Mr. Pliskin/E+ via Getty Images

Written by Padraic Garvey, CFA

Lowering interest rates is an important signal for bonds, sending good things for yields

One of the main themes running through our analysis is the idea that the past decade and a half has been like that Not a normal period to indicate the near future. We have witnessed the global financial crisis, the European sovereign debt crisis, and the pandemic during this period. All of this has put significant downward pressure on interest rates and bond yields. Of course, bad things can happen again in the future (and likely will), and that remains the rationale for having a diversified portfolio that includes decent exposure to bonds. However, from a relative value perspective, this is not enough to justify the material’s lower yields, at least not in light of what we know.

Last week we sent From the piece that says 4.5% as the balance area for 10-year yield in the United States. It is not far from where we are now. We then see 5% as a level we can move towards, given stable inflation and ongoing supply pressures. To change this dynamic, we need to see interest rate cuts by the Fed, as history shows that the onset of interest rate cuts usually coincides with material downward pressure on bond yields. This could actually push the 10-year yield into the 4% region.

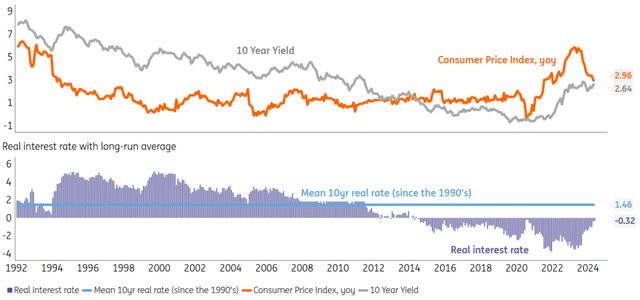

But if there are no cuts in 2024 (which is not our view), there is also little possibility that the 10-year bond yield will fall in a material way. Moreover, with real yields so low, falling inflation is not enough to justify lower yields. Only Fed cuts (or large ones) can stimulate substantial declines in 10-year yields – and this, of course, requires lower US inflation as a premise.

Real prices are still very low. Therefore, a decrease in inflation does not mean a certain decrease in bond yields…

Source: ING estimates, Macrobond

The chart above shows something similar for the Eurozone. There are several real yields you can choose from, including the obvious one – the eurozone real yield. But the chart focuses on the German language, on purpose. It shows that the 10-year real yield is still exceptionally low compared to history. Quite similar to what happened in the US, there is a comfortable spread of about 1% between today’s real return and its long-term average. There are two ways for the real yield to rise. The most obvious possibility is that inflation will continue to fall. The other is rising bond yields. One does not mean the other. In other words, lower inflation in the eurozone does not translate directly into lower yields, at least not without more.

The ECB’s cuts are constrained by the Fed, which remains on hold, and by falling real bond yields

The main difference between the Eurozone and the United States is that the European Central Bank cut interest rates, and by definition peaked in this cycle. It’s possible that the Fed has peaked as well, but the forecast is more accurate. There is a clear discount on the Fed’s rate cut, but the timing of delivery is more ambiguous. This puts some brake on the ability of euro zone yields to fall significantly.

But this also reflects a very complex prognosis of what will happen next. Usually, the first cut is followed by more cuts. The same is likely to be the case here – although there is a lively ongoing debate about this. Bottom line, the ECB’s cut is significant. But unusually, this does not send a convincing message in a bull market.

Content Disclaimer

This publication has been prepared by ING for information purposes only without regard to a particular user’s means, financial situation or investment objectives. The information does not constitute an investment recommendation, nor is it investment, legal or tax advice or an offer or solicitation to buy or sell any financial instrument. Read more

Original post