hapabapa

In general, I don’t gravitate too much towards apparel and apparel companies. This is especially true for those with a retail presence. However, more often than not, I make an exception. After all, it’s important to be flexible when it comes to opportunities.

One company I’ve identified that is definitely interesting is JGIL Company (New York Stock Exchange: Jill). With a physical presence of over 200 stores, the company is a big player in the apparel retail space. Admittedly, it’s not huge. But with a market cap of $380.5 million as of this writing, it should come across most investors’ radar at one point or another.

Over the past few years, the company has achieved financial results that have been decidedly mixed. Revenues were a bit lumpy, while earnings and cash flows were as well mixed. However, the company’s stock prices look attractive, especially compared to other clothing and apparel retailers. With profits covering the first quarter of 2024 It is expected to be announced Before the market opens on June 7, investors will have a lot to look forward to.

Despite my concerns about retail in general, the company looks attractive enough to warrant a weak “buy” rating. But obviously this could change based on new data that emerges when management announces earnings.

A retailer worth considering

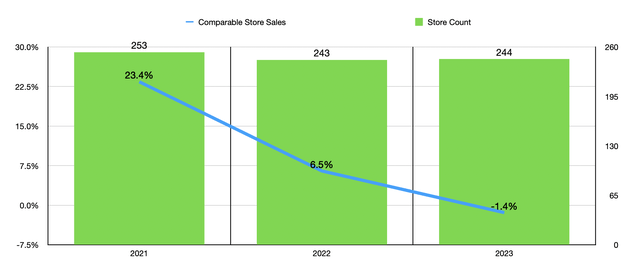

According to J.Jill’s management team, the company is a lifestyle company that sells clothing, shoes and accessories to its customers. Its focus is serving women, usually 45 or older. But it is not limited to any woman. The company locates its stores and prices its products to appeal to those with an average annual household income of about $150,000. In terms of physical presence, as of the end of fiscal year 2023, the company had 244 operational stores. This represents an increase from the 243 stores operating one year ago, but is down from 253 stores at the end of 2021.

Author – SEC EDGAR data

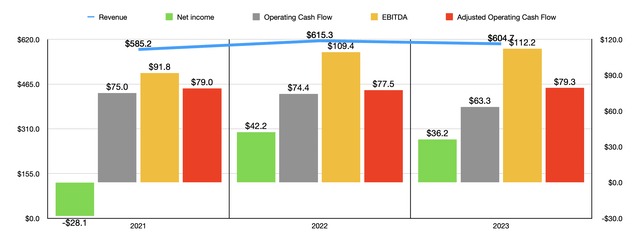

After the pandemic ended, the company saw an initial boom in comparable store sales. In 2021, this percentage reached 23.4%. But that’s to be expected when you consider how much pain the pandemic has caused any business with a storefront. We’ve seen some weakness since then. In 2022, comparable store sales growth was approximately 6.5%. But then, last year, comparable store sales fell 1.4%. Despite these problems, the company’s overall revenues have remained in a fairly narrow range. Sales expanded from $585.2 million in 2021 to $615.3 million in 2022. However, in 2023, sales declined to $604.7 million.

Author – SEC EDGAR data

It is worth noting that in addition to its physical locations, J.Jill sells its products through its own e-commerce platform and catalog. Management considers these two different sources of revenue as the “direct channel” for the company. About 47% of total revenue in 2023 came from these specific activities. Of that, about 95% is attributable to e-commerce operations. The remaining 5% were for orders placed over the phone after customers had viewed products in the retailer’s catalogue.

Bottom line, the picture has been somewhat mixed for the company. In 2021, the company already had a net loss of $28.1 million. This turned into a healthy profit of $42.2 million after one year. But with lower revenues in 2023, net profits fell to $36.2 million. Other profitability metrics were also mixed. Over the past three years, operating cash flow has consistently declined, falling from $75 million to $63.3 million. However, if we adjust for changes in working capital, we get a very narrow range of $77.5 million to $79.3 million. The only profitability metric that improved year over year was EBITDA. This has continually grown, rising from $91.8 million in 2021 to $112.2 million last year.

Before we move on to evaluating the company, it’s important that I cover the update provided by management. This update was released on May 14 of this year. After the end of the first quarter of 2024, J.Jill’s management team decided to use some of the company’s available cash to pay down debt. At the end of 2023, the company had $155.9 million in debt on its books. It also had $62.2 million in cash. All of this debt was in the form of a $175 million term loan that the company took out in April 2023. Management decided to allocate $60.4 million to repay the debt, bringing the total debt balance as of May 10 of this year to $108 million. .

The company was not required to do this. But it seemed like it made financial sense. As of the end of this debt reduction move, the company claims to have $28.2 million in cash on its books. The management also feels confident in the company’s position to the extent that it has decided to pay a regular quarterly dividend of $0.07. This translates to a yield that is now around 0.8%.

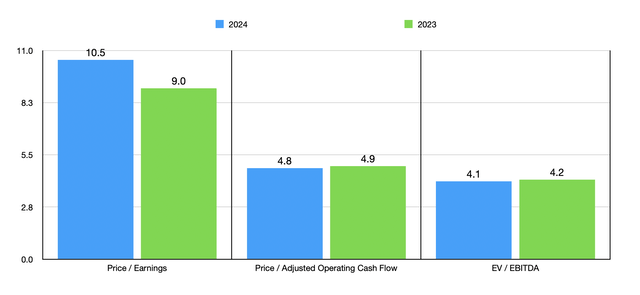

Personally, I would have preferred the capital to be used to further reduce debt or improve operations. But at least management has a strategy in place for how to allocate capital. Having said that, for the purpose of analyzing this company, particularly when evaluating it from an EV to EBITDA perspective, I’m using these updated numbers rather than the results announced at the end of last year.

Author – SEC EDGAR data

If we use historical results from 2022 and 2023, we can value the company as shown in the chart above. On a price-to-earnings basis, the stock seems fairly fair value for a retail play. But when it comes to cash flows, things look very positive. It’s rare to find a company that has price-to-cash flow multiples in the low to mid-single digit range.

In the table below, I then decided to compare the company to five similar companies. What I found is that, on a price-to-earnings basis, it ended up being the cheapest company of the bunch. On a price-to-operating cash flow basis, two of the five companies ended up being cheaper than it. But when it comes to EV’s approach to EBITDA, our candidate was once again the cheapest of the bunch.

| a company | Price/earnings | Price/operating cash flow | Value added/EBITDA |

| ing generation | 10.5 | 4.8 | 4.1 |

| Zoomiz (Zoomz) | 126.1 | 25.1 | 41.2 |

| Genesco (GCO) | 57.5 | 3.1 | 25.5 |

| Urban Outfitters (URBN) | 13.3 | 7.4 | 7.1 |

| End of lands (pounds) | 36.3 | 3.4 | 6.8 |

| American Eagle Outfitters (AEO) | 19.5 | 7.8 | 6.4 |

As I mentioned at the beginning of this article, things can change, for better and for worse, as new data emerges. It so happens that, before the market opens on June 7th, management is expected to announce financial results covering the first quarter of fiscal year 2024. When the company issued its press release on May 14th, management stated that revenues would reach about $160 million for the quarter. They also estimated EBITDA at between $33 million and $34 million. Analysts also expect revenue of $160 million. But they did not themselves provide EBITDA estimates. On the other hand, they estimate that earnings per share will be around $1.20. This would translate to $17.3 million in net profits.

If all of this comes to fruition, revenue would represent a nice improvement over the $149.4 million reported in the first quarter of 2023. EPS would also come in well above the $0.32 reported last year. This means net profits are nearly four times higher than the $4.6 million the company reported last year. In the table below, you can also see other profitability metrics for that time. If revenues and profits are rising, they likely will be.

Author – SEC EDGAR data

Away

Although certainly not a prime candidate for investors, J.Jill, Inc. Sounds like an interesting opportunity to me. The stock looks attractively priced, and the company is back in the mood of increasing its store count rather than reducing it. Revenues, profits and cash flows also appear to be on the rise. Given these factors, along with management’s decision to reduce debt, I would argue that a soft ‘buy’ rating is appropriate at this time.