Richard Drury

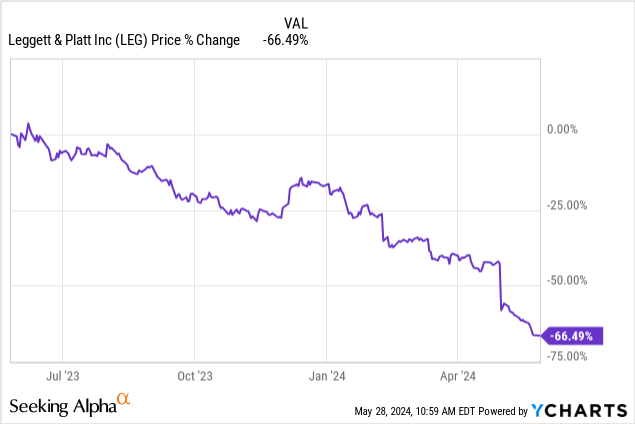

Leggett & Platt, Incorporated (New York Stock Exchange: Leg) designs, manufactures and sells engineering components and products in the United States and internationally. A company we praised for its commitment to returning value to its shareholders through dividends for more than half a year century, recently Cut its profits to $0.05 from $0.46 previously, resulting in a sharp decline in stock prices.

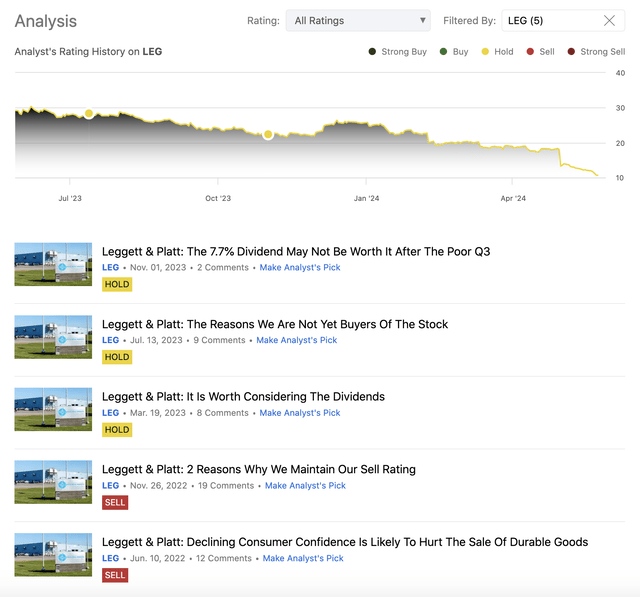

We initiated coverage of the company in June 2022, with an initial sell rating, citing weak consumer sentiment and expectations of weak financial performance. Later, in November 2022, we reiterated this bearish rating, again citing macroeconomic headwinds, coupled with lower sales and profit margins. In March 2023, we became somewhat more optimistic, as we evaluated the company’s shares using a multi-stage dividend discount model, which suggests that the company’s shares Fairly valuable. A range of conventional price multiples supported this view, and we upgraded our rating to ‘hold’, which we have repeated twice since. Once in July 2023 And once in November 2023.

Analysis history (author)

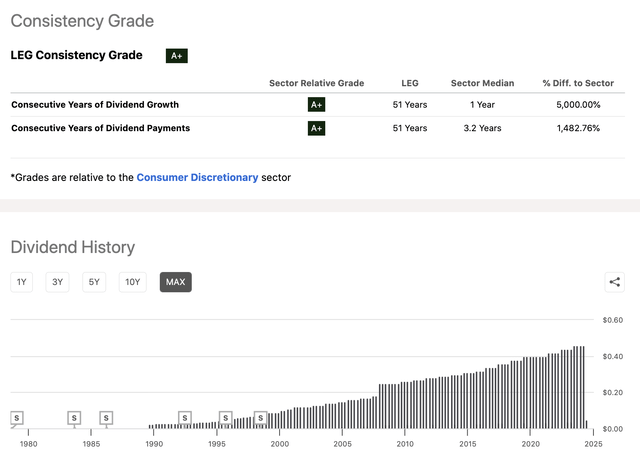

Because the dividend has been almost completely reduced, our ‘hold’ rating based on the assumption of a forever increasing dividend – which was our input to the dividend discount model – is no longer valid.

Dividend History (SA)

The goal of our writing today is to provide an updated view on the company, including a brief explanation of why the dividend was cut, an updated look at the macroeconomic environment, including consumer confidence and the housing market, and last but not least we’ll take another look at a set of traditional price multiples to measure a company’s value. And also discuss why the dividend discount model we used before is unlikely to be very useful anymore.

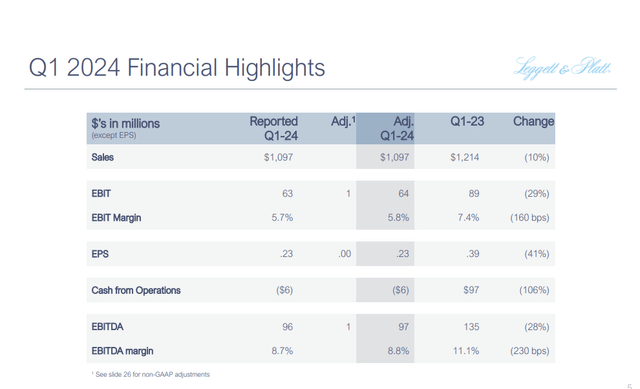

Quarterly results

The company announced its quarterly earnings results on April 30. There was nothing really exciting about the numbers shown. Sales fell to $1.1 billion in the first quarter, representing a 10% decline year over year. Earnings per share fell to $0.23 from $0.39 a year earlier. It left its 2024 guidance unchanged, and continues to expect a significant decline in both sales and earnings per share for the full year.

Highlights (LEG)

So let’s break these numbers down a bit to understand what drives this poor performance.

he won

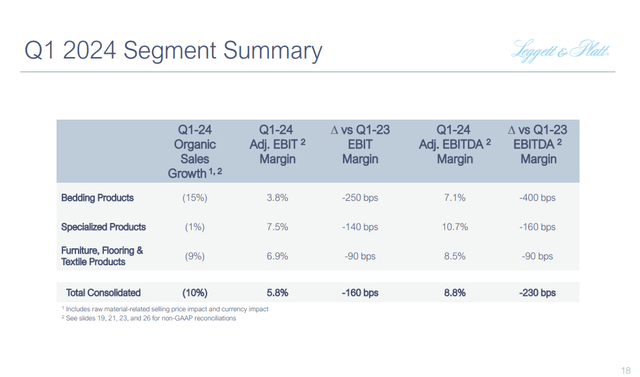

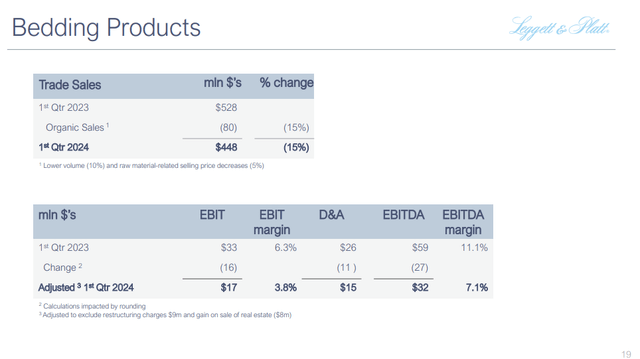

The decrease in sales was due to lower volume as well as lower selling prices associated with raw materials. The decline in volume is a clear indication that demand for LEG’s products is deteriorating, despite lower selling prices related to raw materials. However, we believe this trend can largely be explained by broader economic sentiment and is not necessarily a result of company-specific issues. It is also important to highlight that all segments performed poorly and had negative organic sales growth, but the Bedding Products segment was the worst of all with sales declining by 15%.

Sector Summary (LEG)

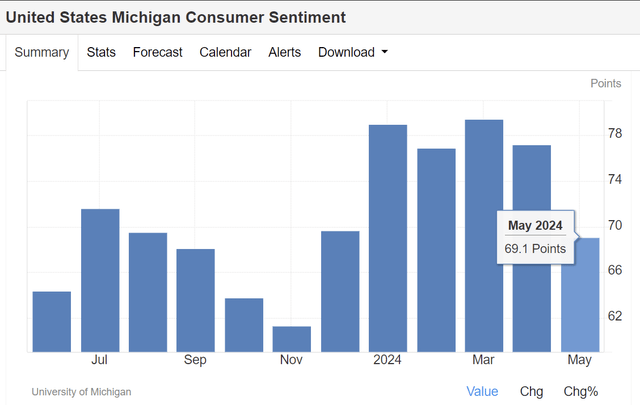

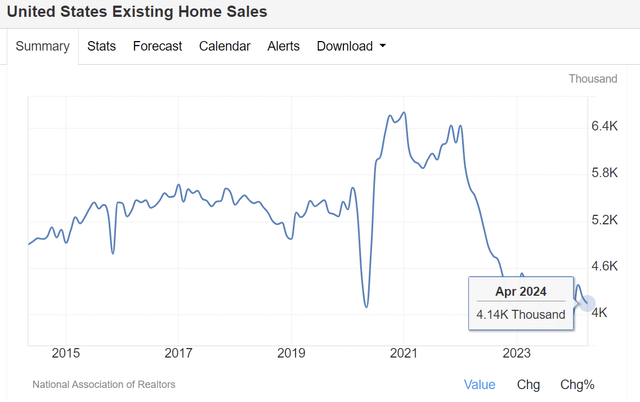

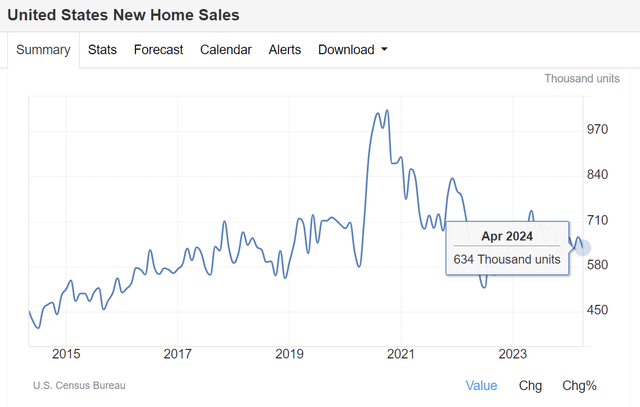

US consumer confidence has remained volatile in recent months, despite a slight improvement in the first quarter. The housing market also remains relatively weak, as new and existing home sales numbers indicate.

US Consumer Confidence (tradingeconomics.com) Existing Home Sales (tradingeconomics.com) New Home Sales (tradingeconomics.com)

In our view, as long as the macroeconomic environment does not improve significantly, LEG’s financial performance is also unlikely to show material improvements.

Profitability

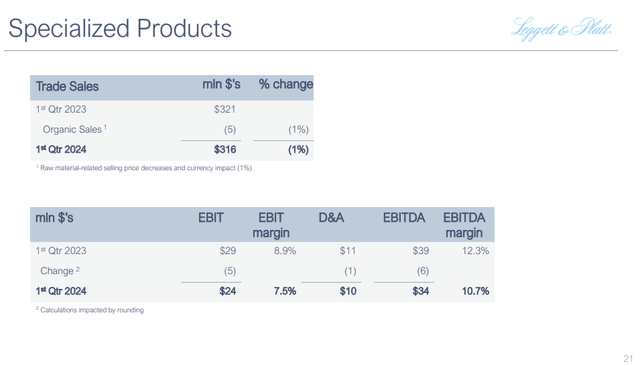

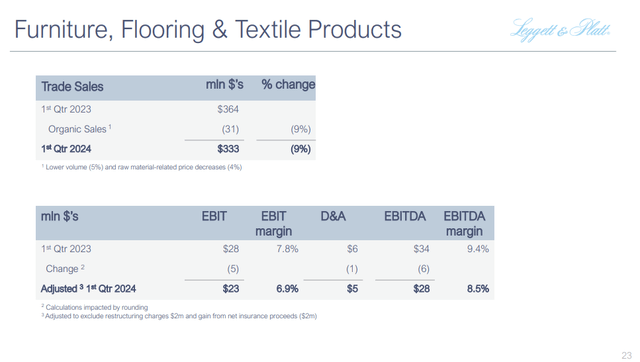

Not only do the sales figures look unattractive, but so does the company’s profitability. Profitability deteriorated as margin contracted in each segment, with bedding products again showing the greatest deterioration.

Bedding Products (LEG) Specialized Products (LEG) Furniture, Flooring and Textile Products (LEG)

Looking ahead, given weak demand and a challenging macroeconomic environment, we do not see an imminent catalyst that could help LEG improve its financial performance. Also, given the container crisis of the past months, sea freight costs may remain high in the near term, resulting in potentially higher expenses for LEG.

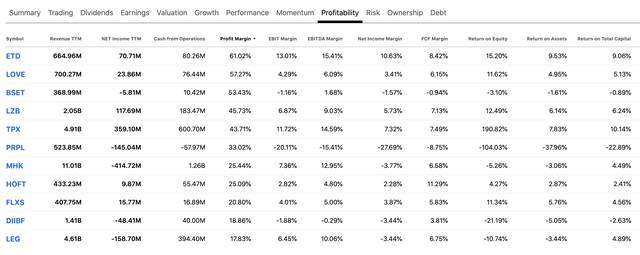

Comparing a company’s profitability metrics with its industry peers/competitors also shows that there are much better alternatives within the industry to consider.

Profitability (SA)

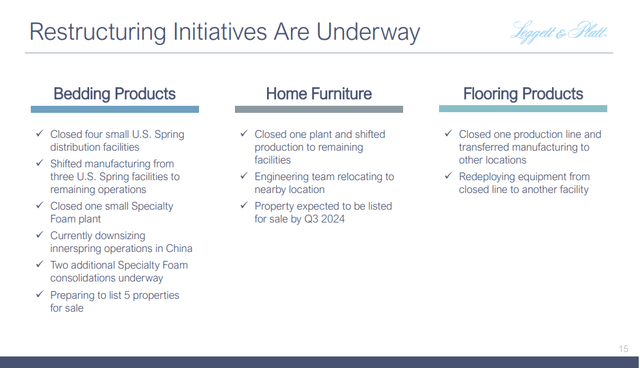

The company’s restructuring is still ongoing. Although some progress has been made, significant expenses remain to be incurred during 2024, which will weaken LEG’s financial performance in the coming quarters. Looking beyond 2024 and 2025, we would first like to see how the restructuring has actually improved the company, before we consider investing in the business.

Restructuring (LEG)

Capital allocation

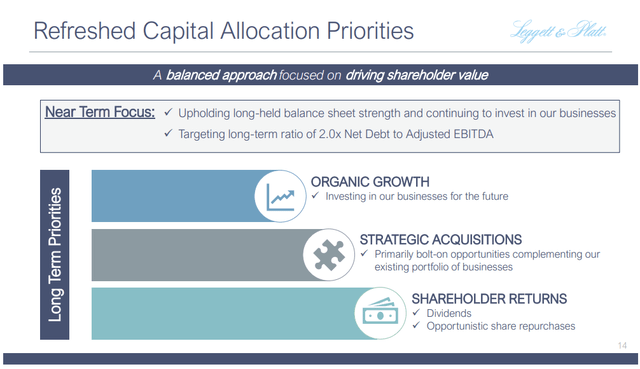

The main discussion regarding capital allocation should revolve around dividend cuts. On the one hand, this move is understandable for several reasons:

Financial performance has deteriorated, and the company needs money to implement its strategy. The cheapest money is internally generated money, so saving on dividends rather than debt/equity financing makes sense.

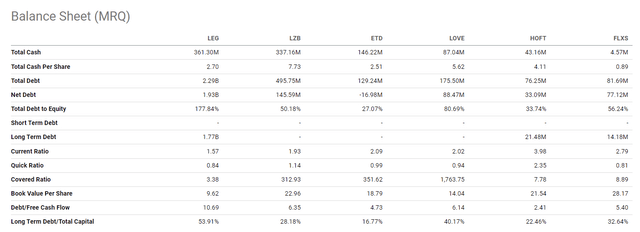

The company wants to reduce its debt, which also makes sense because the company’s liquidity currently appears less robust than that of its peers/competitors. In order to remain competitive in the long term, a company cannot always rely on debt.

A company’s financial flexibility is also key, especially in the current macroeconomic environment. Therefore, reducing debt can help a company become more viable in the long term.

Balance Sheet (SA) Capital Allocation (LEG)

On the other hand, however, LEG has been an option for many dividend and dividend investors, due to the company’s commitment to returning capital to its shareholders on a consistent quarterly basis. This is no longer the case, and given the uncertainties surrounding the company’s restructuring and management’s view of prioritization, we cannot say with any confidence when and how LEG could become an attractive option for dividend and dividend investors again.

evaluation

We believe that the previously used dividend discount model is not necessarily the best tool now to value a company’s shares following the recent dividend cut. While the company has been paying and growing its dividend for more than half a century continuously, a new era is now beginning. We can no longer say that profits are safe and sustainable. We also cannot make any assumptions regarding the dividend growth rate because the company is not prioritizing dividend payments now, due to the strategic shift, and at this moment it is difficult to say when and how its approach will change in the future. For this reason, any forecast made and any fair value inferred will have so much uncertainty that it is likely to be just a meaningless number.

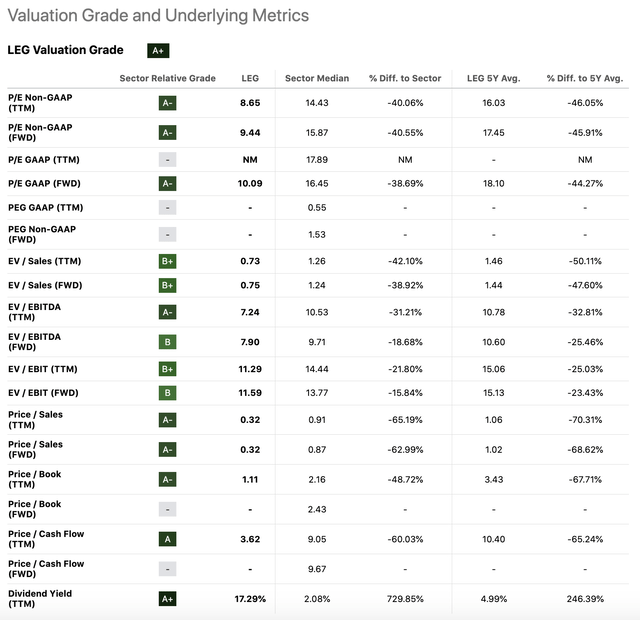

For this reason, we believe that a simple comparison of price multiples can give us a better picture of the company’s valuation, both compared to its peers and also to its historical valuation. The following table summarizes a range of traditional price multiples.

Rating (SA)

Due to the significant price decline over the past 12 months, the company appears to be trading at a significant discount now. However, we believe that this discount is justified. Declining sales, a challenging macroeconomic environment, shrinking margins, and uncertainty surrounding the company’s new strategy all support this thesis. At this point, we believe that starting a new position or even holding LEG shares can only be a speculative play, which is not supported by fundamentals.

Conclusions

Our previously established thesis that the company was undervalued based on its earnings and that expected earnings growth was invalidated, as the company cut its quarterly dividend to $0.05 from $0.46.

The company’s quarterly results are also worrying, including declining sales and shrinking profit margins. A challenging macroeconomic environment, including weak consumer sentiment and a weak housing market, makes the outlook even worse.

The results of the new capital allocation strategy are yet to be seen, and significant amounts of money still need to be spent in 2024 and 2025 until it is completed. This introduces a lot of uncertainty in the near term.

While the valuation looks attractive at first glance, it may be nothing more than a value trap. Such a discount compared to the sector average as well as to the company’s historical valuation is justified, in our view, due to weak fundamentals.

We downgraded the stock from ‘hold’ to ‘sell’.