Japanese government bond yields reach 13-year high, while yen is at 34-year low (USD:JPY).

Takasu/iStock via Getty Images

Japanese government bond yields rose to a 13-year high, while the Japanese yen fell to a 34-year low.

Both are a result of the Bank of Japan (“BOJ”) remaining behind the curve in terms and normalize its monetary policy.

While the Bank of Japan ended its negative interest rate policy in March, the interest rate increase to 0.0-0.1% still leaves the Bank of Japan woefully behind the rest of the developed world.

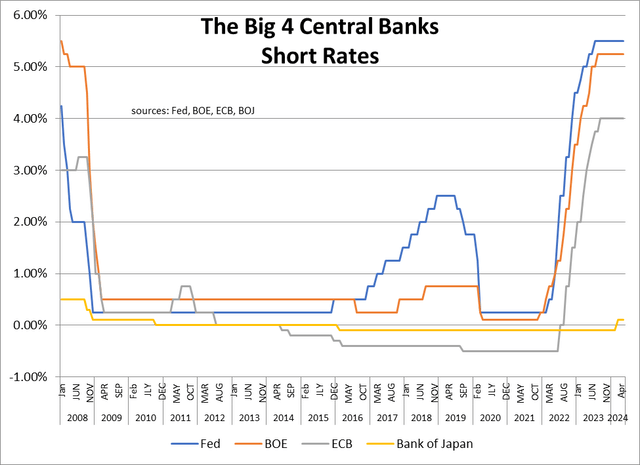

Federal Reserve, Bank of England, European Central Bank, Bank of Japan

With short-term interest rates at the Fed at 5.5%, the Bank of England (BOE) at 5.25%, and the European Central Bank (ECB) at 4.0%, yield gaps are so wide that investors are selling Japan to buy shares in the ECB. High yield markets.

This is putting pressure on Japanese government bond yields and the yen, despite talk of Fed easing Sometime this year, the European Central Bank is expected to cut interest rates as soon as this week.

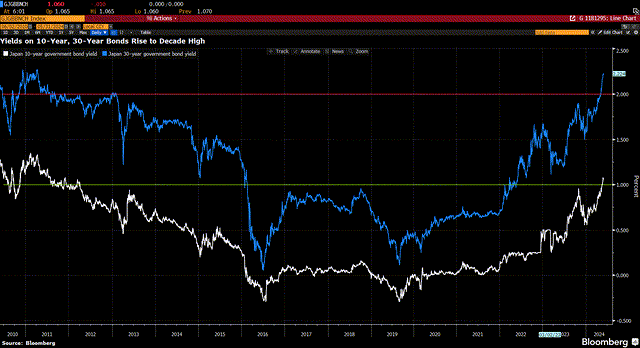

Japanese government bond yields

The yield on 30-year Japanese government bonds reached 2.22%, while the benchmark yield on 10-year Japanese government bonds reached 1.09%, both their highest levels since 2011.

Bloomberg

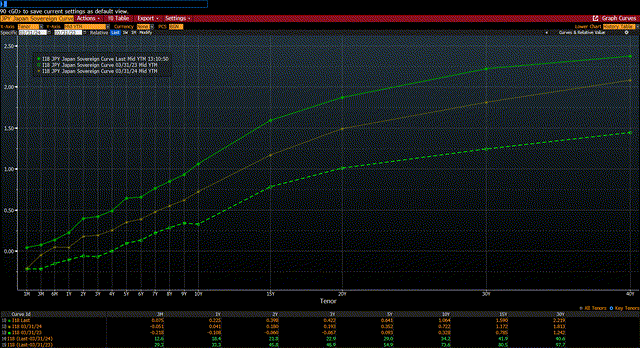

Most of the recent rise in yields has come under Bank of Japan Governor Kazuo Ueda. In fact, the entire Japanese government bond yield curve shifted significantly upward during his tenure.

Ueda began his term in April 2023. Since then, 1-year JGB yields have risen by 33 basis points, 10-year JGB yields have risen by 74 basis points, and 30-year JGB yields have risen by 98 basis points . The ten basic points adopted by the Bank of Japan in tightening monetary policy so far are insufficient.

The market demands more.

Bloomberg

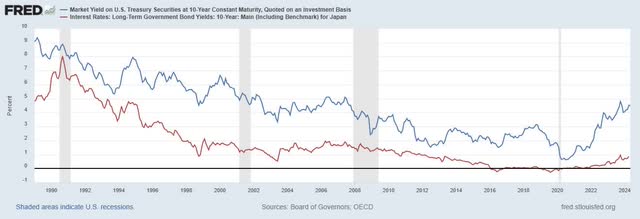

JGB yield gap with US Treasuries

Even with the recent rise in 10-year Japanese government bond yields, the yield gap with the US 10-year Treasury bond (US10Y) has widened to 350 basis points.

unique

Japanese Yen

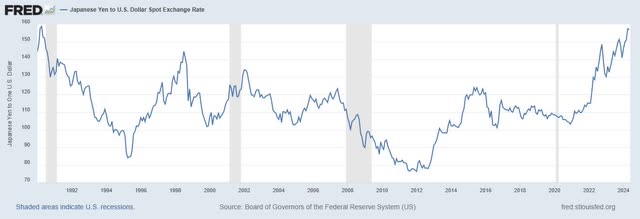

The wide spreads in yields led to outflows from Japan, causing the yen to weaken to its lowest level since 1990.

unique

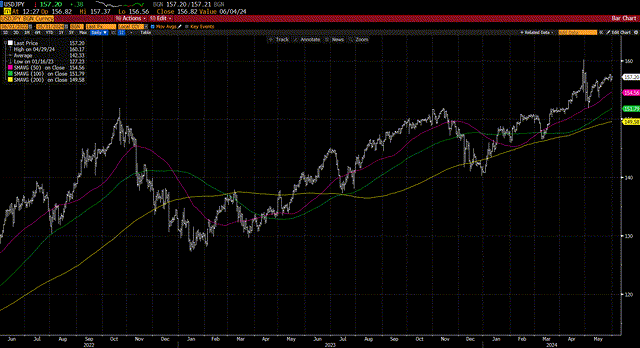

The sell-off in the yen has been particularly sharp since Ueda became governor of the Bank of Japan. When he assumed the presidency of the Bank of Japan in April 2023, the yen was at 133 yen to the dollar. Then it decreased by 15.2%.

Currency intervention

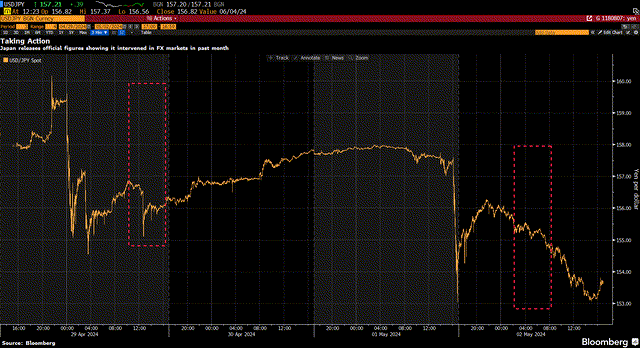

The Bank of Japan was so concerned about the yen’s devaluation that it took the rare step of intervening in currency markets to provide support at the 160 yen to the dollar level. On two separate days, April 29thy And May 2Second abbreviationThe Bank of Japan spent an all-time high of 9.8 trillion yen ($62.2 billion) to defend the currency.

Bloomberg

The short-term effect was to cause the yen to rise to 152, a 5.2% move, but over the next month it fell to 157, undoing the 3.2% gain.

The Bank of Japan’s move surpasses the previous record 9.2 trillion yen ($60.5 billion) of support during its last intervention in October 2022, when it intervened with the yen trading at 152 yen.

Bloomberg

Uncertainty in the Bank of Japan’s policy

The Bank of Japan has been moving too slowly in its policy normalization, which has led to weakness in the Japanese government bond market and the yen.

Ueda hinted that more efforts needed to be done, but the lack of clarity caused weakness.

Many expect a further rate hike in June or July.

In addition, there is uncertainty about the Bank of Japan’s plan to reduce bond purchases. When the Bank of Japan exited its negative interest rate policy in March, Ueda was careful to point out that the policy would remain accommodative. They will continue purchases of Japanese government bonds in the same amount as before.

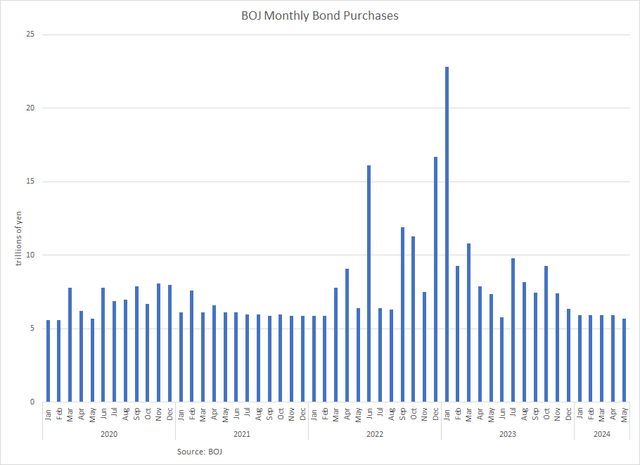

However, the Bank of Japan has been slowly reducing its purchases of Japanese government bonds. They bought 6.0 trillion yen worth of JGBs in February, 5.9 trillion yen worth of JGBs in March and April, and 5.7 trillion yen worth of JGBs in May. JGB’s purchases last month were the smallest amount since May 2020.

Bank of Japan

What no one has noticed is that the Bank of Japan’s holdings of Japanese government bonds are maturing at a rate of 70 trillion yen per year. This translates into a monthly runoff of 5.8 trillion yen. Therefore, if the Bank of Japan continues to reduce its monthly purchases, contrary to its accommodative policy, it is in effect reducing its holdings of Japanese government bonds.

Liquidity

The bond sell-off has contributed to a liquidity problem in the Japanese government bond market, as measured by the Bloomberg Japanese Government Bond Liquidity Index.

Liquidity has deteriorated to the level seen during the Great Financial Crisis of 2008. The only period worse was when the Bank of Japan surprised the market in December 2022 by doubling its yield curve control band and tripling its purchases of Japanese government bonds to defend the band against speculators.

Bloomberg

Conclusion

The Bank of Japan has been slow to normalize its monetary policy, which has led to a sell-off in both the Japanese government bond market and the yen. Further tightening is necessary to stem outflows. The Bank of Japan must act more quickly and with greater clarity.

Editor’s Note: This article discusses one or more small-cap stocks. Please be aware of the risks associated with these stocks.