Spiderstock

LAM Research (Nasdaq:LRCX) is the leader in drilling equipment with a share of more than 40% in 2023 according to the Information Network report titled “Global Semiconductor Equipment: Markets, Market Shares and Market Forecast”.

Plasma etching is a crucial process in… The memory market, especially in NAND processing where the number of layers exceeds 200. Fortunately, the memory market is recovering from a difficult 2023 due to the increased supply of chips for computers and smartphones:

- NAND billings in April were +108% YoY, while service provider rates were +29% MoM and +84% YoY.

- DRAM billings were +75% YoY, while service provider rates were -3% MoM but +41% YoY.

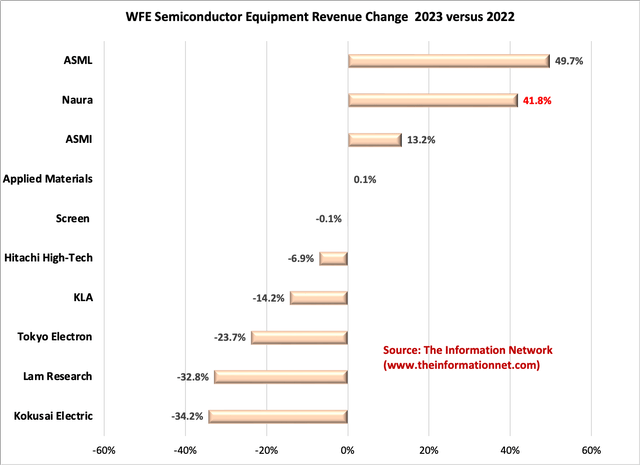

Lam Research’s 2023 revenue performance was significantly lower than its U.S. peers, resulting in year-over-year growth of -32.8%, as shown in Chart 1. Japan’s Kokusai Electric is the only major equipment supplier to perform worse. ASML (ASML) achieved growth of 49.7% year-on-year and Obtained the first position in the WFE market in 2023, overtaking applied materials (deaden).

Japan’s Tokyo Electron ( OTCPK:TOELY ) is Lam’s main competitor in the drilling sector, but its year-on-year growth for 2023 was also negative at 23.7%, which is slightly better than Lam’s.

More importantly, Chinese company Naura, a strong competitor in drilling systems, achieved 41.8% growth in 2023, indicating that US sanctions against China are not preventing domestic equipment suppliers from strong growth, according to the information network report entitled Semiconductor and Equipment Markets in Mainland China: Analysis and Manufacturing Trends.

Information Network

Chart 1

2024 is shaping up differently

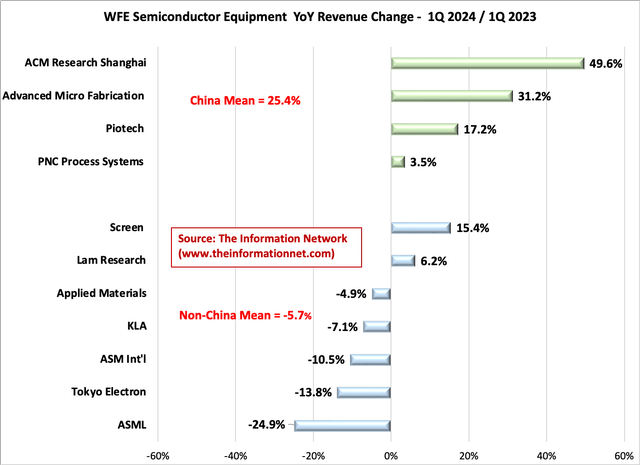

Chart 2 shows the year-on-year growth of Q1 2024 data for Chinese equipment suppliers and non-domestic competitors. ACM Research Shanghai achieved 49.6% growth compared to the first quarter of 2023. In fact, the average growth of Chinese companies grew by 25.4% year-on-year.

Non-Chinese companies continued to perform poorly, with average annual growth reaching 5.7%. More importantly for this article, Lam Research posted growth of 6.2%, better than drilling majors Applied Materials, -4.9%, and Tokyo Electron (“TEL”), -13.8%.

Information Network

Chart 2

China’s AMEC is another strong competitor in the drilling space, and capacitively coupled plasma (“CCP”) and inductively coupled plasma (“ICP”) contribute about 75% of the company’s total revenue. The company’s share of the domestic market for CCP equipment is expected to reach 60% in the next few years, a significant rise from 25% at the end of 2022.

Meanwhile, in the first quarter of 2024, Naura achieved revenue of 5.859 billion yuan, a year-on-year increase of 51.36%.

For 2024, I expect 15% industry-wide growth in bit production for NAND, driven by continued tight supply conditions for both NAND and DRAM. My forecast maintains a conservative stance on supply growth.

Overall, wafer front-end equipment (WFE) purchases are critical to memory equipment purchases, specifically NAND, and I estimate that NAND WFE will increase 9% in 2024 to $9 billion.

I also expect an increase in WFE spending on the DRAM segment, growing 11% to $22 billion in 2024, supported by increased demand for high-bandwidth memory (“HBM”).

LAM Research in 2025

According to the previously mentioned report on Global Semiconductor Equipment from Information Network, Lam Research’s etching revenue declined 33% year over year in 2023, primarily due to its higher exposure to NAND memory.

It is also important to note that drilling revenues are down for other drilling companies, especially TEL. But drilling revenues increased for Chinese companies AMEC and Naura, which increased significantly.

Information Network

Lam will face additional headwinds from Japan’s TEL in the “cryo etch” area, which the company will introduce in 2025.

According to TEL, the drilling process:

- Etching depth of 10 microns was achieved

- 2.5 times faster drilling rate than previous technologies

- Reducing global warming potential by 84%

This innovative drilling technology, which operates at -70sC is capable of producing hole-punch memory channels in advanced 3D NAND devices with an array of more than 400 layers, and TEL will deliver the equipment in 2025.

According to TheElec, SK Hynix is performance testing Tokyo Electron’s cryogenic etching equipment, with the aim of applying the equipment to NANDs with 400 layers and above.

Lam currently holds a 100% share of the NAND channel etching equipment market, according to Nikkei Asia. However, according to Tim Archer, CEO of Lam:

“In etching, Lam uses high aspect ratio cryogenic etching to enhance memory hole formation productivity. Today, we are approaching 1,000 Cryo Etch chambers in our installed manufacturing base at high volume.”

Investor takeaways

Over the course of the past year, LRCX has been impacted by sanctions on its products in China, a severe downturn in memory, the bulwark of its traditional business, stronger revenue growth than its main US competitor AMAT, and increasingly strong growth from Chinese equipment suppliers. .

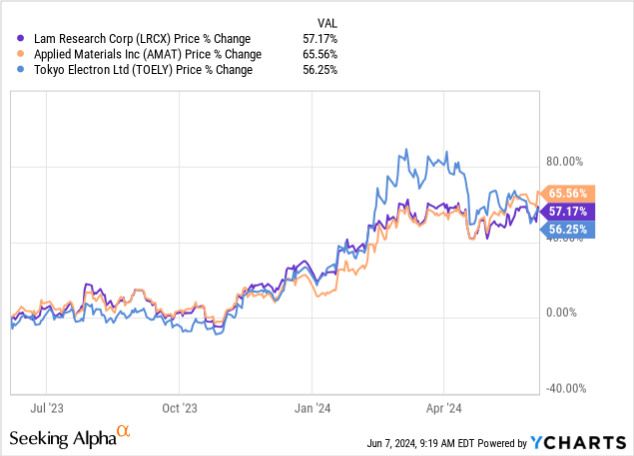

However, according to Chart 3, Lam’s one-year stock price is up 57.17%, while AMAT’s stock price is up 65.56%, and TEL’s is up 56.25% year-on-year.

YCharts

Chart 3

In 2025, I expect WFE equipment spending on NAND and advanced logic/foundry to fully recover. A strong driver of the WFE market will be the growth in the AI server market, which is witnessing an annual growth rate of 31%. AI servers are expected to grow by 32% year-on-year; Personal computers are expected to grow by 14%, and smartphones are expected to grow by 15% on an annual basis until 2025.

Importantly, AI processor chips, especially GPUs from Nvidia (NVDA) require memory, specialized packaging such as HBM (High Bandwidth Memory) and CoWoS packages made by Taiwan Semiconductor Corporation (TSM) to operate at peak performance.

These factors are expected to push the wafer fabrication equipment (WFE) market to achieve double-digit growth in 2025.

Based on a strong recovery in memory in 2024, I rate LRCX a Buy. Investors need to be cautious going into 2025 based on the continued strength of Chinese companies selling in China and from TEL’s cryogenic drilling equipment.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.