Lincoln National: Rising annuity sales in the industry are a blessing, and first-quarter results mask positive trends

Alistair Berg

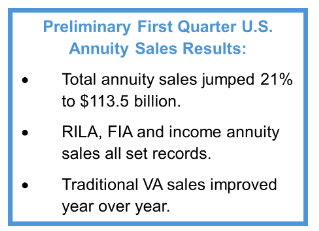

It was another excellent quarter for domestic premium sales. According to Limra, U.S. annuity sales totaled $113.5 billion from January to March, an increase of 21% from the same period the previous year. It was barely below the record amount for the fourth quarter of 2023 And the strongest first quarter since LIMRA began tracking the data in the 1980s.

There continues to be strong demand for protective investment solutions, whether it’s annuities, structured bonds, or buffered ETFs. Insurers appear to be in a good position, and today’s higher interest rates combined with some stability in the fixed income market is a blessing.

I am promotion Lincoln National Stocks (New York Stock Exchange: LNC) From waiting to buying. In late 2023, I was “intrigued” by LNC’s valuation, but stressed that patience was needed regarding its technical chart. The breakout occurred late in the year, and stocks stalled To the races ever since.

Strong annual sales for the first quarter

Limra

Slow down interest rate fluctuations

TradingView

According to Bank of America Global Research, Lincoln National (LNC) is a diversified life insurance company that offers annuities, individual life insurance, group benefits, and retirement products and services. LNC’s products are distributed through financial planners, telecommunications offices, banks, and managing general agents.

Lincoln earlier this month Q1 reported softat least on the surface. Non-GAAP EPS of $0.41 It missed expectations by a significant $0.69, while revenue of $4.58 billion, up 8% from year-ago levels, fell short of consensus estimates by $76 million. Adjusted operating income was impacted by material statutory vesting charges, severance expenses, a small write-off related to the sale of the wealth management business, and unusual tax expenses.

Step back from that, and the earnings power has actually been fairly impressive. Excluding these items, operating EPS would have been approximately $1.41. While Lincoln endured a net inflow of $2 billion from annuities, index-linked annuities enjoyed strong sales. I’d like to see better revenue across segments in the coming quarters after all the one-time charges in Q1.

So the picture with Lincoln is not as rosy as the pensions industry more broadly. Key risks the company faces include stock market weakness, the return of a low interest rate environment, continued outflows from key sectors, and reduced capital allocation. Upside risks include rising stock markets and stabilizing price markets along with the announcement of shareholder-friendly initiatives such as larger dividends and share buybacks.

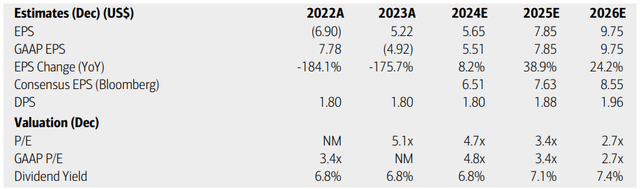

on evaluationAnalysts at Bank of America see… High profits 8% this year with a noticeable increase last year. Operating EPS is expected to be achieved near $9 by 2026. However, the current consensus estimate, per Seeking Alpha, is less optimistic than BofA. $5.92 is the current view with $8.26 non-GAAP EPS in 2026 while top line growth should be strong in 2024, +16%, but slower in outside years in low single digit range To average.

DividendAt the same time, it is expected to rise at a moderate pace over the coming quarters. With its very low P/E ratio and high yield, LNC remains a favorite among many value investors.

Lincoln National: Earnings, Valuation and Dividend Forecast

Bank of America Global Research

If we assume non-GAAP common EPS of $6.30 over the next 12 months and apply a 5-year average EPS multiple of 5.7, the stock should trade near $36, making it a buy. When evaluating. The company’s dividend yield is also well above its long-term average.

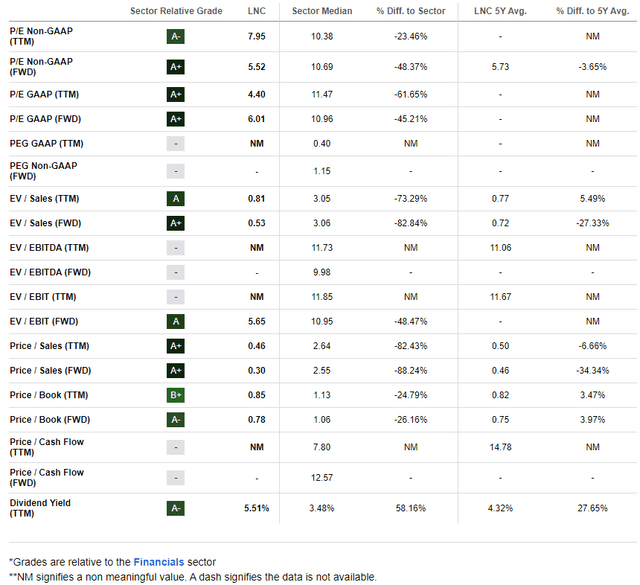

LNC: Compelling valuation metrics, high dividend yield

Seeking alpha

Compared to its peersLincoln has a very compelling set of valuation metrics while its growth trajectory has been mixed. With strong earnings per share expected in the coming quarters, Profitability trends With LNC is not attractive, however. But this is largely due to the extraordinary expenses incurred in the first quarter.

However, the sell side is by no means enamored with Lincoln, given his rally 8 Dividend cuts In the last 90 days without any upgrades. Last week, Jefferies bucked the broader trend LNC upgrade From hold to buy in light of the “return to retail” thesis. Stock price momentum It has improved significantly compared to Q4 2023, and I will detail the new areas of interest on the chart later in the article.

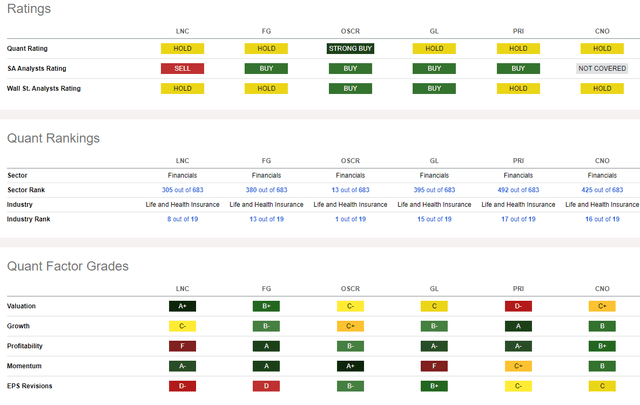

Competitor analysis

Seeking alpha

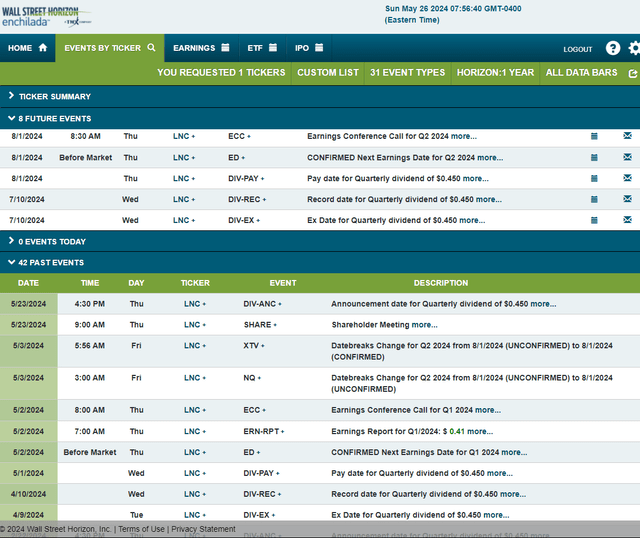

Looking ahead, corporate events data provided by Wall Street Horizon shows a confirmed Q2 2024 earnings date of Thursday, August 1 for BMO with a conference call immediately following the numbers. You can Listen live here. Prior to that, shares trade with a quarterly dividend of $0.45 on Wednesday, July 10.

Assessing the risks of corporate events

Wall Street Horizon

Technical take

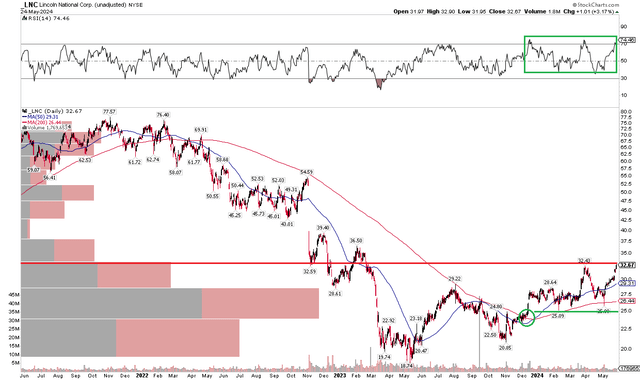

Last November, I noticed major support at the lows of $20 with resistance at the long-term 200-day moving average that was falling at the time. Notice in the chart below that the bulls defended the support area and lifted LNC above its 200 day moving average by late 2023. While $29 was resistance, a new support area came in at $25. Over the past several months, $25 has held a pair of retests while the 200-day EMA is now positively sloped. These are favorable technical developments.

Also take a look at the Relative Strength Index (RSI) momentum indicator at the top of the chart – it ranges in the markedly bullish territory from 40 to 90. Furthermore, there are now a large number of shares trading below the current share price, suggesting The necessity of buying dips in the stock. There is also little public supply of shares until they reach around $40. Finally, $32, the highest price since April, could serve as near-term resistance.

Overall, there has been a bullish momentum reversal and positive shift in LNC’s technical chart over the past six months.

LNC: Trending higher this year, upside momentum, $25 support

StockCharts.com

Bottom line

I see LNC as a more favorable risk/reward setup today, given the breakout last December. While the first quarter was bad on the surface, the company’s normal operations appear to be in a strong position. With the stock still undervalued and setting up better momentum, I consider the stock a buy.