Editorial by Moshe Einhorn/iStock via Getty Images

Lockheed Martin (New York Stock Exchange: LMT) Stocks have been treading water since their initial bounce following the Russian invasion of Ukraine.

Despite the remarkable increase in geopolitical tension in several parts of the world As the backlog grows, shares have remained essentially flat over the past two years.

Let’s try to understand why.

Background – two years of recession

I’ve been covering Lockheed Martin’s issue of Search for Alpha for more than a year. Back in March 2023, I rated the stock a strong buy, as I viewed supply chain disruptions and several other headwinds as temporary.

At the time, the company’s management was adamant that it could return to mid-single-digit growth in 2024 and was quite confident in its goal of delivering 156 F-35 fighter jets per year, starting in 2025.

Two quarters passed, and I decided to discount The stock was held up because I understood that two critical aspects of my investment thesis were wrong.

First, management clearly stated that they did not expect to see a margin benefit from increased demand, which reinforced my major concern that the company had no pricing power at all.

Second, it is becoming increasingly clear that the industry is too “heavy” to make the much-needed transformation to become a faster, more agile chain. I laugh even making the comparison, but we can look to another capital-intensive industry in semiconductors, which has shown the ability to capitalize on demand shocks whenever they occur.

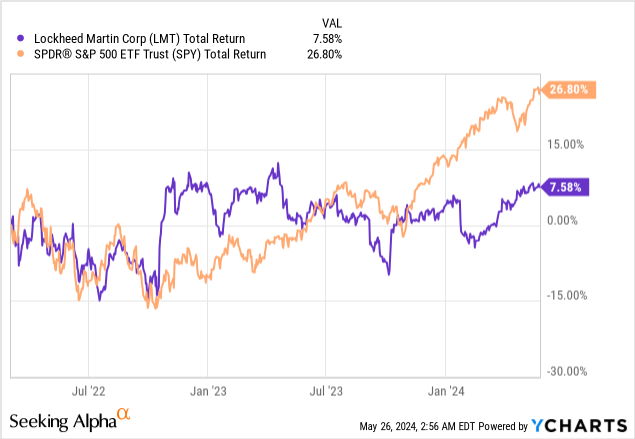

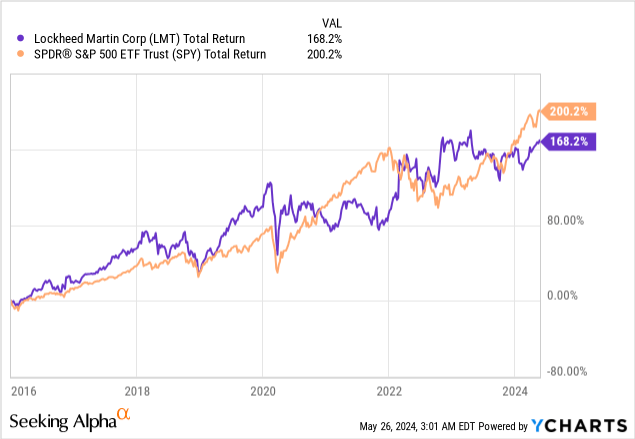

In fact, since that post-invasion bounce, Lockheed Martin has far underperformed the market, with total returns of 7.6% compared to the S&P 500’s return of 26.8%.

In fact, you’d have to go back to 2015 to get a baseline that would have Lockheed outperforming the market on a total return basis, which means we’re about to hit a full decade of underperformance.

With this background in mind, let’s look forward.

Rising geopolitical tension and increasing defense budgets

One thing I’ve tried to make as clear as possible in my three bearish articles since July 2023 is that demand is not the issue for Lockheed. I keep getting a number of comments saying I’m wrong about the company because demand is so strong. So I think I need to devote an entire section to this idea.

It’s no secret that geopolitical tensions are on the rise around the world. Aside from the Russian-Ukrainian war that has been going on for more than two years, we have a war in the Middle East between Israel and Iranian proxies, which has escalated into direct attacks between Iran and Israel as well. We can also see the rise of Islam and pro-Palestine supporters around the world, which increases tension within countries around the world, especially in Europe. In addition, relations between China and the United States continue to deteriorate.

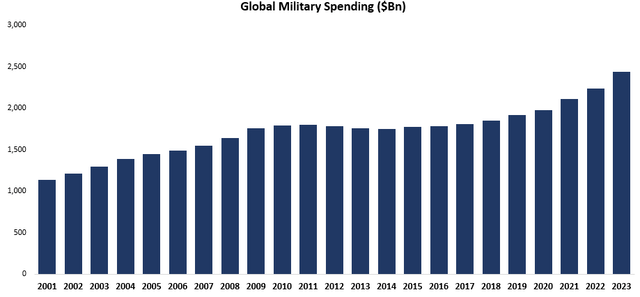

Created by the author using data from Statista.

As geopolitical tensions rise, so are defense budgets, which reached a record $2.44 trillion in 2023, up 6.8% in real terms from 2022. NATO’s share of spending is 55%, led by the United States at $916 billion, followed by Europe. . Members who come together to spend $375 billion.

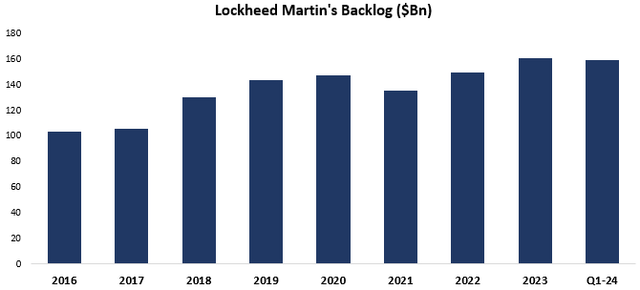

Created by the author using data from Lockheed Martin financial reports.

NATO members are Lockheed Martin’s customers, and the increase in their spending is clearly reflected in the company’s backlog, which grew 7% in 2023, to a record $160 billion.

So, let me be clear, Lockheed Martin does not have a problem with demand. Although backlog fell slightly in the first quarter of 2024, it will likely end the year on a high note.

Struggling to capitalize on growing demand

Demand is only one side of the equation. If a company has high demand, it still needs to take advantage of it, either by having enough supply and increasing volumes or by increasing prices.

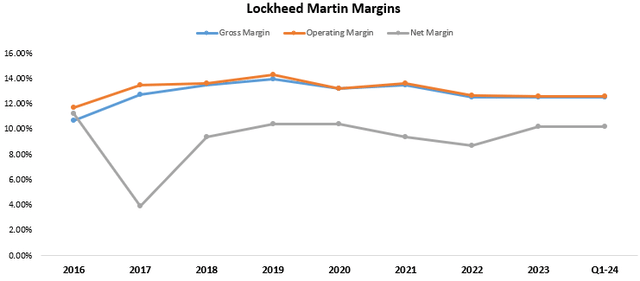

However, Lockheed has a pricing option problem because it is a government contractor, and its prices are primarily determined by cost-plus agreements.

This is best reflected in the company’s margins, which remain constant, for good and for bad:

Created and calculated by the author using data from Lockheed Martin financial reports.

Therefore, the company has only one option left, which is to increase quantities. The problem here lies in what we discussed previously, which is the slowness and intensity of the supply and production chain.

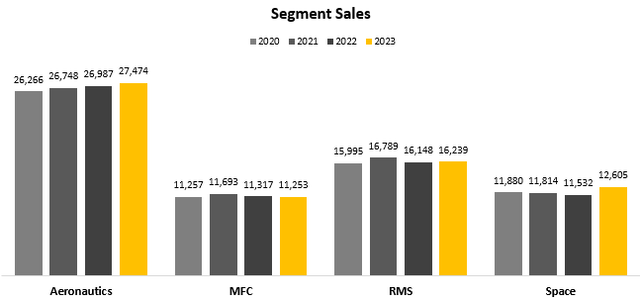

Prepared by the author based on data from Lockheed Martin financial reports; MFC = Missile and Fire Control; RMS = Rotary and Mission Systems.

We can see that in the four years following the pandemic, the company’s sales stagnated, with CAGRs of 1.5%, 0.0%, 0.5%, and 2.0% in aviation, MFC, RMS, and aerospace, respectively.

However, in the first quarter we saw a significant acceleration in each of the segments, resulting in a consolidated growth of 13.7%. That would have been a big sign of improvement if management hadn’t made sure to temper the excitement, as they reaffirmed their previous guidance for 2.5% growth in 2024, attributing the strong growth in the quarter to an easy comparison.

Additionally, recent reports indicate that issues are delaying some F-35 upgrades, which are still parked in Lockheed warehouses.

Drivers of valuation and stock performance

I hope I have been able to prove two important points here. The first is that demand is strong. The second is that Lockheed is struggling to capitalize on it.

Now, it’s important to remind ourselves of the factors that drive stock performance. In general, for a stock to outperform the S&P 500, which should be the ultimate goal for most investors, it needs to grow faster than the market-weighted average.

There is room for debate about the exact measure a company needs to outperform the market. Some might say FCF per share, some might say EPS per share, some might say revenue growth.

For me, it’s not an either/or, but a combination of all of these, as each of these metrics has pros and cons.

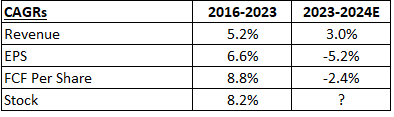

Created by the author using data from Lockheed Martin and Seeking Alpha financial reports.

For LMT, we can see that the stock’s performance was closer to the FCF’s CAGR per share between 2013-2016. Looking ahead, consensus estimates for 2024 project revenue growth of 3.0%, decline of 5.2% and 2.4% in earnings per share and foreign funds per share.

Over the long term, revenues are expected to grow at a low-single-digit rate (~3%), while earnings per share and cash flow per share are expected to grow at a mid-single-digit rate (~5%), outpacing revenues only by roughly Due to buybacks.

Lockheed is not the type of company that easily beats estimates or brings many surprises. Therefore, we can assume that it will come close to these numbers, which are not market-beating numbers.

Then we are left with only one way to achieve market-beating returns, which is valuation.

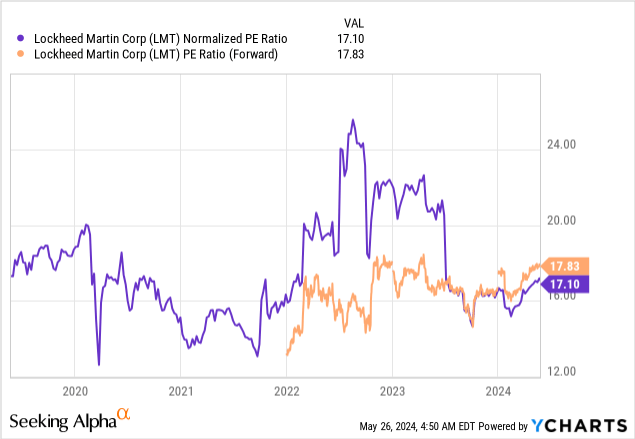

LMT currently trades at 17.8 times expected 2024 EPS, which is 7% above its 5-year average on a GAAP basis and 12% above its GAAP basis.

Unfortunately, this doesn’t sound very attractive either.

Conclusion

Lockheed Martin is a slow-growing and complex company, with limited capabilities due to the nature of its contracts.

Investors should expect market-average returns at best from Lockheed Martin, with slightly lower volatility, resulting from low- to mid-single-digit growth, along with a steadily increasing dividend starting at a 2.7% yield.

While this may be attractive to a certain group of investors, I believe the majority of individuals should either seek to outperform the market or take the passive investing route.

Therefore, I repeat a Hold rating for LMT.