J Studios/DigitalVision via Getty Images

Intel finally has you covered (NASDAQ:INTEC) in January; I placed a sell rating at the time, and since then, the stock price has fallen approximately 35%. Now, I think the company’s value is fair, which prompted a review My review of Intel to hold. I think the bulk of the selling, which was justified by lower earnings, is now over. Therefore, Intel’s near-term future is starting to look brighter, and there could be significant growth over the next few years to benefit from. However, I remain skeptical about how much reliable growth the company can achieve over 10+ years, given that it is already a large company that has not had very competitive growth over the past decade in either its top or bottom line.

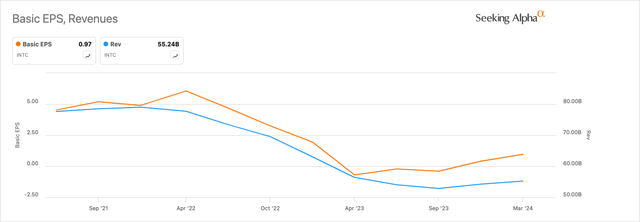

Profits and price deflation

Intel has seen a significant decline in profits and revenues over the past few years:

Author, using Seeking Alpha

This was primarily a result of these reasons:

- Intel has faced assembly bottlenecks at the chip level, restricting its ability to meet demand, especially for its AI-focused Core Ultra processors.

- The company struggled to bring five processing points to the market within four years, resulting in significant start-up costs. Intel’s Foundry Services unit has seen declining revenues, and that unit has high costs to increase capacity to allow it to compete in the foundry market.

- Intel is facing stiff competition from more modern companies like Nvidia (NVDA) and Advanced Micro Devices (AMD). Intel’s new launches, such as 5th generation Intel Xeon processors and Gaudi 3 AI accelerators, have not significantly increased revenue yet.

- Market saturation, competitive pressures and delays in technology adoption have caused declines in core sectors such as networking, edge, data center and artificial intelligence.

- There are macroeconomic challenges at the moment, including stagnant growth, rising interest rates, and geopolitical turmoil contributing to supply chains and market demand.

According to Seeking Alpha data, the analyst consensus expects Intel’s EPS to contract by three quarters, with a significant recovery starting in the first quarter of 2025. Personally, I think the situation could improve soon. Intel is focusing on pushing AI-powered PCs this year, with expectations of selling 40 million AI-powered PCs by the end of 2024. Also, now that Intel Foundry Services is more advanced, it should be able to start experimenting with Gradual profitability benefits from the project. By late 2024 at the latest, the company’s long-term strategy of building on AI solutions and expanding its manufacturing solutions should begin to pay off significantly. The Foundry Services segment actually showed a 63% increase in revenue last quarter, so the positive momentum is definitely building.

Competitive challenges ahead in the long term

Intel faces significant long-term challenges from three major competitors, in my opinion:

| AMD (Advanced Micro Instruments) | AMD is known for its high-performance computing products, including CPUs and graphics processing units |

| Nvidia | Nvidia specializes in graphics processing units and artificial intelligence computing. Nvidia is also a leader in hardware and software solutions for AI. |

| TSMC (Taiwan Semiconductor Manufacturing Company) (TSM) | TSMC is the world’s largest semiconductor foundry. It manufactures chips for major clients such as Apple, AMD and Nvidia. |

Intel has noticeably struggled to keep up with rapid innovations in semiconductor manufacturing. The company faces perhaps the most significant threat from TSMC because it is almost impossible to outperform the Taiwanese company. Instead, I think Intel will have to dig a ditch for itself, which is relatively convenient. It is unlikely to be the leader in advanced production. Alternatively, they may find themselves used in niche and legacy technologies, custom and integrated solutions, foundry services for select markets, advanced packaging technologies, and artificial intelligence and machine learning solutions. This is not necessarily a bad thing for Intel shareholders; This just means that investors in the company should prepare for slower, more moderate growth than Nvidia or TSMC.

| you are K | NVDA | AMD | TSMC | |

| 5-year average FWD revenue growth | -1.18% | 28.4% | 26.22% | 15.19% |

| FWD EPS Growth Diluted 5-Year Average | -8.59% | 34.38% | 47.84% | 15.78% |

| FWD 5Y Free Cash Flow Growth Average | -8.51% | 40.79% | 75.94% | 14.88% |

| TTM Net Income Margin 5Y Average | 19.95% | 29.22% | 11.08% | 38.48% |

| The ratio of equity to assets | 0.55 | 0.64 | 0.83 | 0.63 |

| P/E ratio (FWD) according to GAAP | Done = 32; FWD = meaningless | 47.5 | 115 | 26 |

| Front-end price-to-earnings (P/S) ratio | 2.5 | 24.75 | 10.5 | 8.5 |

For numerical data, key strengths are in bold, and key weaknesses are in italics.

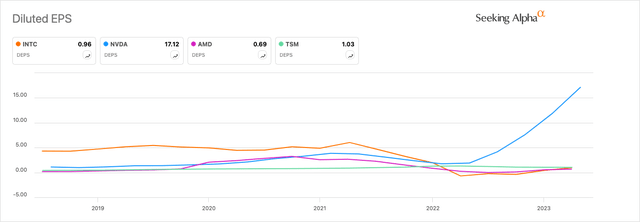

Intel has clearly been struggling more recently than the larger group, which can be seen in its historical earnings per share records over the past five years. We can also see how stark Nvidia’s success is in contrast to the other three companies:

Author, using Seeking Alpha

There are several reasons why I think Intel may struggle in the long term compared to AMD, Nvidia, and TSMC:

- Intel has suffered from delays in developing its semiconductor manufacturing process technology. TSMC and Samsung ( OTCPK:SSNLF ) have moved to 5nm and 3nm nodes, but Intel has faced delays in moving to 7nm (Intel 4) and 5nm (Intel 3) nodes.

- AMD and Nvidia are working on a Fabless model, using third-party foundries like TSMC. The Intel Device Manufacturer (“IDM”) model is more capital intensive, which impacts free cash flow and overall growth, and provides less flexibility.

- Nvidia has established itself as a leader in AI and machine learning with its CUDA ecosystem and specialized hardware like the Tensor Core. Intel’s acquisition of Habana Labs in 2019 and other attempts to penetrate the market still lag far behind.

- TSMC’s focus on being the world’s largest and most specialized foundry means it is likely to be the top choice for major Big Tech companies for the foreseeable future, enjoying economies of scale and more advanced capabilities. Intel’s IDM 2.0 strategy of producing its own chips and operating as a foundry may be too optimistic given the intense competition, straining resources to achieve lower-than-expected growth.

In my opinion, investors are more likely to see strong returns from Intel stock now that the valuation makes more sense. However, in the long term of 5-10 years and more, I think Intel’s growth story is unlikely to be as big as competitors AMD, Nvidia and TSMC. I believe Intel is positioning itself to benefit well from the growing demand for digital goods in society, as well as the future high global economic demand for AI chips and infrastructure, which should be very accretive for Intel, but investors should They should consider how much of this market will be captured by the leading companies in this field, most notably Nvidia in infrastructure, and TSMC in foundry services.

Evaluation analysis

Intel had a negative price-to-earnings ratio (GAAP) of -118 during my first coverage of the company. Now its ratio is ~32. I think this is very promising for short- to medium-term investors, especially since Intel is likely to benefit from the financial benefits of its recent investments in late 2024 and throughout 2025. Its generally accepted accounting P/E ratio is only +5% Difference from sector average. We can see in the peer analysis table above that Intel has the cheapest valuation at this time, with a price-to-sales ratio of 2.5, which is incredibly low compared to major competitors and even below the 5-year average for this ratio. From 2.9. Once Intel starts increasing its dividend later this year, the stock will likely look more attractive to investors, causing increased buying activity and pushing the price higher through momentum, including what I hope will be a significant series of growth outperformances. Earnings per share on an annual basis and potential profits throughout 2025.

Author, using Seeking Alpha

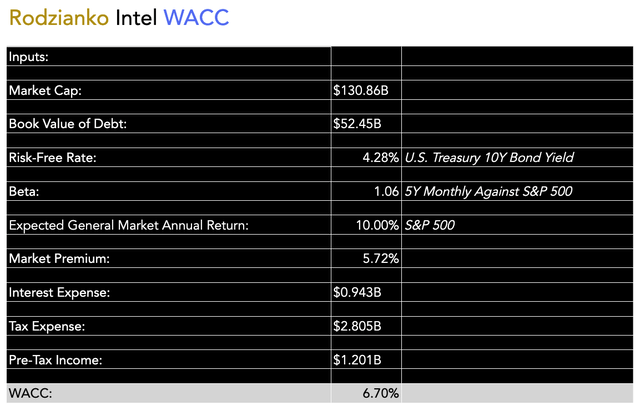

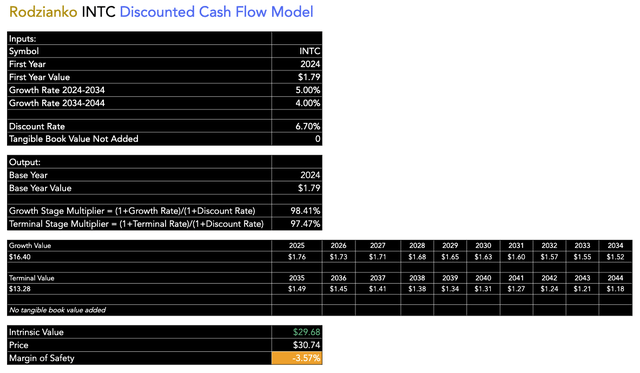

I also valued Intel using a discounted cash flow model, where I used its 10-year average FCF as a starting value because it currently has negative free cash flow. I have used the company’s weighted average cost of capital based on the inputs listed below. My model indicates that the stock’s value is approximate at this time, with a carefully calculated margin of safety at negative 3.57%.

Author account Author model

Main elements

Intel has faced significant earnings and price deflation over the past few years, but now conditions are starting to improve. Much of Intel’s recent decline can be attributed to rising startup costs, increased competition, and macroeconomic stagnation.

Intel faces stiff competition from upstarts, including Nvidia and AMD in chips and TSMC in foundry services. Intel is already lagging behind its leading peers in both aspects. Although Intel has strong exposure to digitization and artificial intelligence trends, the idea that it might be able to achieve the same high growth as competitors is likely too optimistic.

Intel is somewhat overvalued now after having been significantly overvalued in recent history. This is evidenced by the low forward price-to-sales ratio and the slight overvaluation indicated by the DCF model when using a 10-year average of the initial value of the cash flow stream.

Conclusion

In my view, Intel could be considered a buy now, if focused on the short to medium term. However, as a long-term investor with a holding period of more than 10 years, I assign a Hold rating because I believe Intel will face more growth challenges over the next decade. While its valuation is now reasonable, I believe investors can find better long-term, high-growth opportunities in the technology industry.