricing advantages that the Gaudi 2 and Gaudi 3 have over Nvidia’s H100, and states:

Second, Intel announced attractive pricing for system providers, an unusual move aimed at highlighting the value proposition of its Gaudi chips. An AI kit containing eight last-generation Gaudi 2 AI chips and a universal baseboard will cost system providers $65,000, while a version with eight Gaudi 3 AI chips will cost $125,000. Intel estimates that the prices of this equipment are one-third and two-thirds the cost, respectively, of comparable competitive platforms.

While Intel undercuts Nvidia’s price, the company expects its chips to deliver impressive performance numbers. The company estimates that an array of 8,192 Gaudi 3 chips can train an AI model up to 40% faster than an array containing the same number of Nvidia H100 chips.

Intel recently introduced the Xeon 6 chip, an advanced processor ideal for artificial intelligence applications. I think this is another sign that Intel is serious about catching up in the AI market.

Humanoid robots

There’s a lot of interest in AI these days, but I’m thinking two to four years from now is when I think we could see AI converging with hardware, creating the starting point for mainstream adoption of humanoid robots. This seems like a truly massive opportunity, especially since many of the tech leaders and tech billionaires who are leading the way in terms of AI now seem to see a huge opportunity in humanoid robots. Humanoid robots will require a lot of chips and a variety of them, from basic to advanced. Intel could benefit greatly from the potential growth of this emerging industry.

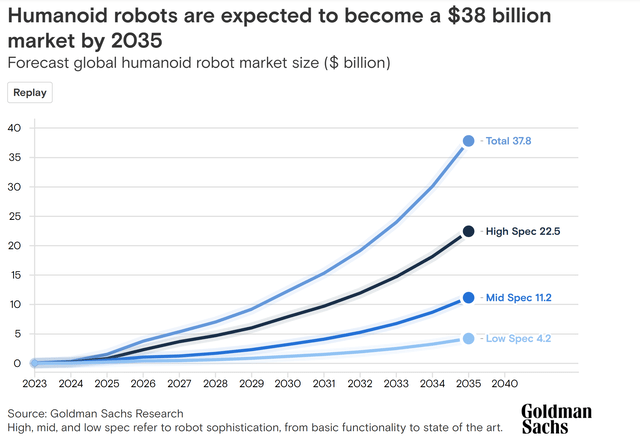

Apple (AAPL) is reportedly looking into developing personal robots. Tesla is developing the humanoid Optimus robot, which Elon Musk said could be larger than any other product Tesla makes now. Elon Musk also said that Tesla may be ready to start selling robots in 2025. Another humanoid robot company, Figer AI, has received funding from Amazon’s Jeff Bezos (AMZN), as well as Nvidia’s Jensen Huang. Analysts at Goldman Sachs (GS) predict that humanoid robots will be worth $38 billion by 2035, as shown below:

Goldman Sachs

Sentiment and market share can change quickly with technology and chip stocks

Sentiment and market share can turn in a very short time, and of course, we have seen many chip stocks rise and fall. Years ago, I wrote an article about Advanced Micro Devices (AMD) when it was trading for about $3 per share. At the time, many investors thought AMD would end badly, but it turned out to be a great buying opportunity. In 2016, Nvidia shares traded for only about $7, and today they trade for about $1,200 per share. This shows that investors have a history of underestimating the potential of chip stocks.

It’s important to keep in mind that almost every major technology stock went through a period where investors were very passive and felt that growth was over and that these companies would never regain that ground again. This happened with Microsoft (MSFT) under Steve Ballmer, it also happened with Apple (AAPL) in the past, and it also happened with Meta Platforms (META), when that stock fell below $100 per share less than two years ago due to growth concerns. Now it is trading at around $500.

Chart

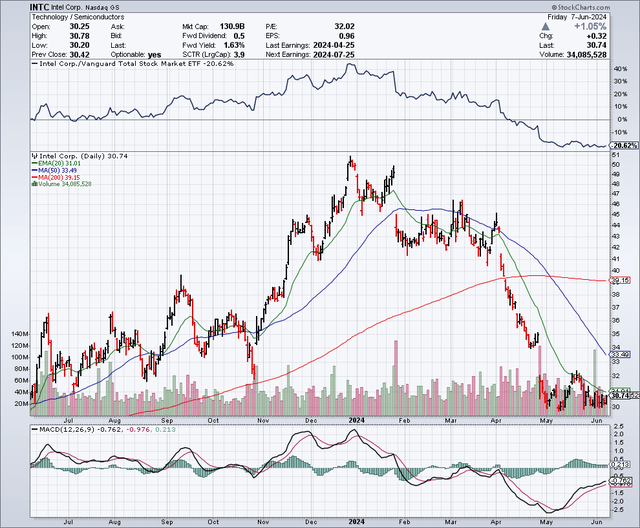

As the chart below shows, Intel shares were trading at around $50 in December 2023, but in the past few months that stock has roughly halved. Intel shares are now trading below the 50-day moving average of $33.98 and the 200-day moving average of about $39.18.

StockCharts.com

Earnings estimates and balance sheets

This year, the bar seems to be fairly low for Intel. Analysts expect Intel to earn $1.10 per share in 2024, on revenue of $55.84 billion. However, growth investors should be happy to see earnings estimates nearly double to $1.98 per share in 2025, with revenue reaching $62.63 billion. Earnings are expected to jump again in 2026, with estimates at $2.57 per share, on revenue of $68.58 billion. Investors seem to be fixated on lackluster 2024 earnings estimates, but I see reason for optimism when considering how much earnings are expected to grow in 2025 and beyond.

As for the balance sheet, Intel has about $52.45 billion in debt and $21.31 billion in cash.

Potential downside risks

Intel has clearly dropped the ball in the past by allowing previously much smaller companies to emerge from behind and gain huge levels of market share in terms of advanced chips. But she seems to have acknowledged this and the need to get back on track. I think Intel has a solid plan to not only stay viable, but to reclaim the throne at least to some extent in the future, but obviously this will take some time. However, competition from Nvidia will remain fierce and may pose ongoing downside risks for Intel. Clearly, management execution represents a potential downside risk, as do macro issues such as a potential recession. Tariffs and chip bans represent another potential downside risk as tensions rise between China and the United States

In summary

Sentiment towards Intel appears to be very negative, which is not uncommon when the stock is trading at or near its 52-week lows. But this is when it gets interesting for value and contrarian investors. I see reasons to be skeptical about Intel, but I’ve also seen the same kind of negativity and skepticism with other stocks that turn out to be buying opportunities. I don’t have a large position in Intel, but I will add more about more vulnerability and give this company time to take advantage of all the tailwinds it could have in the coming years, from PC cycle modernization, to artificial intelligence, to humanoid robots. Intel is also in a unique position as the “home team” where it can serve as a hedge and a key supply chain partner for many technology companies, especially in the event of disruptions in Taiwan.

Again, sentiment can change quickly in the technology sector, especially regarding chip stocks. For example, just remember that Intel stock was worth $50 for the past 52 weeks, and I think as sentiment becomes more positive, it will rise to $50 and more in the coming years.