Narvik

introduction

On April 24, I wrote an article covering shares of Alexandria Properties, a real estate investment trust that owns healthcare properties, including laboratories.

This REIT is on my radar as a great way to leverage innovation in Healthcare without having to know which biotech company will unveil a groundbreaking drug next.

(…) The company provided facilities that allowed groundbreaking research to be conducted, with the company noting that nearly half of all treatments approved by the Food and Drug Administration over the past ten years were attributable to its tenants.

Purchasing real estate also protects investors from the current period of high patent losses among major pharmaceutical companies.

In February, the Healthcare Technology Report wrote that the 20 largest biopharma companies collectively face a $180 billion drop in patent revenue through 2028!

While this comes with risks, there are many ways to benefit From the related desire for innovation in the industry.

- Real estate: Alexandria has certainly found a way to capitalize on this by renting to some of the most stable tenants in the world. However, this somewhat limits the upside potential.

- Biotechnology companies: Finding attractive biotech companies that have strong drugs on the market or in production can be very beneficial.

- Suppliers.

The third point is why I am writing this article.

Since I have a background in supply chains, I like companies that benefit from growth in a particular industry without massive competition, as they can supply a wide range of customers.

This is the place Thermo Fisher Scientific (New York Stock Exchange: TMO) Enter.

Thermo Fisher is a company owned by some family accounts and a competitor to Danaher Corporation (DHR), a closely related company that it bought a few years ago.

My last article on this fascinating dividend growth compound was published on February 6, when I chose the title “The bright future for Thermo Fisher makes it a great buy for double.”

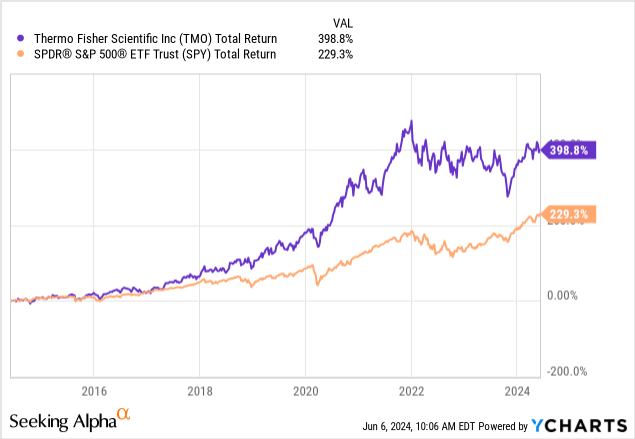

Since then, the stock has returned 3%, lagging the S&P 500’s 8% return.

Over the past 10 years, TMO’s total return of 400% has outperformed the S&P 500 by about 170 points.

In this article, I will revisit my bullish case and explain why I believe this company is in a great position to exploit strong tailwinds in the healthcare/biotech sector.

I also think it’s still a great dividend growth stock despite its low yield and what some might consider a high post-pandemic valuation.

So, since we have a lot to discuss, let’s do it!

Buy innovation in healthcare

I have often written articles about my interest in innovation in healthcare.

It’s really great to see how blockbuster drugs can fight serious diseases and significantly improve the lives of so many people.

However, selecting winners in healthcare is not easy, as it comes with a great deal of uncertainty, including regulatory approval risks, competition, financing risks, and others.

While I invest in biotech companies – I own AbbVie (ABBV) and have other companies on my watchlist – I’m a big fan of buying suppliers.

Although these companies also come with competition, they are often in a great position to capitalize on the public need for innovation in healthcare, as this creates increased demand for related equipment and supplies.

Headquartered in Waltham, Massachusetts, Thermo Fisher serves a wide range of clients, including pharmaceutical and biotechnology companies, hospitals, clinical diagnostic laboratories, universities, research institutions and others.

They are sold through brands such as Thermo Scientific, Applied Biosystems, Invitrogen, Fisher Scientific, Unity Lab Services, Patheon, and PPD.

Thermo Fisher Scientific

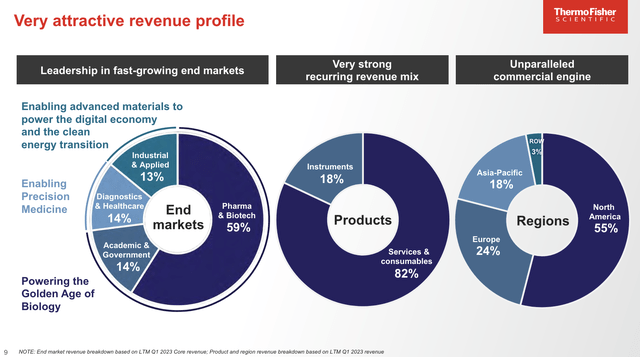

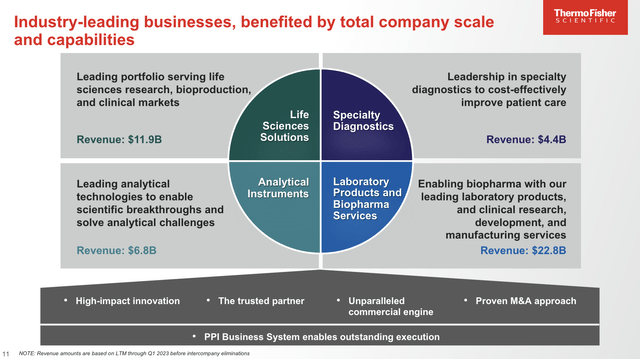

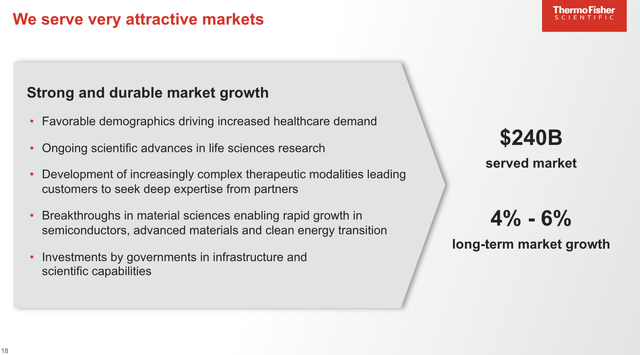

As we see below, the company sells its products through four major multi-billion-dollar segments each targeting a specific area of the healthcare/biotechnology sector, including life sciences, specialty diagnostics, analytical instruments, laboratory products, and biopharmaceutical services.

Thermo Fisher Scientific

Taking all things together, approximately 60% of its revenue comes from the pharmaceutical and biotechnology sectors, which are expected to grow at 4% to 6% annually.

These numbers were 3-5%.

However, as the company has made internal changes with a greater focus on growth markets, it is now seeing consistently higher growth.

Thermo Fisher Scientific

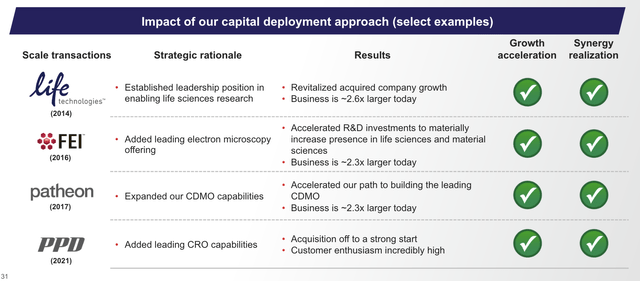

During the Bank of America Healthcare Conference last month, the company explained that strategic mergers and acquisitions played a key role in growing at a faster rate.

This includes PPD and Patheon, which have significantly improved the company’s service offerings and deepened its relationships with biopharma partners.

According to the company, these acquisitions have expanded its capabilities and positioned it as a trusted partner in the development and manufacturing operations of pharmaceutical companies.

Thermo Fisher Scientific

In addition, the company believes that its exposure to China represents a significant benefit.

Last year, 18% of its revenue was generated in the Asia Pacific region.

Despite China’s economic slowdown in 2023, the company expects to benefit from the Chinese government’s multi-year fiscal stimulus program focused on capital equipment.

This program is expected to have a positive impact on the analytical tools sector.

While China experiences post-pandemic weakness, the company expects the revenue benefits to be realized in late 2024 and into 2025, which is great news for the entire industry, in my opinion.

Furthermore, the company’s focus on cutting-edge research and cutting-edge technologies, including the Orbitrap Astral Scientific Thermal Mass Spectrometer, positions it well to capture growth in what has become a rapidly evolving life sciences sector.

The Orbitrap Astral mass spectrometer achieves this by analyzing samples in just 8 minutes from injection to injection, allowing 180 samples to be obtained per day. Each injection can identify more than 8,000 proteins in a standard cell lysate sample, breaking through a bottleneck in sample analysis. This faster throughput allows more than 1.4 million cumulative protein array measurements to be analyzed across 180 samples in a single day, meaning a single Orbitrap Astral mass spectrometer can measure tens of thousands of samples per year. – Thermo Fisher

Although this all sounds good, what does this mean for shareholders?

Not cheap, but far from expensive

Thanks to strong performance and a rebound in demand, TMO raised its first-quarter guidance, now expecting revenue of at least $42.3 billion.

This is expected to result in an EPS range of $21.14 to $22.02.

During its Q1 2024 earnings call, the company also announced strategic partnerships, including its partnership with German healthcare giant Bayer to develop next-generation sequencing-based facilities.

This bodes well for shareholders.

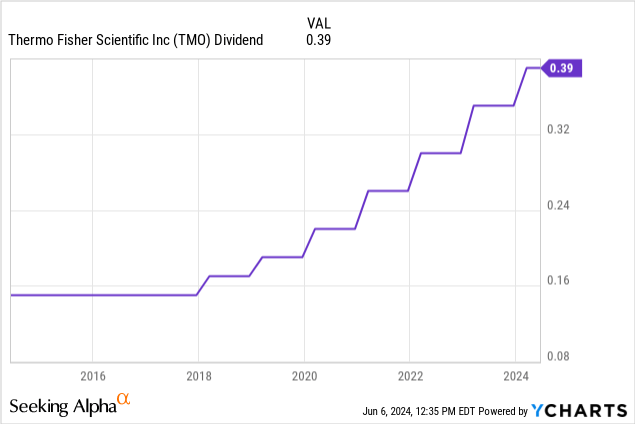

In the first quarter, Thermo Fisher bought back $3 billion worth of stock and increased its dividend by 11.4%.

Currently, it pays $1.56 per share each quarter, giving us a yield of 0.3%.

0.3% is not much. An investment of $10,000 will receive a profit of $30 before taxes. That’s two trips to the fast food chain with the big yellow “M” – for one person.

However, please keep a few things in mind.

It’s not TMO’s fault that its dividend yield is so low.

The five-year compound annual growth rate is 15.5%!

Its yield is low because capital gains offset earnings growth, which explains why it has a great total return.

Obviously, if you need dividend income, the TMO is the wrong one for you.

However, everyone may benefit from purchasing low-yielding dividend growers.

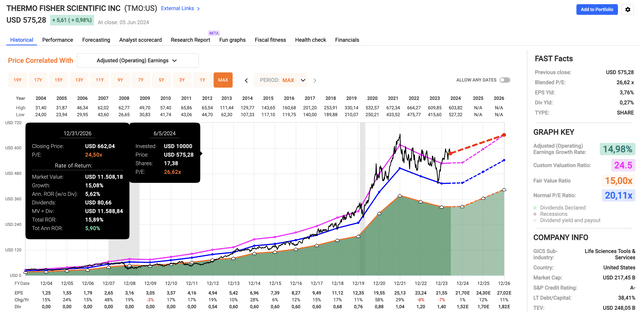

However, using FactSet data in the chart below, analysts agree with the company. After a tough few years post-pandemic, EPS growth this year is expected to reach 1%.

Quick charts

In 2025 and 2026, EPS growth is expected to reach 12% and 11%, respectively.

Currently, TMO is trading at a blended P/E of 26.6x. This is slightly higher than the five-year normalized P/E ratio of 24.5x and much higher than the two-decade normalized P/E ratio of 20.1x (blue line in the chart above).

The reason TMO is not selling is because investors know there is a path to consistent double-digit annual EPS growth, supported by mid-single-digit revenue growth.

Everyone knew that the post-pandemic years would be difficult. Selling on expected weakness is not something investors will do when a positive long-term outlook is confirmed.

While the company’s returns could remain low over the next year or two, I would still expect mid- to high-single-digit annual returns.

Since 2004, TMO has returned 16.7% per year!

Although I don’t expect to see these returns anytime soon, I have no doubt that this powerful business model is capable of delivering high returns in excess of 10% once we leave the slow post-pandemic years behind us.

That’s why my family keeps buying TMO.

The only reason I don’t own it is because of my investment in DHR. I love both and don’t have a favorite.

Away

Thermo Fisher Scientific is a remarkable company in the healthcare and biotechnology sectors, which continually benefits from the industry’s demand for innovation.

Despite a lower dividend yield of 0.3%, TMO’s strong organic growth and strategic acquisitions have led to impressive total returns.

Given its favorable growth outlook, TMO remains a compelling investment for those seeking long-term growth rather than high income.

While the post-pandemic period presents challenges, the company’s strategic positioning and partnerships ensure that it remains a major player in healthcare innovation, with what I believe is a very promising future.

Pros and Cons

Positives:

- Strong growth potential: TMO is well positioned to exploit significant tailwinds in the healthcare and biotechnology sectors.

- Strategic acquisitions: Previous acquisitions such as PPD and Patheon improve TMO’s growth capabilities.

- Innovative edge: Cutting-edge technologies allow the company to stay on top of the latest trends.

- Long term returns: TMO has a history of impressive total returns and consistent earnings growth, which I expect will continue.

cons:

- Low dividend yield: At just 0.3%, the dividend yield is nothing to write home about.

- evaluation: Trading at a blended P/E ratio of 26.6x, TMO is slightly overvalued, which means it needs to provide its guidance (there is no room for error).

- Short-term challenges: The post-pandemic recovery phase may pressure returns over the next year or two, which could limit short-term gains.

- China exposure: Relying on the Chinese market comes with some risks, including political and cyclical risks post-pandemic.