Sezeryadigar/iStock via Getty Images

LEG Stock: The Dividend King Cuts Its Dividend

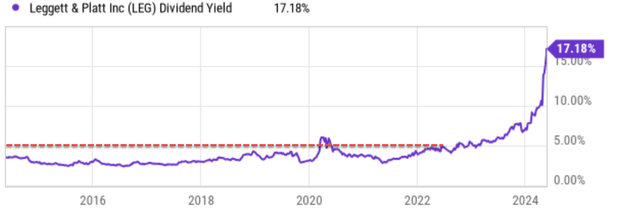

Leggett & Platt Company (New York Stock Exchange: Leg) came to my attention in early 2022 during my routine screening of dividend stocks. In these screens, I specifically look for stocks that… It pays regular dividends and its yield is either significantly higher or lower than its historical average yield. LEG’s yield was around 5% at the time as shown in the following chart, near at least a 10-year high (excluding the sell-off period during the coronavirus outbreak). Leggett was a dividend king having raised his dividend for 51 consecutive years (at the time).

So, when I saw that the Dividend King yield was outside the historical range, I just had to dig in and find out why. Experience has taught me that the first place to dig is… Safety of profits. In hindsight, I’m glad I learned that lesson and applied it. Last month, the stock made a dramatic announcement Cut profits From $0.46 per quarter to $0.05. Share prices have fallen from around $40 in 2022 when they showed up in my scan to the current price of around $10.

Against this background, the thesis of this article is twofold. First, I would like to share with you the notes I took at the time in the hope that they will help other dividend investors avoid potential pitfalls. Secondly, I would like to provide my forecast for the stock in the future. In short, I continue to see significant headwinds in profitability going forward, which are further exacerbated by inventory accumulation and future balance sheet risks.

Seeking alpha

Dividend lesson: Don’t just look at payout ratios

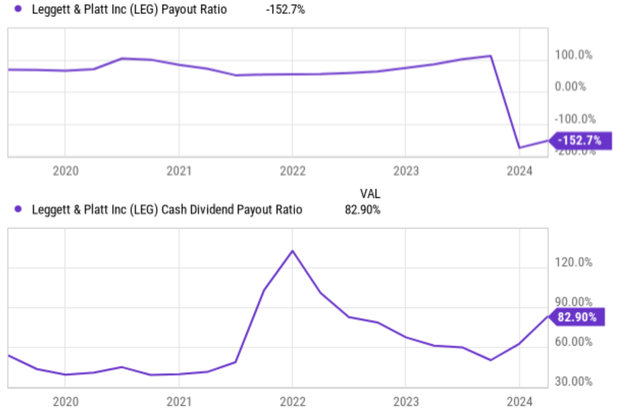

I’m sure payout ratios are among the first things all dividend investors check. Looking back to 2022, LEG’s payout ratios are showing some worrying signs, but really nothing as worrying as shown in the chart below. Its dividend payout ratio was just under 100%, which is close (actually slightly better) than the average level in previous years. Many companies maintain profits of up to 100% for many years. Its cash payout ratio soared to over 100% in the wake of the coronavirus outbreak (which is completely understandable) and was showing signs of normalizing in early 2022 as we saw.

Seeking alpha

However, the main lesson we learned: Don’t stop at payout ratios. As described in a previous article on dividend payout ratios, payout ratios have several limitations:

- The simple payout ratio ignores the current assets that a company has on its balance sheet. Obviously, for two companies with the same earning power, the one with more cash on its balance sheet should have a higher level of earnings security.

- The simple payout ratio also ignores upcoming financial obligations. Again, it is clear that for two companies with the same earning capacity, the one with a lower level of liabilities (pensions, debt, capital expenditures, etc.) should have a higher level of earnings security.

Thus, I have been reminding my readers whenever I have the opportunity to look beyond these simple return ratios through other metrics such as the protection ratio. For readers who don’t really want to put in the effort, at least take a look at credit ratings. In the case of LEG, its credit rating (see sample report from Fitch Ratings below) was already showing red flags at the time. For example, in June 2022, its ratings were affirmed at BBB, but the outlook was revised from stable to negative. The negative outlook was then confirmed again in September 2022. Finally, the credit rating was downgraded in August 2023 to BBB-.

Fitch Ratings

LEG Stock: Earnings Forecast

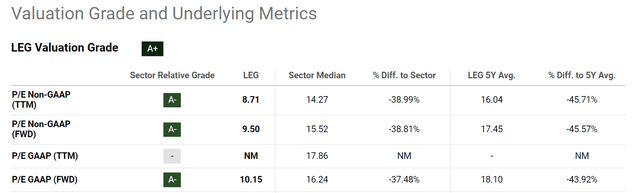

Now, with falling stock prices and dividend cuts, many potential investors may believe the worst has already happened – with good reason. For one thing, the stock is now trading at a very attractive valuation multiple, as seen in its valuation scores. The P/E multiples are close to the bottom bargain positions, both in absolute and relative terms. In absolute terms, LEG’s P/E ratio is just in the single digits (about 8.7x on a TTM basis). In relative terms, P/E ratios are now at a discount of about 40% from the sector average. LEG has historically traded at a premium compared to the sector (the average P/E in the past 10 years has been around 18x).

Seeking alpha

However, I would suggest against attempts at bottom fishing. I see several strong headwinds ahead, which will likely drag down its earnings. As such, FWD rating multiples can be much more expensive than the numbers above indicate. First, I expect the ongoing lackluster bedding markets to continue due to weakness in the residential market. It goes without saying for most investors that high borrowing rates (and also high inflation) tend to make people more reluctant to buy new homes. But my experience is that it also makes current homeowners more hesitant to sell their current home. I’m really speaking from my current experience – I have to think twice if I want to give up my current 2.5% mortgage rate and get a much higher rate.

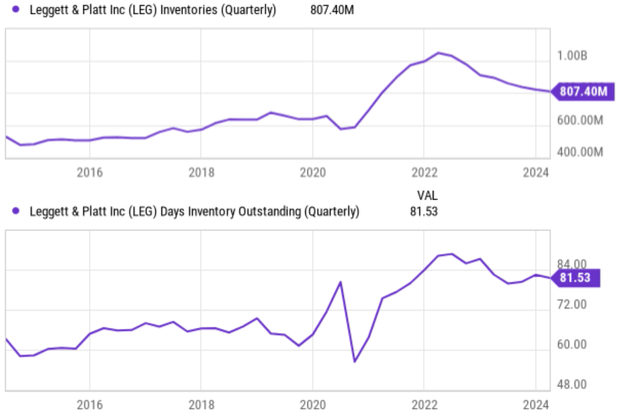

Second, LEG’s current inventory exacerbates the problem here. As shown in the chart below, its stock is around $807 million, which is well above the historical normal range. In terms of days of inventory outstanding, the level is currently 82 days, near the highest level in at least 10 years. Holding such a large inventory adds significant operating costs (warehousing, insurance, etc.), restricts cash, and increases balance sheet risk.

Seeking alpha

Speaking of balance sheet risk, the company’s balance sheet is becoming more stretched. The following chart shows LEG’s operating income and liabilities in the last few quarters. As we’ve seen, the good news is that the company has started deleveraging seriously over the last year or so. Long-term debt reached a peak of $2.1 billion in the September 2022 quarter and has fallen to the current $1.7 billion level. However, the $1.7 billion debt is still at the same level as it was in September 2021 as we saw. However, the company’s current operating income is only a fraction ($55 million last quarter) of its 2021 level.

Seeking alpha

Other risks and final thoughts

In terms of upside risks, the company has other revenue sources besides the residential markets. For example, its sales could benefit from higher demand in the automotive and industrial sectors to partially offset the headwinds mentioned above. Furthermore, raw material prices are highly volatile and can fluctuate in the direction in favor of LEG. Looking further, improvements in profitability are a possibility given the significant restructuring plan the company is implementing. The company plans to move production across bedding supplies, interior furniture manufacturing, flooring and other businesses. This plan involved moving production from smaller facilities to larger facilities, while dropping some production lines that were less favored by the market.

It’s very likely that these moves will eventually lead to margin and EPS improvements down the road. However, in the near term (say next year or two), these reconstruction efforts will very likely result in higher costs and lower profits.

I repeat that my goal in this article is twofold. First, I want to use LEG to illustrate some lessons I’ve learned as a dividend investor. When you see an unusually high yield, your first reaction should be caution, as this often indicates the risk of unsustainable payouts such as the LEG case. When analyzing the health of a dividend, don’t stop at a simple payout ratio and consider a company’s financials more comprehensively. Secondly, I want to caution against attempts at bottom fishing here. Despite the low prices and significant valuation discounts, I see signs of a value trap in Leggett & Platt, Incorporated stock given the EPS headwinds I anticipate.