Robert Y

Lee Otto (Nasdaq: Lee) delivered a mixed earnings budget for its fiscal first quarter last week, but the electric car company nonetheless saw solid delivery and strong growth. While Li Auto missed the upper and lower bound estimates, the electric car The manufacturer has also seen a sequential decline in its vehicle margins, which I believe is the most important metric for Chinese EV startups right now. Even with the sequential contraction in vehicle margins, I believe Li Auto still represents the best value for long-term EV investors as the company continues to outperform its competitors in terms of delivery growth and is already profitable on a net income basis!

Previous evaluation

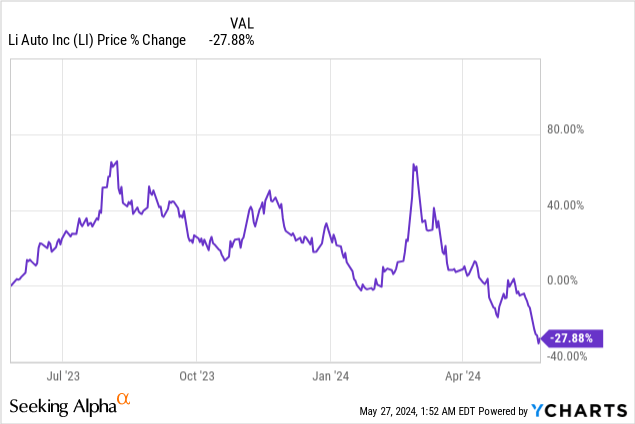

I rated Li Auto a Strong Buy in February, just when shares peaked after the company revealed it beat expectations In the previous quarter. While shares are down 55% since then, I believe Li Auto still represents deeper value as the company rapidly grows its deliveries, fueling revenue growth, and expectations for the second quarter point to accelerating revenue growth. In my opinion, Li Auto, from a valuation standpoint, offers the best value proposition in the crop of Chinese EV startups.

Li Auto estimates missed

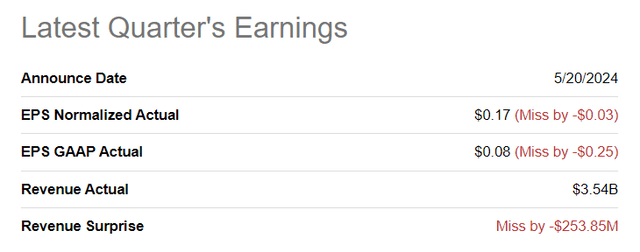

Li Auto missed consensus expectations for Q1 2024 last week: The electric car company generated $0.17 per share in adjusted earnings on revenue of $3.54. While Li Auto beat expectations, investors should take into account the fact that the EV maker is already profitable, something that sets Li Auto apart from other EV manufacturers, especially XPeng (XPEV) and NIO (NIO).

Seeking alpha

Li Auto Q1’24: Everything you need to know

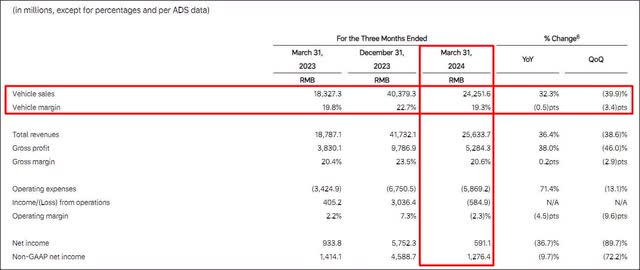

Li Auto achieved sales of CNY24.3 billion (US$3.4 billion) in the first quarter of 2024, showing 32.3% year-on-year growth. XPeng, which also announced revenue figures last week, achieved a higher figure of CNY5.54 billion ($0.77 billion) and growth of 57.8%. The first fiscal quarter is usually a disappointing one for electric vehicle companies due to the Chinese New Year period leading to factory closures. So, I don’t think the revenue P&L tells a good story, and as the outlook for the fiscal second quarter suggests, Li Auto expects a big rebound on the delivery front.

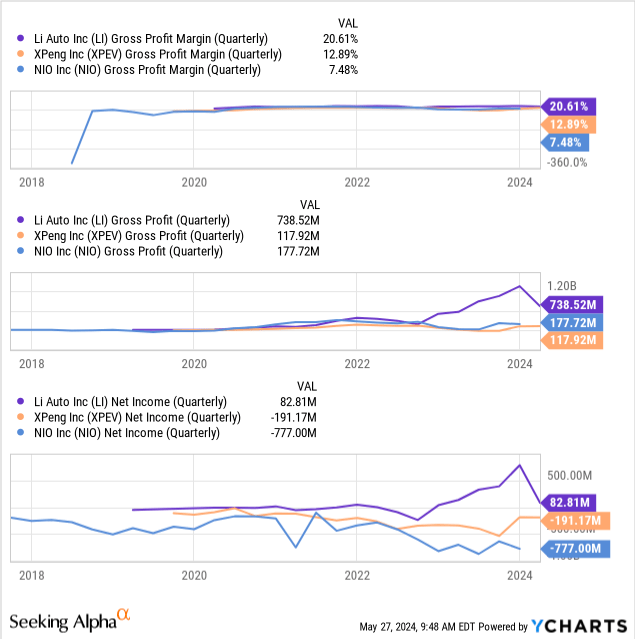

Unfortunately, Li Auto also suffered a 3.4 basis points q-o-q decline in its auto margin in the fiscal first quarter to 19.3%. While the auto margin decline was not significant, it is clear that Li Auto is still performing better than NIO (NIO) or XPeng (XPEV). For example, XPeng reported a vehicle margin of just 5.5%, so Li Auto does much better here in terms of unit economics. Although XPeng’s vehicle margin trend has improved, the company increased its vehicle margins by 1.4 basis points quarter-on-quarter, and investors should be aware that Li Auto’s unit margins are 3.5 times higher than XPeng’s.

Lee Otto

In addition, Li Auto has an advantage over other Chinese EV companies since the company is already profitable. Li Auto also leads the sector in terms of gross margins and absolute gross profit, being four times larger than NIO, for example.

Forecast for the second quarter of 2024

Li Auto delivered 105,000 and 110,000 electric vehicles in the fiscal second quarter, representing a year-on-year delivery growth rate of 27.1%. On a quarterly and mid-term basis, Li Auto expects a 33.7% rebound in deliveries as the company (and the industry) recovers from seasonal impacts in the first quarter of 2024. Total revenue is expected to be between CNY 29.9 and 31.4 billion (4.1 to $4.3 billion), indicating a potential increase of up to 9.4% year-on-year.

Li Auto Rating: Best-in-class value for electric vehicle investors

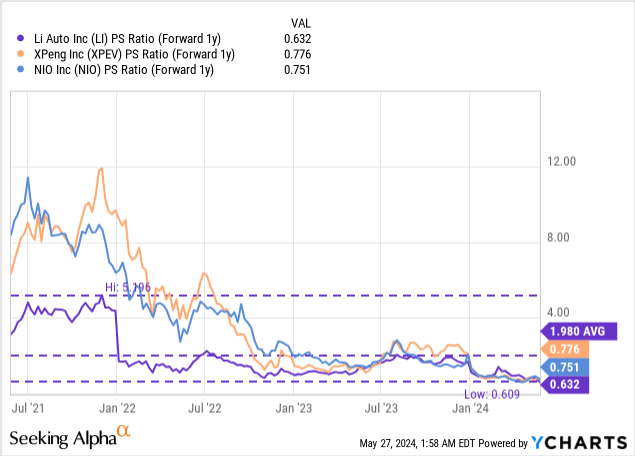

In my opinion, Li Auto continues to offer the best deal in the pantheon of Chinese EV startups consisting of Li Auto, XPeng and NIO. The main way Li Auto differentiates itself is through a highly efficient production line as well as a high factory production level that allows the company to achieve much stronger profit margins than competitors. Li Auto is currently valued at a P/E ratio of 0.63X which compares to P/S ratios of 0.75X for NIO and 0.78X for XPeng.

In my opinion, Li Auto deserves a higher revenue multiple simply because the EV maker has grown to a much higher production level than its competitors: it delivered 3.7 times more EVs than XPeng and 2.7 times more EVs than NIO in the quarter year First financial.

As I noted in February, I believe Li Auto could revalue to a fair value P/E of 2.0X – which is also equal to its long-term average P/E valuation – since the company is already profitable (as opposed to its dividend ) competitors), generating impressive gross margins/vehicles, and also has its highest quarterly delivery volume ever. The 2.0XP/S ratio suggests a fair value of $65 (down from $75 the last time I covered Li Auto, mainly due to lower revenue estimates).

Risks with Li Auto

The biggest risk Li Auto faces, as I see it, relates to the company’s vehicle margins, which are much better than what the competition achieves. Hence, an emerging downtrend in vehicle/gross margins would severely disappoint investors, given that the EV company is leading the startup sector in this regard. What might change my opinion about Li Auto is if its margin picture deteriorates or the company falls behind its competitors in terms of delivery growth.

Final thoughts

Li Auto delivered a mixed, but overall strong, earnings report for its fiscal first quarter, despite a sequential decline in its important auto margin. Li Auto is still growing deliveries and revenue by double digits, and the outlook for its fiscal second quarter deliveries and revenue growth isn’t bad either: it points to a strong rebound in deliveries, mainly due to seasonal factors.

What I still like about Li Auto is that the company has the largest delivery volume ever, and that the electric car maker is already profitable (and is expected to remain profitable on a full-year basis). Li Auto represents the deepest value to me in the Chinese EV startup group due to its combination of over 100K quarterly delivery volume (on a forward basis), high vehicle profit margins and a relatively low price-to-revenue ratio when compared against XPeng and NIO.