com.nkbimages

With my portfolio, I have historically achieved an average market annual return, but with very low volatility of less than 10% per year and a portfolio beta in the 0.7 – 0.8 range. This translates into risk-adjusted outperformance, which can be achieved and explained In many ways. To me, this means at least average market performance with much lower than average risk – and a good measure of this is the Sharpe ratio. One of the reasons for this portfolio’s score is my focus on four pillars: Technology, Healthcare, Entertainment, and Consumer Staples, each of which contributes different factors to the overall score (i.e. growth vs. stability). In this article, I want to walk you through the final pillar by evaluating Keurig Dr Pepper (Nasdaq: KDP) K Possible In addition to my portfolio, which currently contains Coca-Cola (ko) and PepsiCo (Beep). I’m attracted to these types of companies because of their clear business models and their long-term durability and stability. My analysis is organized as follows:

- Anatomy of KDP’s quality segment structure, growth and profitability over time.

- Which shows that despite always being in the shadow of the major players, KDP proves that the industry offers space for multiple quality service providers.

- Assessing the extent to which coffee headwinds, a somewhat weak balance sheet, and weight-loss drugs pose relevant risks.

- I approximate this by comparing KDP’s evaluation criteria with those of industry peers.

KDP is more than just soft drinks

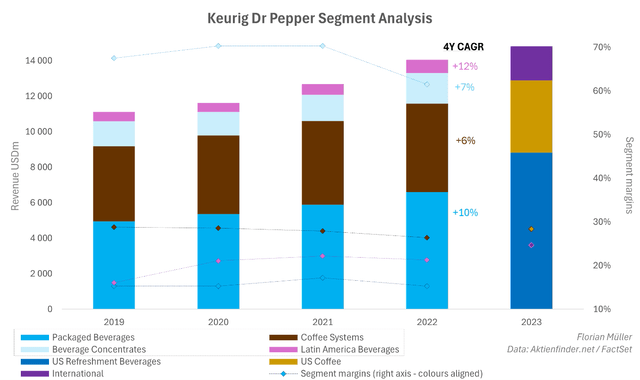

First, I aim to provide a comprehensive historical performance review of the KDP’s most fundamental drivers over the past five years. I hereby refer to my summary The table at the bottom. Over the past five years, the KDP has achieved annual growth of 7%. Given the change in sectors reported in 2023, we will first focus on the years 2019 to 2022. Notably, individual sectors show different margin profiles. For example, the margin from the sale of concentrates and juices was an unusually high 60% to 70%, while the profit margin on bottled beverages was in the mid-teens, on the opposite end of the spectrum. This is also why Coca-Cola’s profit margins were higher, as we will see later, as it increasingly outsourced bottling to franchise operations and focused value creation on juice and product development. The second highest margins, just under 30%, are achieved by the second largest segment, coffee, which had been the slowest growing over the four years prior to 2023. In new segment reports since 2023, it remains clear that KDP is mostly ( 88%) US-focused company, with margins as high as 28% in coffee and soft drinks (which now combine juice and bottled beverages). In summary, KDP projects a fundamentally strong image as a high-quality, medium-growth, highly profitable and diversified beverage company.

Author | Data: Aktienfinder.net/FactSet

A rock in the middle of a competitive industry

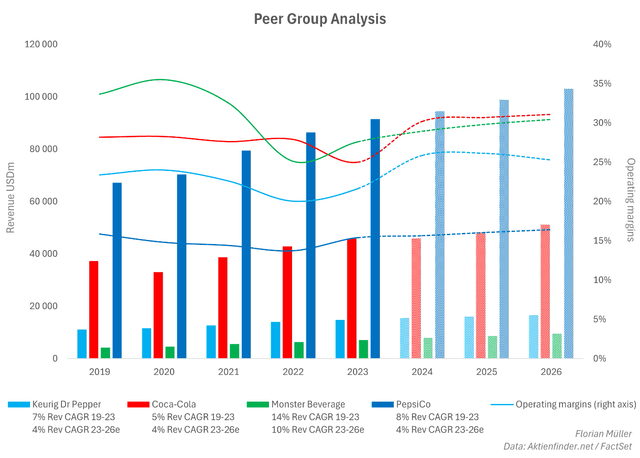

However, it is clear that there are a lot of quality beverage companies out there, some of which are quite powerful. Therefore, I want to put the KDP in perspective with the following peer group analysis. For this reason, I chose industry giants Coca-Cola (the licensor, not a bottler) and Pepsi-Cola, as well as Monster Beverage Company.

PepsiCo is the largest company by revenue, but it also includes a large snack segment alongside beverages. Moreover, PepsiCo’s business model does not rely on outsourcing bottling, which leads to mid-life operating margins that are the lowest among its peers – only half as high as Coca-Cola. Thus, despite doubling revenues, PepsiCo’s earnings and valuation levels are comparable to Coca-Cola. As previously mentioned, Coca-Cola has shifted its business model toward selling richer concentrates to regional bottlers, allowing it to achieve higher operating margins approaching 30%. Monster Beverage operates similarly to Coca-Cola, but is the smallest of the four companies in terms of revenue. However, due to its strong growth, it is still valued higher than Keurig Dr Pepper. Therefore, KDP is a relatively small, but still important player in the beverage market. Its operating margins in the mid-20s are about the peer group average. Likewise, its overall growth, both historical and projected, is comparable to that of larger competitors Coca-Cola and PepsiCo, in the mid-single-digit range. Monster Beverage, on the other hand, has double-digit growth rates.

Author | Data: Aktienfinder.net/FactSet

The KDP can thus assert itself as an important and profitable player in the competitive market, even though it consistently stands in the shadow of the major players. It is quite clear that there is fortunately room for many players. In this context, I would like to quote what Warren Buffett said in 1997, which this analysis shows is still true today:

“Dr. Pepper appeals to a lot of people. It’s interesting how regional tastes can be. I mean Dr. Pepper would have a share in Texas, you know, much higher than it would in Minnesota or something like that but there are people who would prefer that. ( …) You can make money with a soft drink company that doesn’t dominate the business (…). It is not winner take all (…). There are some companies that are winner-takes-all, but soft drinks are not one of them.“

Quality portfolio but risky balance sheet

Additionally, when compared to the major players, it can be easy to overlook how impressive and diverse the brands are behind the underdog KDP. I would just like to provide a brief overview by pointing to the image below. However, a recent concern for KDP has been the large coffee segment with significant revenues and strong margin, which contracted by 2% last quarter due to lower prices, with flat volume development. In the previous quarter, this sector fell by approximately 10%. While this shows at least some improvement, this sector needs to be closely monitored. A strong and relevant competitor in this field is none other than Nestlé, the world’s largest food company, with its coffee sector.

Keurig Dr Pepper

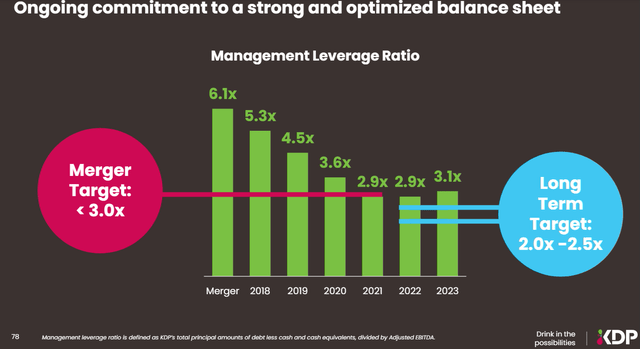

On the more risky side, I would also rank KDP’s balance sheet. The often reported leverage ratio, see below, I find rather interesting. Essentially, it includes net debt to EBITDA, where EBITDA depends on an adjusted variable. In this context, using EBITDA only seems to show half the truth. Next, I would like to provide a clearer picture of the KDP’s balance sheet from my perspective.

Keurig Dr Pepper

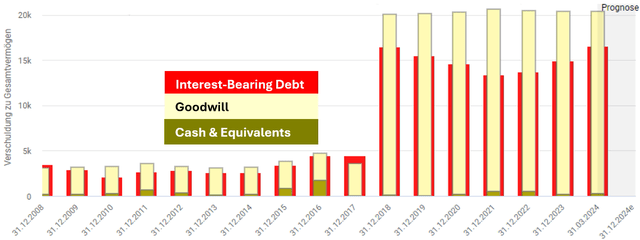

Interest-bearing debt reached record highs. On the one hand, free cash flow conversion has been weak recently. On the other hand, priority was given to dividends, which led to a necessary and continuous increase in debt. In addition, the cash position has always been relatively tight – currently, it’s barely visible in the chart below. Another major risk is very high goodwill, which recently accounted for 39% of total assets, roughly equivalent to the total reported equity of 47% of total capital.

Aktienfinder.net

Another frequently mentioned risk factor is weight loss medications that are currently in vogue. News about these drugs has sometimes caused turmoil in the stock prices of fast food or soft drink giants, due to concerns about changing consumer behavior toward supposedly unhealthy drinks and snacks. However, the CEOs of these companies themselves have remained very relaxed about this, and business numbers so far do not reflect such an impact. From the beginning, I have never feared this influence, and I still hold to this opinion. Furthermore, lifestyle drinks are often low-calorie or no-calorie, and I believe companies are adaptable enough to adjust their branding if necessary.

There are no red flags regarding the evaluation

Finally, I would apply some simplified valuation theories to estimate whether an investment in KDP might be attractive at the present time, having considered it compelling in terms of basis and type while also highlighting significant risks. As a first step, I calculated the cost of equity for the peer group using CAPM. For KDP, I mostly used the Damodaran value relative to the US in determining the country-weighted equity risk premium, while I increased the ERP for Coca-Cola due to their greater exposure to international and emerging markets, and slightly lower for Monster Beverage and PepsiCo to also reflect this . They have less exposure outside the United States. For all companies, a low beta factor is typically observed for this industry. In addition, I made simplified adjustments for alpha risk. For KDP, the fact that the brands, despite their high quality, lag significantly behind Coca-Cola and Pepsi, led me to increase their costs of capital (impairment), while the opposite is true for Coca-Cola and Pepsi – reduce their capital costs (increase the value). . Monster drink, I see in the middle, and therefore I do not allocate it Personal Alpha adjustments risk it.

Author | Data: Seeking Alpha, Damodaran, Aktienfinder.net / FactSet

In conclusion, Coca-Cola and PepsiCo’s stock costs are slightly lower than those of KDP and Monster Beverage. They must now be compared to their actual market valuations and growth dynamics. As a starting point, I use the TTM multiple, the reciprocal of which is the current earnings yield. In the case of KDP, a P/E ratio of 22 equates to a current dividend yield of 4.5%. I then consider the long-term growth dynamics as an average of the historical 5-year CAGR and the expected 3-year earnings CAGR. For example, despite the highest P/E ratio of 33 and therefore low Earnings Yield, Monster Beverage still shows the best P/E+ growth of 14.2% due to its high growth dynamics. This figure must now be compared to the cost of equity. Thus, Monster Beverage stands out as the most interesting overall package to me, with the largest positive deviation of the dividend yield + growth number from the cost of equity, followed by Coca-Cola, reaffirming its position as a core investment in my portfolio. . PepsiCo’s delta is also positive because its high P/E ratio seems justified by its lower costs of capital, and thus it remains strong in my portfolio, although it ranks relatively lower due to less growth dynamics. Keurig Dr Pepper The lower P/E partly reflects higher costs of capital. However, the company is growing at an average rate in the industry, which makes it appear fairly valuable in my view. However, it is not enough to include it in my portfolio. In this case, I favor Monster Beverage as a potential new addition. For KDP, I assign a hold rating with a positive slope.

Concluding remarks

Keurig Dr Pepper offers a well-liked, diverse, and straightforward business model within the industry, albeit in a highly competitive market with strong players. However, the KDP has demonstrated admirably its ability to maintain stability in this environment. Profitability and growth metrics are average within the peer group. However, due to its small size, there seems to be no possibility of catching up above average. Although KDP seems somewhat valuable, in this case I would still prefer to stick with industry leaders like Coca-Cola and Pepsi, as I find Monster Beverage interesting in the smaller space. However, objectively speaking, KDP certainly deserves a positive hold rating.