Just excellent

Lithium Americas Corporation (New York Stock Exchange: Latin America and the Caribbean) fell to a new low on a new short report. The lithium miner faces normal risks from volatile lithium prices and diluted financing in the future, but the risks are overstated in the report. My investment thesis The company remains very bullish on the stock amid expectations of higher lithium prices in the future, while the company does not have any near-term exposure impacted by current low prices.

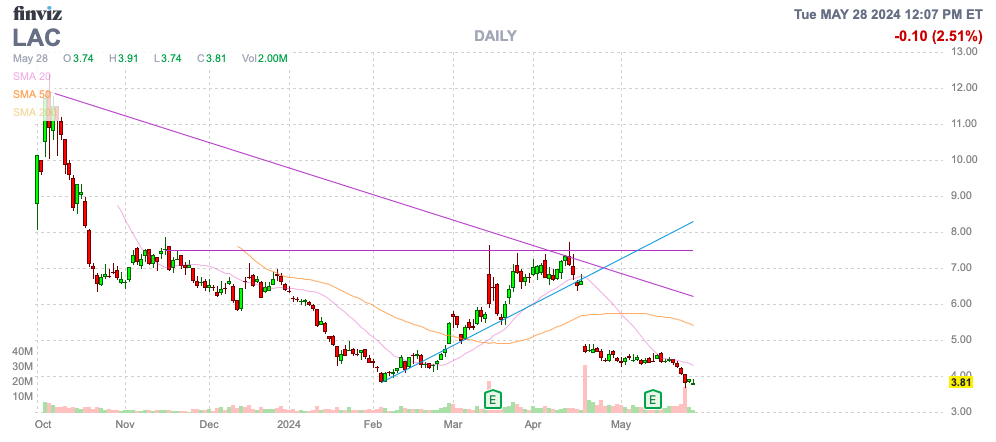

Source: Finviz

Biggest short hit

Bleecker Street Research hit the stock with a short report last week and the company is clearly suffering from a lithium Americas shortage, but the company appears to be making an extra effort to distort the truth about the lithium miner. In editorial summaries, the research firm calls the company a “junior miner” and a “stock promoter.” While the first claim is technically true, both claims appear as a deliberate attempt at distortion market.

Source: Bleecker Street Research

While Lithium Americas is technically a pre-revenue mining company now, the company and management team recently completed the Caucharí-Olaroz lithium mine in Argentina and separated the business from Lithium Americans (Argentina) (lac). One of the key investing points is this very crucial distinction.

Since Lithium Americas has a recent history of opening a lithium mine, the whole stock promotion thesis should be thrown out the window. not to mention, General Motors (GM) is firmly in the mining company and the Department of Energy has conditionally approved a major loan for the Thacker Pass mine, providing a long list of credibility to avoid the stock promotion label.

Once you get past some of the smear attempts, the biggest negative from Bleecker’s short report is that Lithium Americas somehow has technology that cannot be supported in the current market. The executives have already developed the Lithium American (Argentina) mine in Argentina and are highly experienced in the lithium mining sector, although this clearly does not mean that the management team is out of touch.

One common thread of the short reports is the questioning of technology and product assumptions by respected experts that most investors do not have the knowledge and experience to challenge. Management would have no reason to exaggerate Thacker Pass claims.

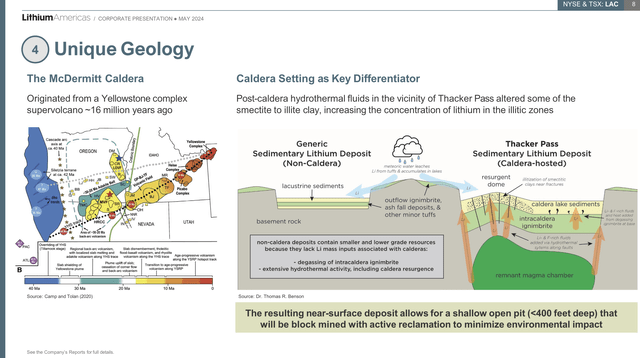

The geology of McDermitt Caldera was recently estimated to contain one of the largest lithium deposits in the world. If anything, lithium in the Americas may have much more resources than expected.

Source: Lithium Americas Q1 2024 presentation

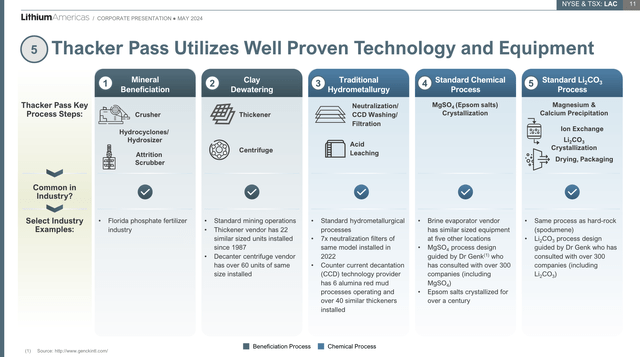

Lithium Americas went into great detail in its Q1 2024 presentation, highlighting how the Thacker Pass project uses proven technology and equipment. The lithium miner has already produced lithium carbonate samples from Thacker Pass since July 2022 with proven production of high-quality battery lithium through its continuous production process.

Source: Lithium Americas Q1 2024 presentation

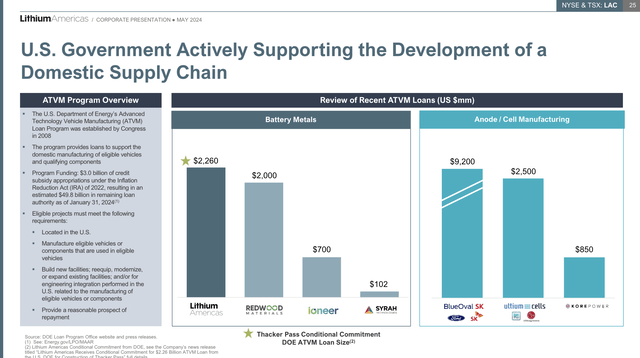

The short report appears to expand significantly on the past history of DOE loans. The US government has a bold new plan to support the domestic supply chain, including a major focus on lithium production for electric vehicles.

Source: Lithium Americas Q1 2024 presentation

Redwood Materials’ $2 billion loan was conditionally approved last year, and the inflation-reduction law was only passed in August 2022. Any prior loans were entirely subject to a different era.

Again, the main negatives are actually unproven points distorted by the past without any concept of the current market difference. The concepts of clay lithium mining are new and constantly being improved.

Lithium prices

As much as one might want to delve into the economics of any particular mining project, what ultimately matters for the share price is the price of the relevant commodity. As for Lithium Americas, with mines not producing until 2027, lithium prices will drive the stock price.

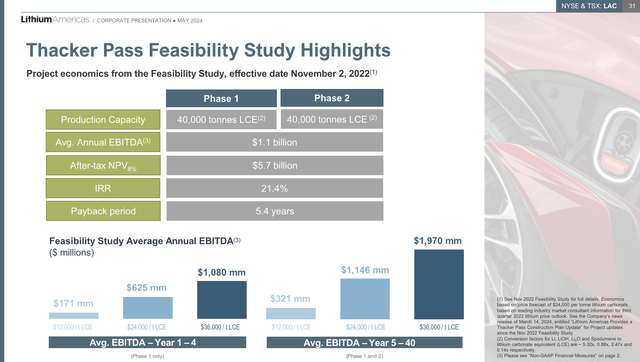

Unit economics remain strong for the project. Lithium Americas expects the company’s EBITDA to be positive on lithium prices of just $12,000 per ton LCE due to lower production costs.

Source: Lithium Americas Q1 2024 presentation

Bleecker Street Research disagrees with predictions that the project will be uneconomic, although Lithium Americas points out that the cost of the project is only $7,000 per ton. The market won’t actually know for years whether a company is accurate or short-reported.

Remember, a large part of the low costs is due to the size of the mine. The short report does agree that the targeted 80,000 tons of LCE amounts to approximately 8% of the global LCE market. The size of the project is one of the main reasons why the Thacker Pass project is economical.

The main point of investment in Lithium Americas is based on the shortage of lithium supply when the project reaches the market in 2027 and an experienced management team. CEO Jonathan Evans has been CEO of Old LAC since May 2019 and has been primarily responsible for taking the mine into production. Not to mention that General Motors is the main investor and that many of the previous mistakes in the electric car sector have been exaggerated by the report that was considered to be ultimately canceled by the company. Nicola (NKLA) before officially agreeing to a deal to invest in the company, supply equipment and build the Badger pickup truck.

The CFO, Executive Vice President – Capital Projects, Senior Vice President – General Counsel, and Vice President – Resource Development each have different experiences working in the legacy LAC region. The management team has extensive and recent experience in developing a new lithium mine.

Lithium Americas has more than $400 million in cash after its recent secondary offering. Combined with the Department of Energy’s $2.26 billion loan and GM’s additional $330 million tranche, the company expects to have all the cash needed to finance the lithium mine project without the need for an additional dilutive offering.

The company has already spent $250 million on capital expenditures for the project, leaving only about $2.7 billion left to finance the mine. If anything, Lithium Americas now has $300 million in excess financing with access to nearly $3 billion in funds, but nothing is guaranteed in the stock market especially with new mines.

Morningstar analyst Seth Goldstein reiterated the stock’s $12 price target following the short report. The research has already assumed that costs and lithium production are below expectations to achieve this target on a stock that is now at $4. The upside potential is that the company actually achieves the goals.

He stays away

The most important thing for an investor to take note of is that Bleecker’s short report certainly asks some of the right questions. Unfortunately, the report seems to overemphasize some historical facts that are not necessarily relevant now.

Investors should be aware that Lithium Americas is a highly speculative stock. The stock offers strong risk/return potential for those who believe in lithium’s long-term potential.