bjayam/iStock via Getty Images

the iShares US Financial ETF (NYSEARCA:IYF) is a broad, value-weighted portfolio in a subset of US financial institutions, thus banks and insurance companies. The beta version of deposits is being launched for banks, so there is not much accretion anymore Benefit from higher rates. Mergers and acquisitions are improving for full-service banks. Higher rates mean better performance for insurers’ reserve portfolios as well.

Overall, the rising rate environment is very good for the IYF ETF, to the point where it doesn’t start to cause major credit issues, which would have a big impact on bank stocks. We are relatively confident in the US economy, and we also believe that the idea of the CPI going from 3.5% to 3.4% is a “cold” idea and a joke, especially when it comes to inflation expectations, which is arguably the number one leading indicator and a reason of inflation, well above the policy level and slightly below current CPI numbers.

Overall, we think financials remain a good choice, but we might go further and choose insurance companies to avoid the direct consequences of credit issues with ETFs like the iShares US Insurance ETF (IAK), which is the same conclusion we reached in our recent coverage of IYF.

Collapse of the International Youth Federation

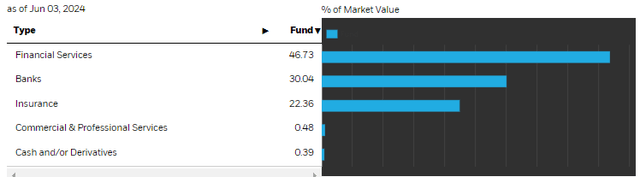

The IYF ETF contains the typical large-cap stock names that dominate US indices overall. Let’s take a little closer look at sector exposures.

Sectors (iShares.com)

Financial services should include conglomerates such as Berkshire (BRK.A), perhaps rating agencies, brokerages, derivatives and equity exchanges, and most likely private equity funds and asset management companies. Berkshire is primarily an insurance exposure, due to the high tilt toward its insurance business. The banks are full-service banks and regional banks. Insurance is clearly the first line, with reinsurers in ETFs.

Overall, a very uniform distribution, especially given the details of BRK, between insurance, banking and financial services.

Let’s start with our view on pricing because it is a common systemic factor for all companies, and a point where the market frequently gets it wrong. Inflation does not subside just because it has fallen by 10 basis points. Inflation expectations are at 3% over the next five years according to a Michigan survey. This tells you that inflation above 2% interest rates is not only persistent, but clearly well entrenched. The Fed has so far failed to try to bring inflation down quickly before stabilization occurs, as people like Fed Governor Michael Bowman had hoped early in the inflation battle.

The Fed may be counting on maturity walls for 2024 and 2025 to help drive the recovery Bullet of mercy At current rates. We’ve also seen that this can have a big impact. However, our internal view has changed to include the fact that refinancings are occurring very quickly, with corporate debt in high demand. We are puzzled by the fact that credit spreads have reached record lows despite what we believe are important outstanding questions about inflation and the health of the economy. Confusing or not, it points to demand for corporate issuance and means that even high-yield issuers are smoothing maturity filings, and their issuances likely won’t translate into employment numbers very quickly, which will have a traceable impact on inflation depending on It is expected. Phillips curve.

There is some decline in job availability, suggesting a slight slowdown in the labor market, but according to economic theory, and really basic logic, that will have no impact on inflation.

As a result, with smaller caveats on maturity walls, and refinancings still occurring at higher rates and putting some pressure on issuers, rates are likely to remain higher for longer. Recessions for other reasons would be needed to break the current pace of rotation of wages and prices.

minimum

High interest rates have already reached peak benefits for banks. National Insurance Institutions have reached their peak, and in some cases, as at Bank of America, there are clearly declines to come. Loan growth is very modest at present, and fee income is not enjoying much momentum either. The next stage may be credit issues, which we would prefer to avoid.

For insurance, a longer rally is great because it means they can replenish their buffer portfolios, which are mostly made up of fixed-income securities, at higher rates.

With regard to financial services, the picture is more mixed. For P/E, it’s certainly not great, and for asset management, it’s also not great as deposit interest rates and other easier savings alternatives have become very formidable competitors. AM also faced the problem of inflation in the fixed cost base, which affected the performance of the shares. As for brokerage firms, it’s also not great because they keep people on the sidelines. However, rating agencies have a lot to do lately, due to major maturity walls in 2024 and 2025.

The clearest picture of insurance. An insurance ETF would be better for us, or perhaps some specific picks if we were more confident in insurance prices in some markets than others. Especially when the P/E ratio is so similar between IAK and IYF, both at around 15x. Expense ratios are also the same at 0.4%.