Luis Alvarez

I have added strongly to my position in Kimco Real Estate Company (New York Stock Exchange: KEM) Last week the stock went through a brief period of unearned selling weakness.

Kimco Realty benefited from strong leasing activity in the first quarter It continues to display very healthy payout metrics in relation to REIT earnings.

Kimco Realty’s low payout variance and favorable lease spreads make the trust a compelling buy from both a cash flow and earnings growth angle.

My evaluation history

Kimco Realty’s net operating income growth and strong FFO were good reasons I recommended the mall-focused real estate investment trust to passive income investors a few months ago.

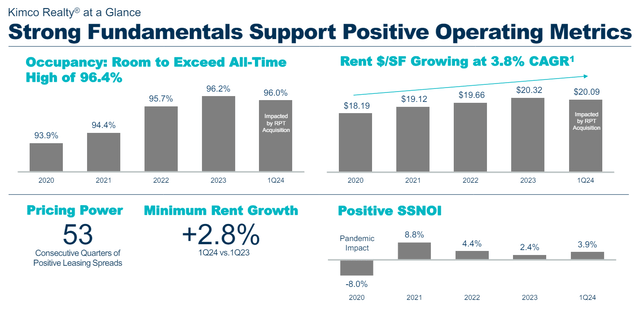

Kimco Realty continued to profit from strong leasing activity (higher rents, higher net operating income on a same-store basis, higher spreads) in the first quarter and first quarter of the year. The outlook is positive here, and Kimco Realty also felt comfortable enough to raise its forecast for funds from operations by 2 cents per share.

Portfolio review

Kimco Realty primarily owns shopping center properties leased to grocery-focused retail chains such as Aldi, Trader’s Joe’s, CostCo and WholeFoods. Shopping mall-focused REITs benefit from healthy fundamentals in their category. Same-store net operating income accelerated from 2.4% in 2023 to 3.9% in the first quarter of 2024 amid a strong release of demand for Kimco Realty’s shopping center space.

Strong fundamentals (Kimco Properties)

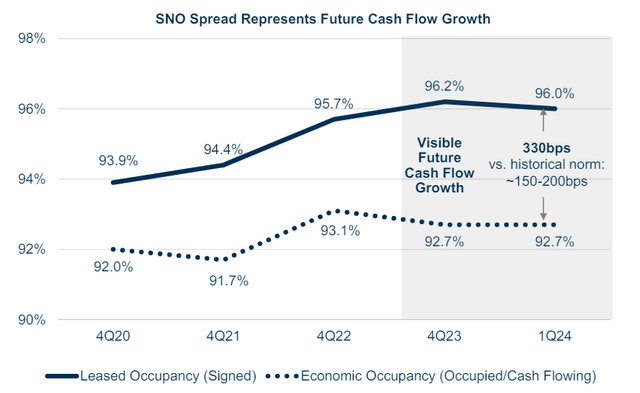

Kimco Realty primarily benefits from its ability to raise rents on its tenants in its shopping centers. The leasing spread, which currently stands at 330 basis points above current occupancy, indicates the fund’s ability to increase its market rents by releasing space to lease shopping centers. In simple terms: releasing spreads captures the increased upside in cash flow once properties are released to the next tenant.

The positive rental spreads that Kimco Realty is currently seeing in the market reflect good demand for mall space. The leases that have already been signed, but have not yet begun paying, as of the first quarter of 2024, reflect a $63 million increase in the fund’s annual base rent.

Future cash flow growth (Kimco Properties)

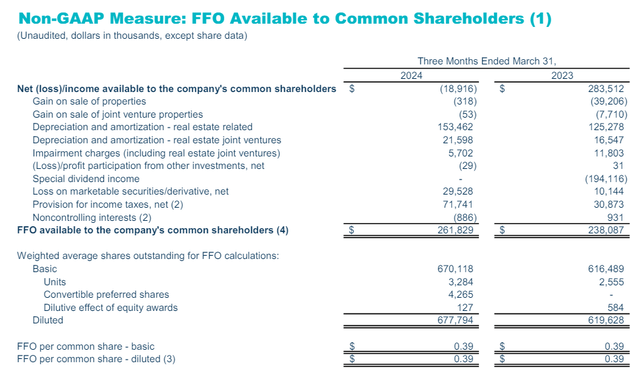

One criterion for the success of REITs is their ability to convert rental income into distributable funds from operations. In the first quarter of 2024, Kimco Realty generated $261.8 million in funds from operations, up 10% year over year thanks to tailwinds associated with higher new lease rates as well as increased net operating income for existing stores.

In 2024 and 2025, if interest rates start to fall, I could see increased interest in acquisitions, which in turn could be a driver of funds from operations growth in subsequent quarters.

Considering that the dividend is well covered and that spreads look strong, I think Kimco Realty’s dividend value, as well as its dividend potential, is great.

Non-GAAP financial measures (Kimco Properties)

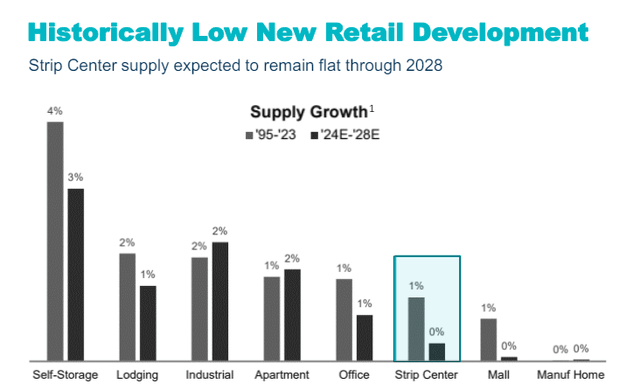

Favorable supply dynamics can support NOI/rent per square foot growth

The industry is not currently investing a lot of capital in developing outdoor malls, which creates a positive outlook for the owners of these properties. This is partly due to changing shopping trends as more people buy products from e-commerce sites like Amazon. Since Kimco Realty’s malls are predominantly grocery store-based, the outlook for same-store net operating income growth is very favorable. Another reason is that the coronavirus has negatively affected the construction of new malls amid uncertainty during the pandemic. All of these trends have led to a situation where there is no measurable growth in the central supply of the strip, which in turn should pressure rents and lead to sustained rent per square foot growth in the next couple of years for Kimco Realty. With both NOI and rent per square foot already growing, I expect continued tailwinds to these two key metrics, and perhaps even an improvement in the trust’s long-term occupancy rate.

Supply growth (Kimco Properties)

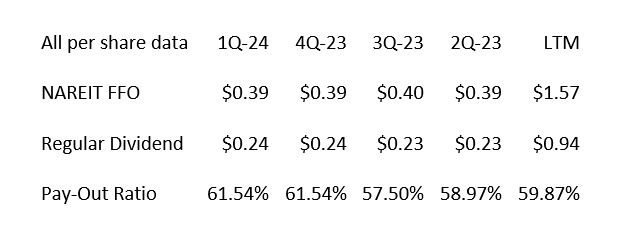

Dividend coverage remains intact, despite the dividend increase

Kimco Realty raised its dividend to $0.24 per share in the fourth quarter and has maintained very good dividend metrics since then. Its dividend payout ratio in the first quarter was just 62%, the same as in the previous quarter, meaning Kimco Realty generates more than enough cash from operations on a recurring basis to afford its dividend.

This low payout ratio, which I consider to be a fundamental strength of Kimco Realty’s investment proposition, gives the REIT a great deal of freedom to invest excess cash in new property acquisitions, development projects or other strategic initiatives.

In the last twelve months, Kimco Realty paid out just under 60% of its money from operations. The dividend payout ratio calculated based on Kimco Realty’s 2024 FFO projections indicates a payout ratio of 61%. I believe the very low volatility of the trust’s payout ratio is what provides so much value to risk-averse passive income investors who value low-risk profits more than anything else.

Dividend (The author created a table using trust information)

Kimco Realty and multiple FFO guidelines

Kimco Realty raised its forecast for 2024 funds from operations from a range of $1.54-1.58 to $1.56-1.60 per share amid strong leasing activity in its portfolio. The range translates into money from multiple operations, at the current share price of $19.36, or 12.3x. I think the multiple is a compelling reason to add the stock to a passive income portfolio, especially considering the trust’s low FFO payout ratio, which translates to a high margin of dividend safety.

Realty Income, which I often consider a standard bearer for quality in the real estate investment trust sector, paid out 75% of its money from operations in the first quarter meaning Kimco Realty offers better covered dividends to passive income investors. However, Realty Income shares are selling for 12.5 times money from operations.

Although Realty Income is more focused on retail properties and Kimco Realty on malls, I believe the quality of Kimco Realty’s earnings and cash generated from operations is undervalued in the market.

Why your investment thesis might be wrong

Just because a REIT is performing well currently, doesn’t mean it always will. Potential headwinds for Kimco Realty relate to the fund’s concentrated strategic exposure to shopping malls. For example, the 2020 pandemic exposed some previously unrecognized vulnerabilities in the mall REIT model in times of pandemics.

deductive

Kimco Realty is benefiting from strong leasing activity, upward momentum in leasing spreads, as well as moderate mid-single-digit growth in same-store net operating income.

These trends are positive and are mainly supported by mall REIT funds from operations and a lower dividend payout ratio.

Kimco Realty has cut its dividend during the pandemic, but the fact that the shopping fund has been consistently increasing its dividend since the end of 2020 is encouraging and bodes well for passive income investors who value confidence focused on returning excess cash flow to shareholders.

The stock is reasonably cheap and the dividend is quite safe, so I’m willing to double down on Kimco Realty shares every time the price drops.