Pennsylvania7/iStock Editorial via Getty Images

Connie Aweg ( OTCPK:KNYJF , OTCPK:KNYJY ) has a significant amount of exposure in China. New orders down there. Otherwise, new orders in other markets have increased, which is crucial for KONE blades and blades Models, maintenance and service revenues were strong and provided some margin. The cost-cutting programs that Cooney discussed in the last call and Our latest article It also helps a little bit to lift EBITDA on a year-over-year basis. The business is highly flexible, essentially bond-like, but the valuation reflects that.

First quarter earnings

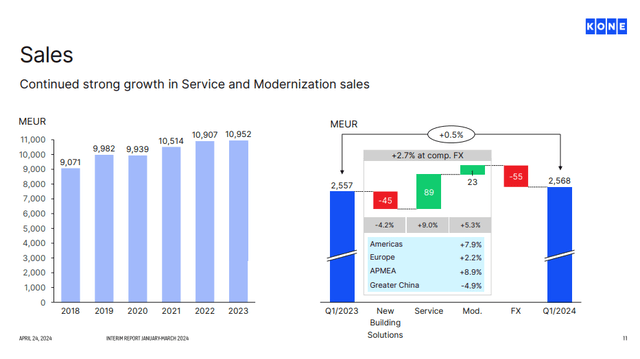

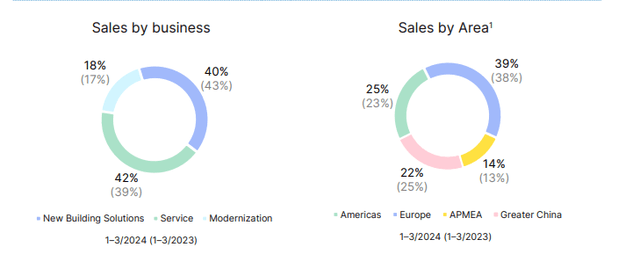

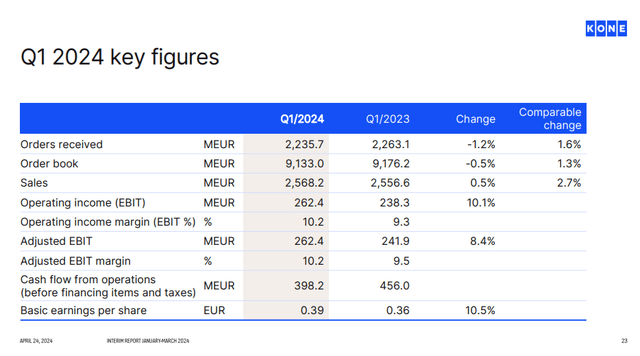

Orders decreased on a core basis by 1.2%, but increased by approximately 1.6% on a constant currency (cc) basis. The reason for this was the lack of demand activity for new equipment from China and Europe as well, which was already evident in the current results and in line with market expectations. The operating environment is there. Overall sales increased 2.7% in terms of CCbut new construction solutions were down about 4.2% on a cc basis, with recurring service business up 9% cc.

Upgrade was up 5.3% cc, and overall Chinese sales were down about 4.9% cc due to weak development markets there, with upgrade and service growing well. However, the loss of volume actually meant a lot of price competition, which further impacted the sector’s performance and unit economics on new equipment, as all the elevator companies have a large Chinese presence and significant volume there. Large projects have been the problem, and orders in China are poor for new builds but good for modernization.

Asia Pacific, Middle East and Africa Americas prices were up about 8-9% on a CC basis, and in Europe they were up just 2%, consistent with lower new equipment orders but offsetting growth in upgrades. The Americas were more interested in new construction solutions than modernization and service, skewing towards new mega projects. Prices were good, US orders were good, so geography should improve. Market share is being won because the operating environment has been weak in the US due to high interest rates.

In Europe, the tepid results are consistent with a weak new construction solutions demand environment, in line with the weak operating environment in many of Kone’s markets, including the Nordics and Western Europe. Newbuild sales were already declining and impacting European sales figures, but margin was supported by strong performance in higher margin repeat business.

Service in most geographies rose by significant amounts, offsetting this pressure and also contributing to a significant positive mix effect responsible for most of the margin gains year over year.

sales (View Q1)

There was about 100 basis points in EBIT margin, hence strong growth of 10% in the absence of significant growth in headline sales. This was due to strong pricing in the US environment and of course a combination of effects from more repeat business in the mix from Europe and China, whose new equipment markets led to the declines. There was some cost inflation, particularly in labor, which is important because this is a service-intensive business, but the cost improvements offset those impacts and allowed the mix effects to contribute to EBITDA on a year-over-year basis. Mix effects also offset pricing pressure in China that exacerbated the volume and pricing of new equipment.

Lineage (First quarter PR) the address is (View Q1)

minimum

Chinese exposure is really important in my universe. Receivables are also large on the balance sheet, with 88 days outstanding, and receivables are just under 10% of total assets. The Chinese real estate market is going through a deleveraging phase, so the risk of bad debt rates rising in China is not insignificant. This may have some impact on the company’s total asset value, and certainly on cash flow such as the income statement.

However, the business model for razors and blades and its resilience is emerging again despite some major issues in key markets such as China as well as a weaker economic environment in Europe. The forward P/E is around 25x. Margin leverage from the mix effects of recurring business is critical, and results in a counter-cyclical profile for Kone that makes its dividend almost bond-like, with additional growth prospects. The dividend yield is consistent with a fixed income strategy with similar risks. Connie’s assessment is probably fair on an absolute basis.

On a relative basis (for whatever it’s worth), it looks like Kone will be a discount to Schindler (OTC:SHLRF) and Otis (OTIS), depending on which forecast you use. Surely there is at least a 10% discount in the evaluation from Schindler. However, this could be explained by the fact that Schindler has a much smaller Chinese exposure (less than half that of Otis and Kone) – so there is no value case there either.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.