KBC Group remains one of the best income options in the European banking sector (OTCMKTS:KBCSF)

Noel Bennett

KBC Group (OTCPK:KBCSF) offers a sustainable high dividend yield within the European banking sector, but its valuation seems fair at the moment.

As I’ve covered in previous articles, KBC is one of my favorite European banks because of what it offers Strong fundamentals and attractive income profile. However, I lowered my recommendation a few months ago because interest rates were at record highs in Europe and there was some possibility of a rate cut in the future, which would be negative for its earnings momentum.

Although the European Central Bank has already cut its key interest rate recently, interest rates remain relatively high in Europe, which is a positive backdrop for retail banks, such as KBC Bank. This has been an important support to its share price over the past few months, resulting in a total return of over 31% since my last article on KBC.

Since I haven’t covered KBC for a while, I think now is a good time to analyze its latest financial performance and update its investment case, to see if it still represents a good income pick in the European banking sector for long-term investors.

KBC’s earnings for the first quarter of 2024

During the first quarter of 2024, KBC reported positive operating performance supported by its bancassurance business model, with both its banking and insurance operations performing well in recent months.

The bank was able to report loan growth and deposit growth in the first quarter, a positive result given the strong competition in the market, especially on the deposit side which has come under pressure due to the issuance of retail bonds from the Belgian government.

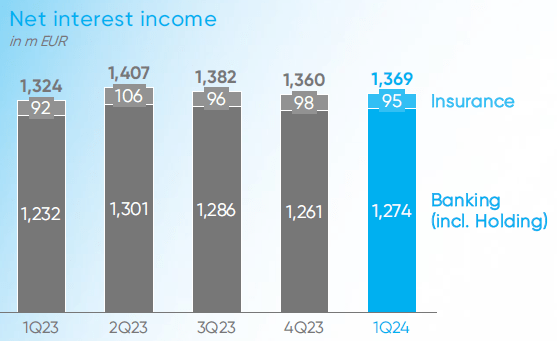

However, KBC was able to report some growth in net interest income (NII), rising by 3% year-on-year to EUR 1.37 billion in the first quarter of 2024, and also slightly above the level reached in the previous quarter.

Net interest income (KBC)

As I have discussed in previous articles on KBC, the bank does not have much exposure to interest rates due to its business model which has a more diversified revenue mix than most of its European peers, resulting in a lower weight of National Insurance on total revenues than most European revenues. Banks and loans in their main markets are mainly at fixed interest rates, so their willingness rates are relatively low.

This explains why despite the rising interest rate environment in Europe over the past couple of years, NRI has been relatively stable, a profile that has not been particularly bullish when interest rates are on an upward trajectory, but is now a positive factor given that interest rates Interest is expected to decrease in the future.

In fact, according to Street estimates, the ECB is expected to cut interest rates several times in the coming months, with the market expecting the key interest rate to fall from its current level of 4.25% to around 2.5% by the end of 2025. The rising interest rate environment has been positive For banks that rely more on National Insurance, e.g PBVA (BBVA) For example, the downward trajectory is expected to put pressure on NII going forward. This means that banks with lower interest rates are expected to have a more stable revenue profile going forward, which bodes well for KBC, at least on a relative basis.

In terms of commission income, KBC recorded a 7% year-on-year increase to €614 million in the previous quarter, supported by higher fees in the asset management segment, which was justified by higher management fees as assets under management increased by 19% year-on-year driven by net. Inflows and positive market performance

In the insurance sector, it also recorded a positive operating performance, with life sales rising 60% year-on-year to €765 million in the quarter. This strong growth is due to the successful launch of a structured fund and commercial work with the private banking sector in Belgium, which led to a strong increase in unit-linked sales in the first quarter of the year.

Regarding operating expenses, excluding bank taxes and insurance, its core costs decreased by 1% year-on-year to €1.06 billion, which is a very good result considering the inflationary environment. While wage growth pressured operating expenses, the sale of its Irish unit had a positive impact on costs.

Another important positive feature of its operational efficiency is KBC’s efforts to digitize and automate customer service, specifically through KIT (the bank’s artificial intelligence assistant). This automated customer service has been well received by its customers, and is currently used by approximately 4.5 million KBC customers. This AI assistant was implemented three years ago and is increasingly accepted by KBC users, enabling the bank to improve productivity.

This AI assistant has a very good track record when it comes to customer questions, as it can answer about two-thirds of the questions independently, as well as by leveraging sales. According to KBC, Kate was responsible for an additional 32,000 sales during the first quarter of 2024, serving as an important tool for the bank to improve its productivity. This is also a great example of how technology and artificial intelligence will impact banking operations, supporting improved efficiency in the coming years.

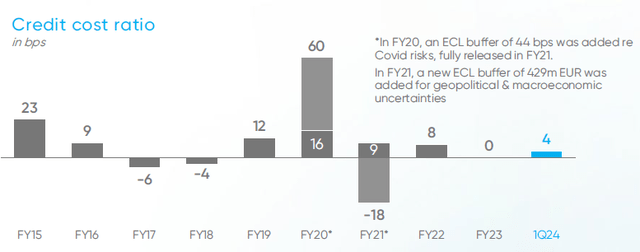

In terms of credit quality, it remained very good given that KBC’s provisions in this quarter amounted to only EUR 16 million (compared to the reversals in Q1 2023), representing a cost-of-risk ratio of only 4 basis points.

Credit costs (KBC)

This is a very low risk ratio compared to other European banks, and while some peers have reported a slight rise in credit costs in recent quarters, KBC maintains very good credit quality. However, its guidance is rather conservative and the bank expects credit costs to increase over the coming quarters to a level of 25-30 basis points, which is still relatively low and, if macroeconomic conditions remain supportive, can be easily overcome in the coming quarters. . .

Its net profit in the first quarter of 2024 was €508 million, relatively unchanged from the same quarter in 2023, and its return on equity (ROE), a key measure of profitability in the banking sector, was 14%. This is a very good level of profitability compared to its peers, demonstrating that KBC has a high quality profile.

In terms of capital position, KBC’s common capital ratio (CET1) stood at 14.9% at the end of last March, which is comfortably above capital requirements and in line with its medium-term target. Since the bank has good organic capital generation, it has set a CET1 ratio of 15% as its target, while excess capital will be returned to equity on a discretionary basis, through special dividends, share buybacks, or a combination of both. .

Indeed, the bank recently decided to distribute surplus capital in excess of 15% through a special dividend to shareholders amounting to €280 million, or €0.70 per share. This was in addition to the interim and final dividends of €4.15 per share already paid, meaning the total dividend relating to the 2023 dividend was €4.85 per share. At its current share price, KBC offers a dividend yield of around 7.30%, which is very attractive to shareholders.

For 2024, its dividend policy remains unchanged, and it expects to pay at least 50% of its annual dividend to shareholders including AT1 coupons, as well as distributing excess capital through special dividends or share buybacks. It expects to pay an interim dividend of 1 euro per share next November, unchanged from the previous interim dividend, while potential dividend growth will be determined in relation to the final dividend when it announces its results for 2024 (during the first quarter of 2025).

The current consensus expects a dividend of €4.62 per share, without considering potential special dividends, so based on the ‘normal’ dividend, the Street expects KBC to increase its dividend by 11% year-on-year, which seems sustainable given the bank’s conservative payout ratio. And good treatment. Organic capital generation.

In terms of its valuation, KBC is currently trading at around 1.2x book value, while its historical average over the past five years is 1.26x book value, meaning its shares appear to be fairly valued at the moment. Compared to some of its closest peers, e.g G Group (ing) or ABN Amr (OTCPK:AAVMY), is trading at a higher price, which is another sign that KBC shares are not undervalued at the moment.

Conclusion

KBC is one of the best banks in Europe due to its strong fundamentals, good asset quality, strong capital position and high dividend yields. While during the high interest rate environment it has not been among the most interest rate oriented banks, in the expected low interest rate cycle before that, the stability of its revenues and profits is a plus, making it a good earner in the European banking sector.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.