South_agency

Investment thesis

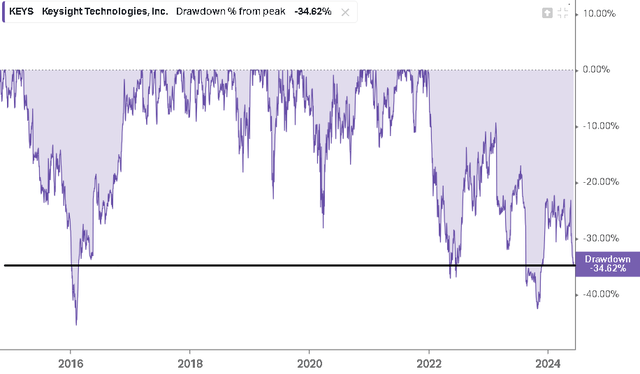

I’ve previously covered Keysight (New York Stock Exchange: Keys) where I talked in more depth about the business model and the underlying quality I think it has. In that article, I decided that the best thing to do was to hang in there for now and Since then, the company has fallen 11% compared to the S&P 500’s 2% rise.

Although this may not seem like a huge decline, the current decline of 33% from the recent peak is one of the largest declines in Keysight’s history, and a larger decline has only occurred 3 times. Given that and adding the fact that the company reported its Q2 2024 results on May 20, I’d like to dive into what’s changed at the company since then.

Drag keys (Quevin)

Second quarter 2024

The summary of the results was that the company exceeded modestly Expectations, but given that we are currently in a very negative economic environment for the company, exceeding the guidance that management itself provided a quarter ago is noteworthy.

Given Q1 core orders of $1.14 billion, we expect Q2 revenue to range from $1.190 billion to $1.210 billion, and Q2 earnings per share to range from $1.34 to $1.40.

CFO Neil Dougherty during the first quarter 2024 earnings call

The not-so-positive aspect that made the market so cautious with Keysight is that during Q2 2024 revenues were down 12.5% (even taking into account beating expectations) and that initial guidance for Q3 would mean a decline of about 14%, so no one should be surprised. If this fiscal year ends with a double-digit decline in sales.

| appreciation | actual | Win/Miss | |

| he won | $1.20 billion | $1.22 billion | 1.0% |

|---|---|---|---|

| EBITDA | $327 million | $332 million | 1.4% |

| Earnings per share | $1.39 | $1.41 | 1.6% |

Author’s compilation

We expect third-quarter revenue to range from $1,180 billion to $1,200 billion and third-quarter earnings per share to range from $1.30 to $1.36 based on a weighted diluted share count of approximately 175 million shares.

CFO Neil Dougherty during the second quarter 2024 earnings call

| Fiscal year 2023 | Fiscal year 2024 | Change revenue | |

|---|---|---|---|

| Q1 | $1,381 | $1,259 | -8.8% |

| Q2 | $1,390 | $1,216 | -12.5% |

| Q3 | $1,382 | $1,190 | -13.9% |

| Q4 | $1,311 | ? | ? |

Author’s compilation

One thing worth clarifying is that this problem is not unique to the company and does not appear to be caused by loss of market share or competitive advantages. To illustrate what I mean, I made this comparison table with companies similar to Keysight but of different sizes.

We can quickly see that Keysight isn’t the only one facing problems this year, both in growth and margins. Smaller companies, such as Calnex Solutions, posted a sharp 40% decline this year. So, although no one wants their company to reduce its revenues by 10%, it can at least be considered that this is due to a general impact on the industry derived from the fact that the customers of these companies (semiconductor companies, telecommunications companies, among others ) ) They also feel dissatisfied with the high interest rate environment and thus postpone their capital expenditure investments.

Author’s compilation

evaluation

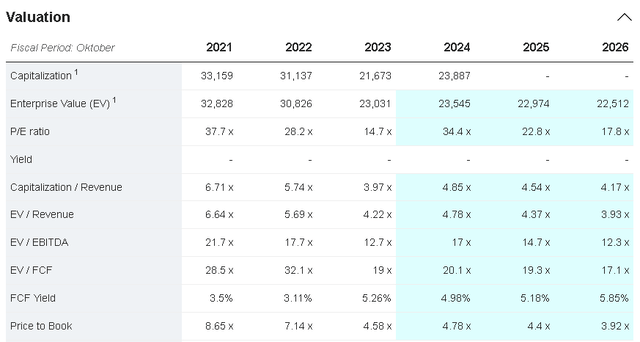

Keysight is currently trading at a P/E of 34 if we use 2024 earnings as a reference. This doesn’t sound cheap, but the reason is that this year margins are expected to compress and income decline, as evidenced by net margin, which has risen from 19% in 2023 to 15% in the past 12 months.

There is expected to be a recovery in 2025, which we can already start to see in sectors such as semiconductors, and then the P/E will rise from 34 to 23 thanks to a recovery in profit margins.

In semiconductors, the industry outlook is improving with expectations for a recovery in 2025. Inventories are falling to healthier levels and demand is increasing in certain areas such as high-bandwidth memory.

CEO Satish Dhanasekaran during the second quarter 2024 earnings call

Market examiner

I estimate that free cash flow this year will suffer a larger decline than revenue this year, but this low comparable base would cause free cash flow/share growth to be larger than in years past, in my estimate, 12%. Annually, which would be somewhat higher than the 10% per year it provided between 2014 and 2023. At this estimate, Keysight would earn approximately $12 per share in 2030 and would represent a 12% return if bought at the current price.

Evaluation form (author’s compilation)

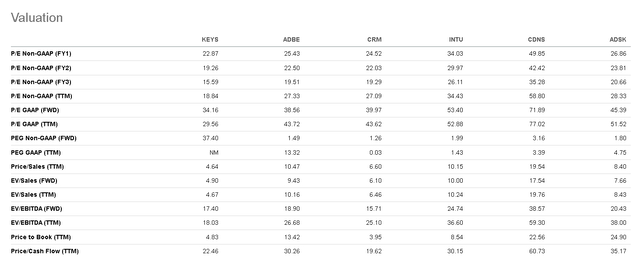

I chose a free cash flow multiple of 25x based on what can be seen in other software companies. It’s not a dirt cheap ratio, but it’s hard to find a software company that trades at less than 20 times, unless it’s displaying structural issues or something that merits a low valuation.

Evaluation ratios (Searching for Alpha)

Bottom line

As I mentioned throughout the article, I don’t think Keysight has problems that will affect its future. It is not losing market share and the economic slowdown should be temporary, since its services are essential to customers. So, now that the valuation is better than it was a few months ago, I’m finally interested in buying.

The biggest risk is that the company takes advantage of operating leverage and keeps its costs fixed. This is positive in a growth scenario, but causes earnings to fall more than revenues in a contraction, which could cause it to issue debt to fund itself and could cause the estimate to decline in free cash flow. In this case, the stock will probably remain flat for longer than expected, but I think if your time horizon is longer than two years, the stock should do well as an investment.