Kwarkot/iStock via Getty Images

introduction

One of the main characteristics of CEFs is the NAV discount, which is typically used to measure how cheap a CEF is in the market. There are various reasons why mutual funds are cheap. As Interested investor, I often watch the NAV discount of well-managed mutual funds. Noveen Real Estate Income Fund (New York Stock Exchange: GRS) is such a fund with a NAV discount of 12.44%, which looks very cheap and attractive to me.

JRS is managed by Nuveen, who is known as an expert in the field of CEF. The funds’ portfolio is about 2/3 as heavy as real estate investment companies. Compared to the broader market, the REIT sector is still performing very poorly, and the JRS NAV discount provides an excellent opportunity to raise capital when the REIT market really wakes up.

In the At the current price level, the fund pays dividends in excess of 9%, making it very attractive to income-oriented investors, especially retirees who may rely on the 7% withdrawal rule to offset the impact of high inflation. JRS shareholders will be well paid while they wait for the REIT market to emerge. I give JRS a Buy rating. I recently opened an initial JRS position in my income portfolio. I plan to add more JRS shares before the NAV deduction starts to narrow in a meaningful way.

Highlight JRS Fund

JRS is a CEF fund with a heavy focus on the REIT market in its portfolio. It is managed by Nuveen, which is considered one of the best companies in managing mutual funds and real estate investment fund assets. The following from the official JRS document is a good summary of the Fund’s purpose and strategy:

The fund’s investment objective is to increase current income and capital appreciation. The Fund invests primarily in income-producing common stocks, preferred stocks, convertible preferred stocks, and debt securities issued by real estate companies. At least 75% of the assets managed by the Fund will be in investment grade securities.

The ETF was founded in 2001. The fund has total assets of $243.85 million. Daily trading volume is usually around 50k. Given its history of more than 20 years, it is not a very popular fund. An expense ratio of 1.53% is quite typical for mutual funds.

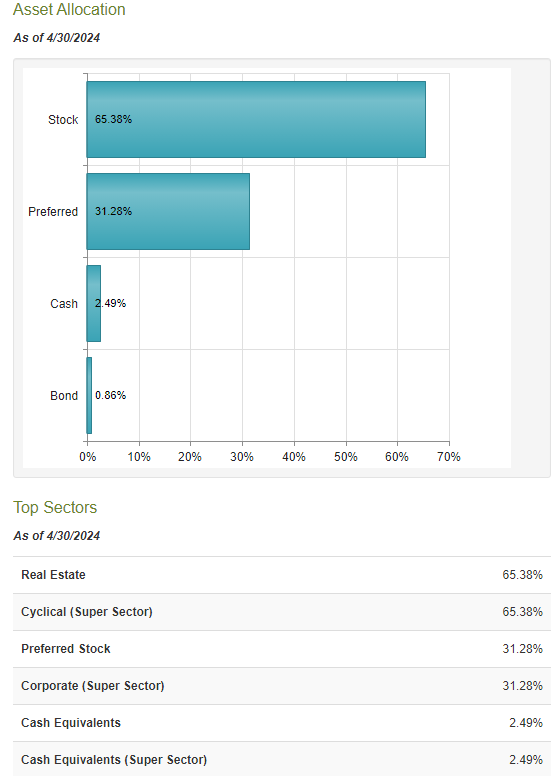

The following shows the fund’s asset distribution and sector division:

Allocate JRS assets and sectors from CEFConnect

The weight of the REIT is 65.38%. There is a weighting for corporate preferred stock of 31.28%. Preferred stock is used to collect high-yielding dividends from issuers. Note that preferred stocks are classified as fixed income assets with low volatility. 31.28% is a good ratio in the portfolio, which helps offset the high volatility of REIT holdings.

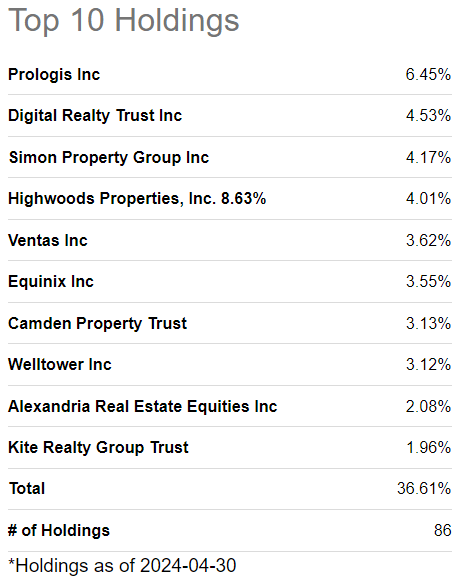

The total number of holdings is 86. Below is a glimpse of the top holdings. The top 10 holdings represent 36.88% of the portfolio. These are large-cap stocks and blue-chip REIT stocks. I believe they are all leaders in REITs in their industries, including industrial, data centers, storage, healthcare, etc. Below is the market cap information for all top ten holdings: #1 $102.34 billion, #2 $48.79 billion, #3 $57.51 billion, #4 $2.76 billion, #5 $20.28 billion, #6 $72.00 billion, #7 $11.60 billion, #8 $62.79 billion, #9 $20.34 billion, #10 $4.91 billion. With the exception of No. 4, they all received a consensus Buy rating from Wall Street analysts. #4 is an office REIT rated as holding.

JRS Top 10 Collectibles from SA

The fund pays dividends of 9.2%. This was one of the main attractions for me when I opened the initial position in my portfolio. Keep in mind that not many REITs can produce dividends of 9% or higher. None of the top 10 holdings in JRS’s portfolio pay dividends anywhere near this high.

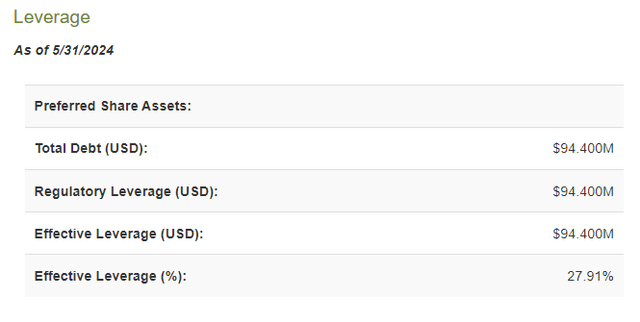

JRS uses high leverage to enhance returns. The leverage itself is normal debt (loans). The current leverage ratio is 27.91% as shown below. It is actually slightly lower than the average CEF, which is around 31%. I think the leverage ratio spread may actually prove the effectiveness of the fund’s management team, because lower leverage means lower borrowing costs. This can reduce the fund’s expense burden under the high interest rate situation.

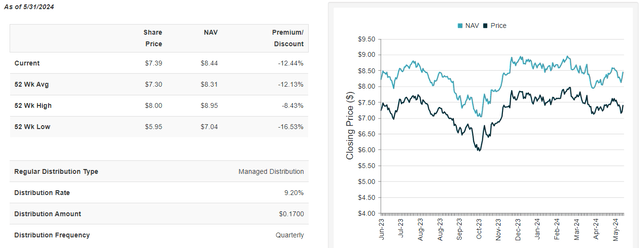

JRS NAV discount from CEFConnect

The deep discount to NAV puts JRS well positioned for a REIT rebound.

As of May 31, JRS was trading at a discount of 12.44% to its net asset value. As shown below, the discount is still slightly larger than the 52-week average (12.13%). Therefore, I think there is a lot of room for JRS to catch up and narrow its NAV discount gap.

JRS NAV discount from CEFConnect

In my opinion, the REIT sector will rebound sooner rather than later. Once that happens, the recovery could be significant due to the extreme underperformance in the REIT sector over the past three years. In fact, the REIT index remains at its five-year level while the rest of the market is making new highs. I have discussed a ‘The inevitable REIT rebound’ In my previous article about another REIT CEF RNP. Interested readers can find more details there. Here I just want to quote the next part “If the Fed starts lowering the interest rate, not only will this reduce the burden of interest expenses on the RNP, especially for high leverage, but the underlying REIT assets in the portfolio will also become more valuable.”. The same can be said for JRS as well. JRS’s 27.91% leverage may work well once interest rates peak during the cycle. Any reduction in interest rates will be a tailwind for highly leveraged REITs. The lower cost of leverage typically helps REIT CEFs outperform (non-leverage) REIT ETFs.

Looking ahead, I don’t think the Fed’s plan to cut moderate interest rates will be changed in 2024, despite all the recent major news about what and when the Fed might do with interest rates. Actual economic data shows a significant slowdown in US GDP growth. In fact, GDP growth in the first quarter was 1.6%, below expectations. The latest Fox Business News report was dated June 5 “…We’ve had disappointing retail sales. We’ve had disappointing PMI manufacturing numbers. And the ISM numbers have been disappointing.” I believe the next rate change from the Fed will be a (moderate) rate cut to save the economy from further sliding into recession. So interest rates have effectively peaked right now, and deep discount JRS is well positioned for the next REIT rebound.

Activists are looking forward to significant reductions in net asset value.

There are ongoing battles over control of some CEF funds (with significant discounts to net asset value) between activists and major CEF players, including BlackRock and Nuveen. One recent event related to Nuveen is the right to vote, as Businesswire.com reported:

On January 14, 2021, Saba filed a lawsuit against Nuveen and the trustees after they stripped voting rights from shareholders in their closed-end fund. On February 17, 2022, the court issued a summary judgment in favor of Saba and invalidated the actions of Nouvin and the trustees.

Although it is not entirely clear who will be on the winning side in terms of investment return, such events will typically help prompt Nuveen to do something to narrow the NAV discounts of its CEF funds, which in turn could benefit shareholders in these funds. . Funds, including JRS.

JRS is a good candidate for a retirement plan with a 7% rule to combat high inflation.

The 7% rule is often viewed as a solid retirement withdrawal plan. This is because the portfolio will quickly shrink in total capital if 7% of it is withdrawn each year. I believe the best way to comply with the 7% rule is to include high-yielding, high-quality properties in your retirement portfolio.

Note that a retirement withdrawal plan under the 4% rule makes more sense in preserving portfolio capital. The 4% rule makes the portfolio last longer than using the 7% rule. Many blue-chip stocks, such as those in the Dow Jones Index, have dividends around this yield level. Some popular ETFs, such as SCHD and VNQ, also offer relatively stable dividend payouts with a yield of around 4%. However, in an inflationary environment with a “higher for longer” rate requirement, the 7% rule is more desirable because the 4% rule may not be enough to cover inflated retirement expenses. This is where JRS shines with a dividend yield of over 9%.

Some income investors like me are often skeptical about high-yielding stocks, believing that the returns come from a falling stock price and may be unsustainable from a company fundamentals perspective. These are legitimate concerns. Finding good stocks for a high-yielding retirement portfolio is often a very difficult task.

With JRS, I can put an end to many worries for the following reasons:

- REIT assets are known to be inflation-proof. It’s always a good strategy to own some real estate. REITs are similar alternatives. JRS is cheap with a significant discount to NAV, so it has a price advantage over many other REITs. See more analysis below.

- High-quality fund REITs are often selected by leading experts in the field. Nuveen Real Estate is “one of the world’s largest investment management firms with $147 billion in assets under management,” according to its official website. This has laid a solid foundation for the good fundamentals that will be created with JRS. The top holdings discussed earlier are good examples of high-quality REIT companies.

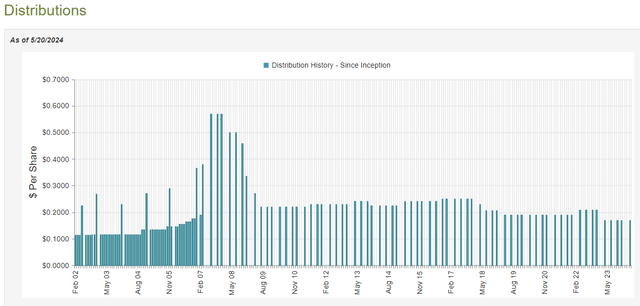

- Well-experienced management works hard to maintain the fund’s performance in terms of high-yielding returns and distributions. I think this is a reassurance to passive investors. Below is the distribution history of JRS since February 2002. It can be seen that the distributions have remained at high levels. I believe this is largely due to the “85+ years of real estate investing experience and 785+ employees” at Nuveen Real Estate, as stated on the Nuveen website.

JRS distribution history from CEFConnect

With a yield of 7.88%, another REIT RNP is also an excellent candidate for a retirement portfolio with the 7% rule. The following table was compiled when building my REIT portfolio, with RNP and JRS being the first two choices. The table shows that JRS is more volatile than RNP, as measured by 52-week historical volatility. Therefore, JRS is considered more dangerous than RNP. While RNP is my first choice for a CEF REIT due to its lower volatility and much larger size in assets under management, JRS may offer more upside potential for total return due to its higher yield and deeper NAV discount.

REIT CEF comparison from the author, may be outdated, for reference only

Risks and warnings

For long-term investors, significant price pullbacks for the REIT market may occur during a financial crisis, such as the Great Financial Crisis of 2008, and the US regional banking crisis in 2023, when the REIT sector was hit hard. For highly leveraged CEF funds, it can be very difficult to recover these withdrawals. This is a major risk factor that shareholders must take into account.

The REIT market is very sensitive to rising interest rates. Any further hike in interest rates would be a major headwind for the REIT sector. If the Fed is forced to increase its anti-inflation efforts, hope that REITs will rebound quickly may diminish. I believe the Fed will have to deal with an increasingly weaker economy, as discussed earlier in the article. Therefore, the chance of another rate hike is slim, in my opinion.

Unlike many other mutual funds with a monthly distribution, JRS has a quarterly dividend payment schedule. This may not seem appropriate for investors who rely on monthly income to pay bills.

Conclusion

The JRS Specialty REIT is a well-managed CEF. They are cheap with a discount to NAV of over 12% and are well positioned for a recovery in the REIT market. The 9.2% yield JRS is also a good choice for a retirement portfolio that deploys a high withdrawal plan, such as the 7% rule. I have a Buy rating on JRS.