Tero Visalainen/iStock via Getty Images

Inter Perfumes (Nasdaq: Eibar) markets and distributes perfumes under a wide range of licensed brands. The company does not have manufacturing facilities, but obtains the required components through external supplier contracts.

The company is splitting it up Operations in European and US operations, as viewed at May 2024 Investor presentation. Inter Parfums has a 72% stake in operations in Europe, and is listed as a separate entity on Euronext Paris under the ticker ITP. The European side of the business, which accounts for 65% of Inter Parfums’ revenue, sells under brands such as Jimmy Choo, Montblanc, Coach and Lanvin along with many others. Inter Parfums, on the other hand, has entire operations in the US with brands like Guess, Donna Karan/DKNY and Ferragamo within this segment. Although the business divisions are divided into two geographical segments, Inter Parfums derives revenues from a high profile international customer base.

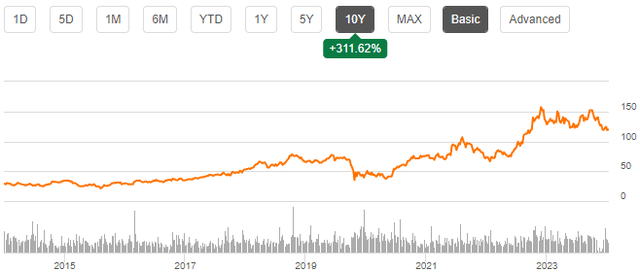

Because Inter Parfums has been able to achieve impressive earnings growth with very light capital requirements, the stock has returned extremely well in the past decade. The compound annual growth rate during this period is 15.2% from the rise alone, and in addition, the company distributes dividends with a current yield of 2.50%.

Ten year stock chart (Searching for Alpha)

Value earnings growth over the long term

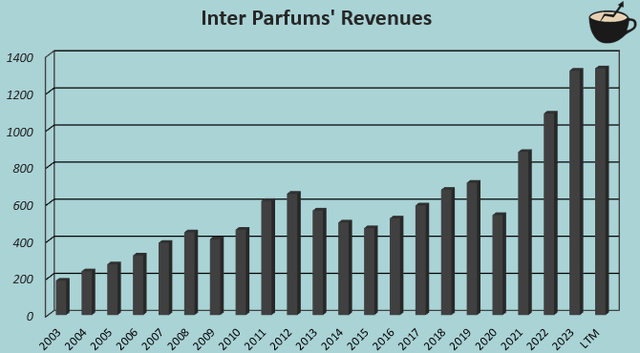

Despite some turmoil during the Great Financial Crisis, brand portfolio changes from 2012 to 2015, and the Covid pandemic, overall Inter Parfums has achieved impressive organic revenue growth. The company’s revenues grew at a CAGR of 10.3% from 2003 to 2023, and the growth is set to continue in 2024. Inter Parfums has been able to obtain fragrance licenses for an increasing number of globally recognized brands, resulting in good growth.

Author’s calculation using TIKR data

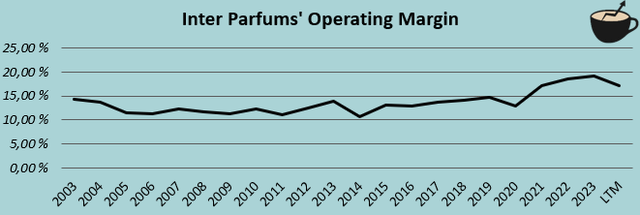

Along with strong growth, Inter Parfums has been able to achieve high and stable profit margins. Currently, the company’s trailing operating margin is 17.2%, higher than the 2014-2023 average of 14.7%, as higher revenues appear to have driven good operating leverage. Gross margin remained very stable, ranging from 53.7% to 56.9% from 2015 onwards.

Author’s calculation using TIKR data

Since Inter Parfums does not have manufacturing facilities, and operates through contractors, the company has a capital-light business model. In the past twelve months, there has been only $5.1 million in capital expenditures, and working capital needs have historically been very low, only disturbed in the past two years by inventories and receivables swelling. Return on equity is currently at a very healthy 20.4%.

Relying on licenses increases risks

Since Inter Parfums’ fragrance brands are licensed from well-established companies, the company relies on its ability to maintain a good licensing portfolio. The company spent about $238 million on acquiring intangible assets from 2014 to 2023 to maintain a healthy portfolio of licenses. The licensing-based business model is quite typical in the fragrance industry but still increases the risk of the stock.

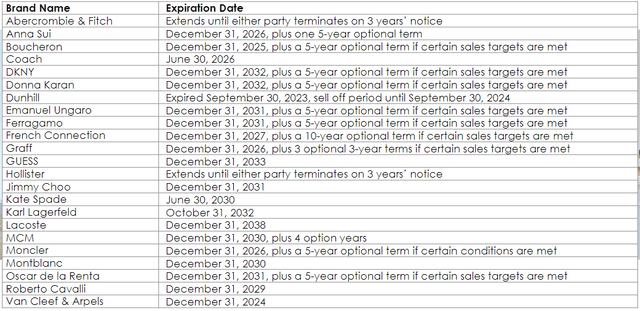

The company had already faced a major financial downturn due to the license termination – Burberry terminated the licensing agreement with Inter Parfums at the end of 2012, and being a very large revenue contributor at the time, the termination resulted in a collapse in Inter Parfums’ revenues and profits. From 2012 to 2014 as shown in the revenue chart. Although Inter Parfums’ licensing portfolio is now more diversified, and no single brand has the same weight as Burberry, the company still has licenses that represent a very notable portion of total revenues – for example, Jimmy Choo represents 17 % of net sales revenue in 2023, and although the brand license should not increase risk in the medium term as it expires at the end of 2031, it does increase risk in the long term. The trainer, which accounts for 15% of sales, expires in approximately two years at the end of June 2026.

Inter Parfums license expiration dates (IPAR presentation to investors in May 2024)

First quarter results showed temporary weakness

Inter Parfums’ Q1 report negatively surprised analysts, with the company reporting revenue of $324.0 million and earnings per share of $1.27, missing estimates by $4.7 million and $0.34, respectively. Revenue grew just 3.9% year over year, down significantly from 21.3% growth in 2023 as Inter Parfums customers reduced inventories in the quarter, according to the report. The company’s operating income declined by a significant -24.7% year over year but is mainly related to an incredibly strong comparable margin in Q1 2023.

Weaker growth is set to subside in 2024 as Inter Parfums reaffirms 2024 guidance. The company forecasts sales of $1.45 billion, up 10.0% from 2023. Adjusted EPS is expected to rise 8.4% to $5.15 – while The first quarter was weak, the problems seem to quickly fade away and return to good growth.

There is expected to be a reasonably long growth runway

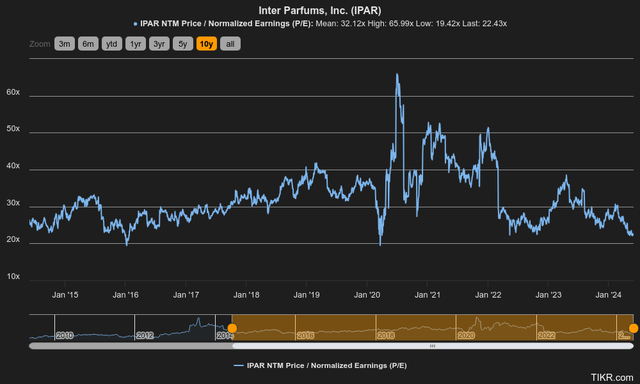

A good amount of growth has been priced into the stock – while the current forward P/E of 22.4 is below the 10-year average of 32.1, the earnings multiple is still very high and appears to be pricing in continued growth.

Historical Forward Earnings Multiple (10 years) (Taker)

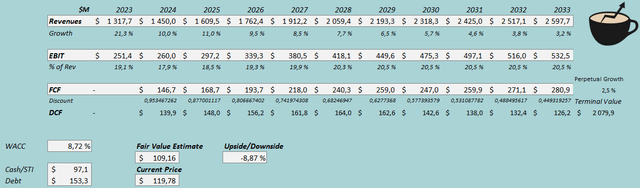

To estimate the fair value of the stock, I built a discounted cash flow model. In the DCF model, I estimate a sustained 10.0% growth in revenue growth in 2024 and 11.0% in 2025. After that, I estimate growth to slow to a final permanent growth of 2.5%, representing a total CAGR of 7.0%. From 2023 to 2033.

I estimate some additional operating leverage for EBIT margin from 19.1% in 2023 to a final level of 20.5%. The company’s capital-light business model does not tie up a lot of capital, which makes its cash flow conversion very good. I expect an even worse turnaround from 2030 onwards, as licenses for prominent Inter Parfums start to expire. The transfer also represents a 28% minority stake in Inter Parfums’ non-owned European operations.

Using these estimates, the DCF model estimates Inter Parfums’ fair value at $109.16, about 9% below the stock price with the May 31 closing price – a good growth runway for the stock is priced in. A longer-than-expected growth story could make the stock undervalued, but since the licensing portfolio adds to Inter Parfums’ long-term growth risk, I think the valuation is mostly balanced.

Discounted cash flow model (author’s account)

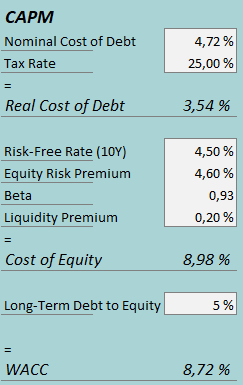

A weighted average cost of capital of 8.72% was used in the DCF model. The weighted average cost of capital (WACC) used is derived from the capital asset pricing model:

CAPM (author’s account)

In the first quarter, Inter Parfums had $1.8 million in interest expense. With the company’s current amount of interest-bearing debt, Inter Parfums’ annual interest rate is 4.72%. The company benefits from a very small amount of debt, and I estimate that its long-term debt-to-equity ratio is only 5%.

For the risk-free rate on the cost side of stocks, I use the ten-year US bond yield of 4.50%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the US, updated on January 5. Seeking Alpha rates Inter Parfums’ beta at 0.93. Finally, I add a small liquidity premium of 0.2%, creating a cost of equity of 8.98% and an average cost of capital of 8.72%.

Away

Inter Parfums has an impressive growth runway behind the company, and despite weak growth in the first quarter, the growth story continues with strong momentum. The company was able to acquire a valuable licensing portfolio, and although Burberry license terminations slowed from 2012 to 2014, Inter Parfums was able to grow successfully thereafter. I continue to believe that the risks surrounding obtaining licenses, especially as currently held licenses begin to expire, increase long-term growth risks. The current rating expects a fair amount of future growth given the licensing risks, and as such, I have a Hold rating for now.